- S&P and Nasdaq futures little changed in Thursday morning trading ahead of the PPI inflation data. Comes after US equities pulled back on Wednesday, but still finished well off their worst levels for the session. Bond proxies, homebuilders, home improvement, energy, aluminum, trucking, ag chemicals among the laggards. Big tech mixed. Drug stores, autos, managed care, biotech, China tech, airlines and exchanges outperformed. Asian markets mixed overnight with Hong Kong giving back some recent strength and Japan up over 1%. European markets higher, up ~1%. Treasuries firmer after a big backup in rates on Wednesday. Dollar index down 0.1% with euro extending recent strength. Gold up 0.5%. Bitcoin down 2%. WTI crude down 1.5% after losing more than 2.5% in prior session. See chart below.

- Trade Ideas Sheet: I covered DE ahead of today’s earnings with a small gain as it had diverged positively from CAT short and I didn’t have strong read on the report today. They beat with a low quality report (low tax rate) and guided lower and the stock is lower by 4.5%. We still have CAT short and it’s been working. Seeing a lot of dispersion with earnings reactions both up and down from yesterday and today.

- Market waiting for details on reciprocal tariffs, particularly in terms of potential carveouts/concessions and whether there is any attempt to equalize non-tariff barriers. Fits with broader Trump 2.0 policy uncertainty. Also a lot of attention surrounding potential Trump-Putin meeting as Ukraine ceasefire hopes ramp up. However, spillover effects for US equities from an end of the conflict seem fairly limited (weaker oil, stronger euro). Retail buying (including on dips) continues to be flagged as excessive, though also some concerns about its ability to continue as looming seasonal influences turn negative.

- PPI and initial claims on the economic calendar this morning. In addition, Treasury selling $25B of 30-year bonds. Nothing in terms of Fedspeak after Powell’s monetary policy testimony failed to break any new ground and was seemingly overshadowed by the hotter CPI print on Wednesday. This pushed probability of a June rate cut well below 50% and left the market pricing in just over 25 bps of easing for the entire year. Retail sales, import/export prices, industrial production and business inventories cap off the week on Friday.

- DE beat but was a low quality with a lower tax rate, lowered guidance. CSCO boosted by AI, Splunk and new product tailwinds. APP up big on big beat and guide above with Advertising the tailwind. EQIX Q4 results and 2025 guidance light. RDDT takeaways largely positive but expectations very elevated and DAUs missed. MKSI beat but guide light. FSLY pressured by margin headwinds, cash burn. UPWK beat, guided in line and said macro still challenged. RCL boosted dividend and announced $1B buyback. BROS up big on comp strength. MGM helped by positive LV commentary. ALB boosted by better FCF takeaways. TTD missed for first time in over 30 Qs. HOOD takeaways noted include blowout Q and strong Jan metrics.

- Key Upgrades/Downgrades: DuPont de Nemours upgraded to equal weight from underweight at Barclays. Trade Desk downgraded to in line from outperform at Evercore ISI. Cisco Systems upgraded to buy from neutral at Rosenblatt Securities. Gordon Haskett upgrades CASY; downgrades M, TGT.

market snapshot

economic reports today

premarket trading

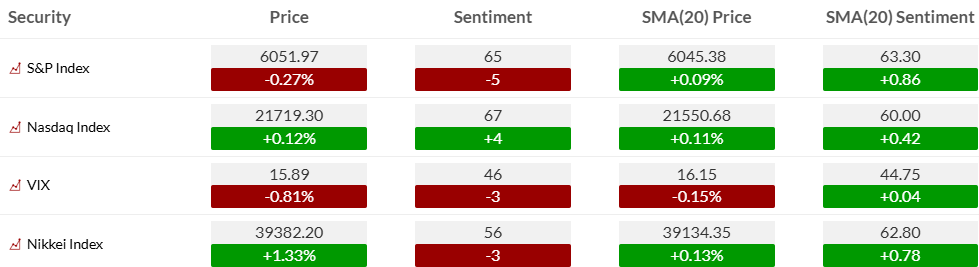

US MARKET SENTIMENT

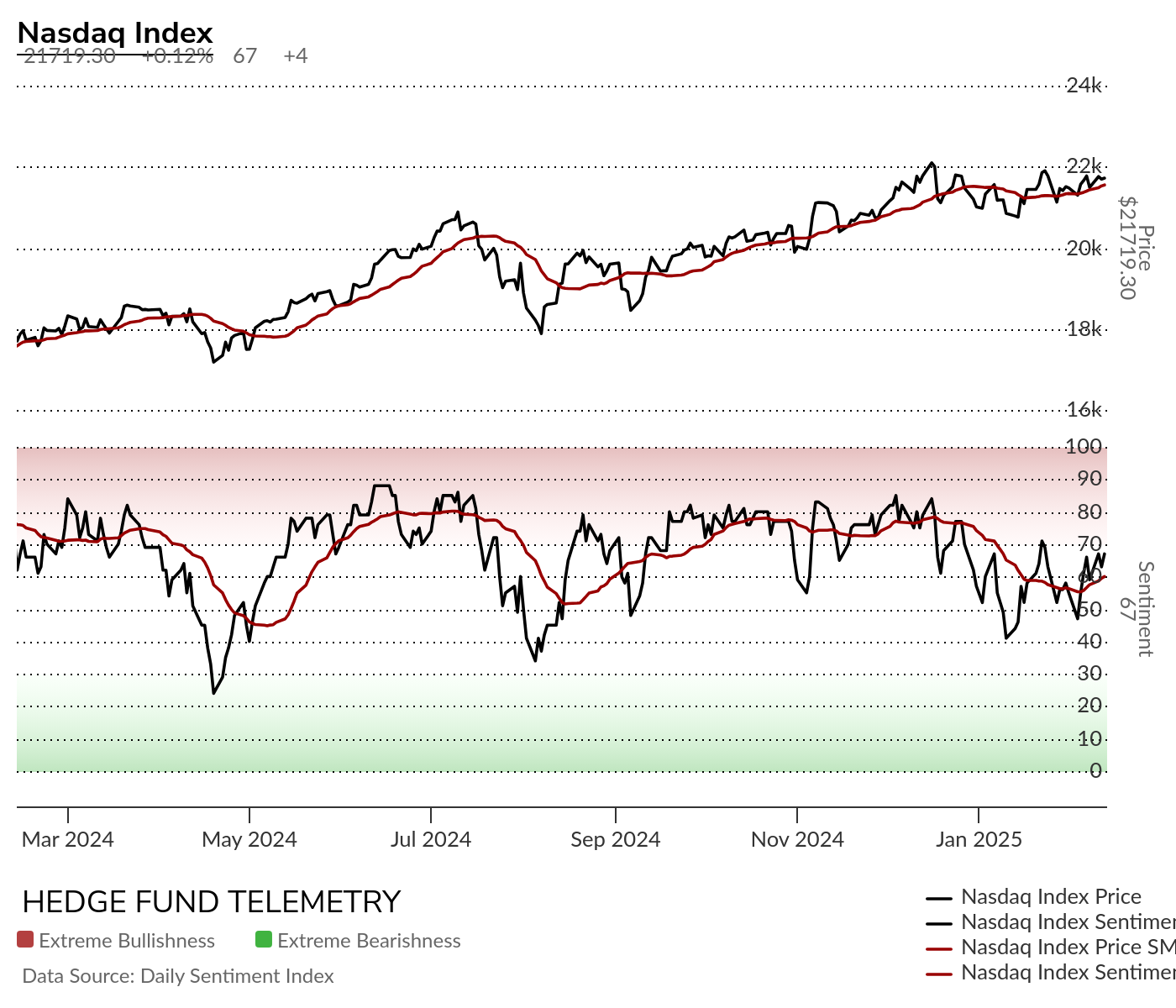

S&P and Nasdaq bullish sentiment was mixed yesterday and back in the 60’s under the elevated zone >70%

Bond bullish sentiment fell hard and just couldn’t keep the momentum going to clear the 50% midpoint majority level.

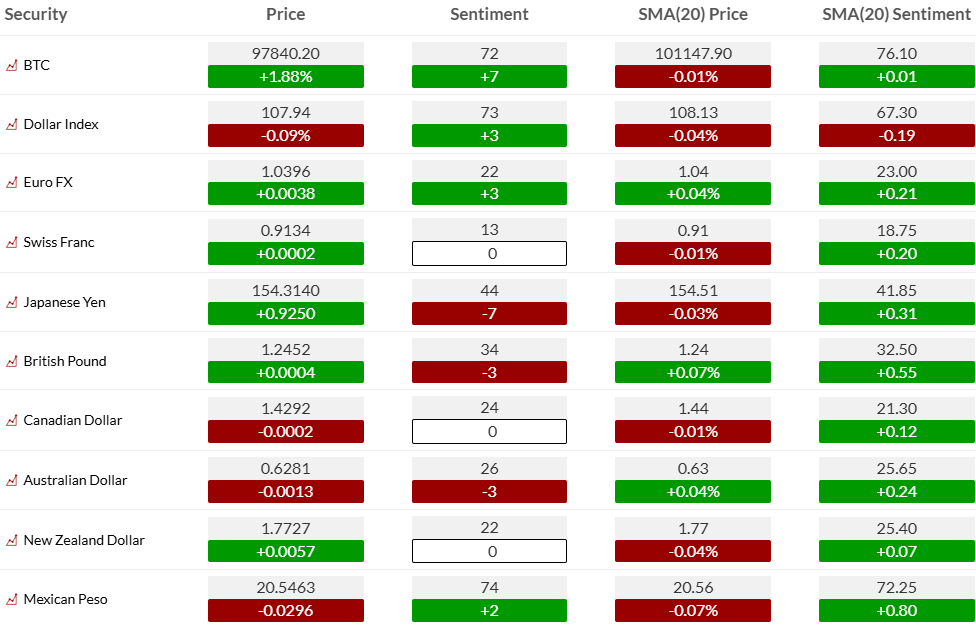

Currency bullish sentiment little changes

Commodity bullish sentiment saw energy weakness again with crude near recent lows. Copper was overbought in the short term and due for a pullback. I still like it on the long side.

US MARKETS

S&P futures 60-minute tactical time frame continues to trade in a choppy range which narrowed in the last two weeks. 6000 is the first support and the short term breakdown level as GS Rubner mentioned yesterday.

S&P futures daily sideways since November in range bound markets.

Nasdaq 100 60-minute tactical time frame shows the top end of the recent range with support at ~21,600

Nasdaq 100 futures daily at top end of recent range

Extra charts we’re watching

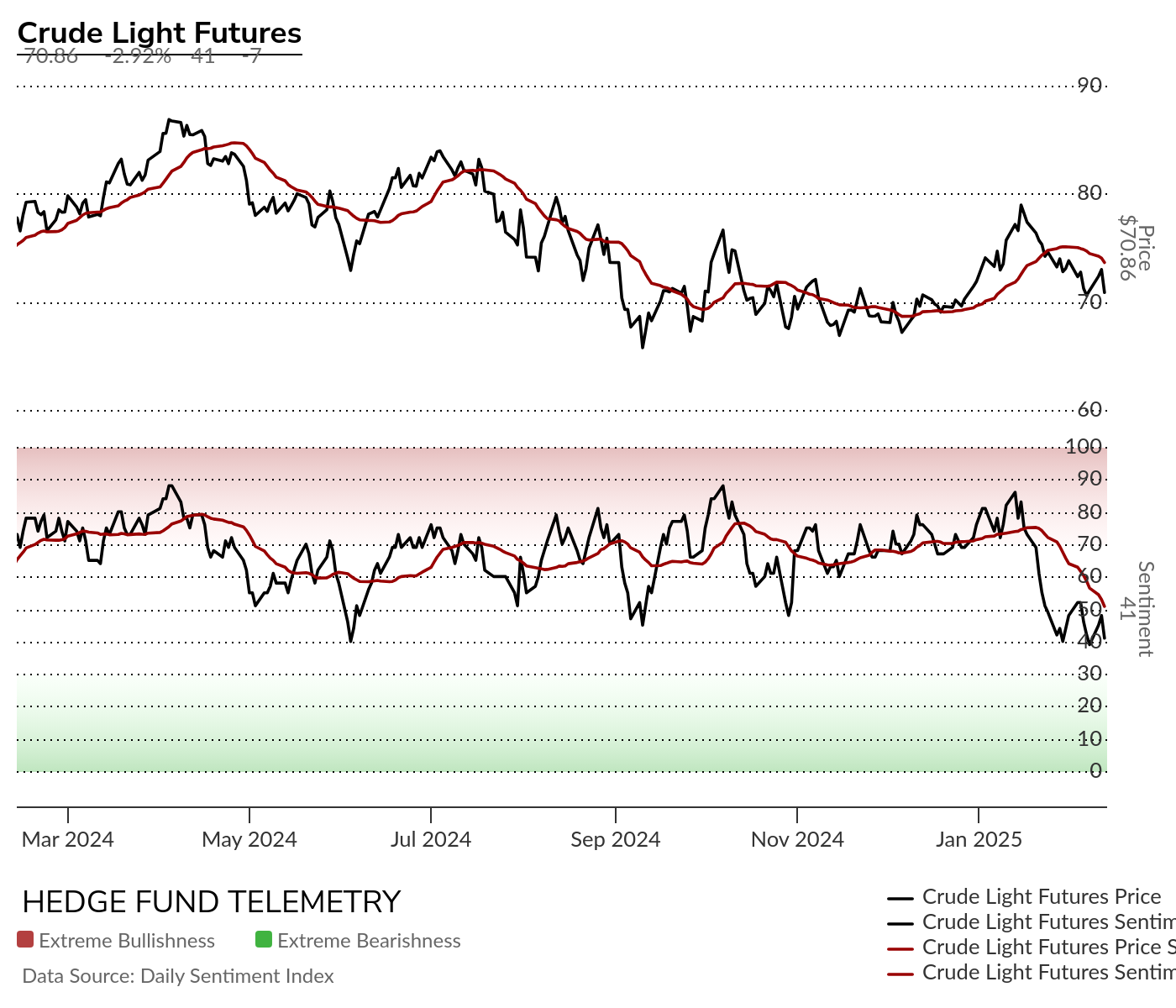

Crude has struggled for a while now after short lived bounces. The 50 day and 200 day are nearly equal at 71.90 and if price is going to work on the upside a move over those levels is needed and holding the TDST Setup Trend support.

Crude bullish sentiment at support seen last summer and recently at 40%.

US Dollar Index daily with recent DeMark Sequential sell Countdown 13. There is the elective 8 vs 5 setting for the Sequential that could see it move one more time higher too. Breaking down below recent low (wave 1 in yellow) could move this to wave 3 price objective of 105.77

US 10-Year Yield with a sharp spike higher yesterday backing off a little ahead of the PPI report this morning

Bitcoin Daily continues to slip holding the 95k level with bigger support at 90k

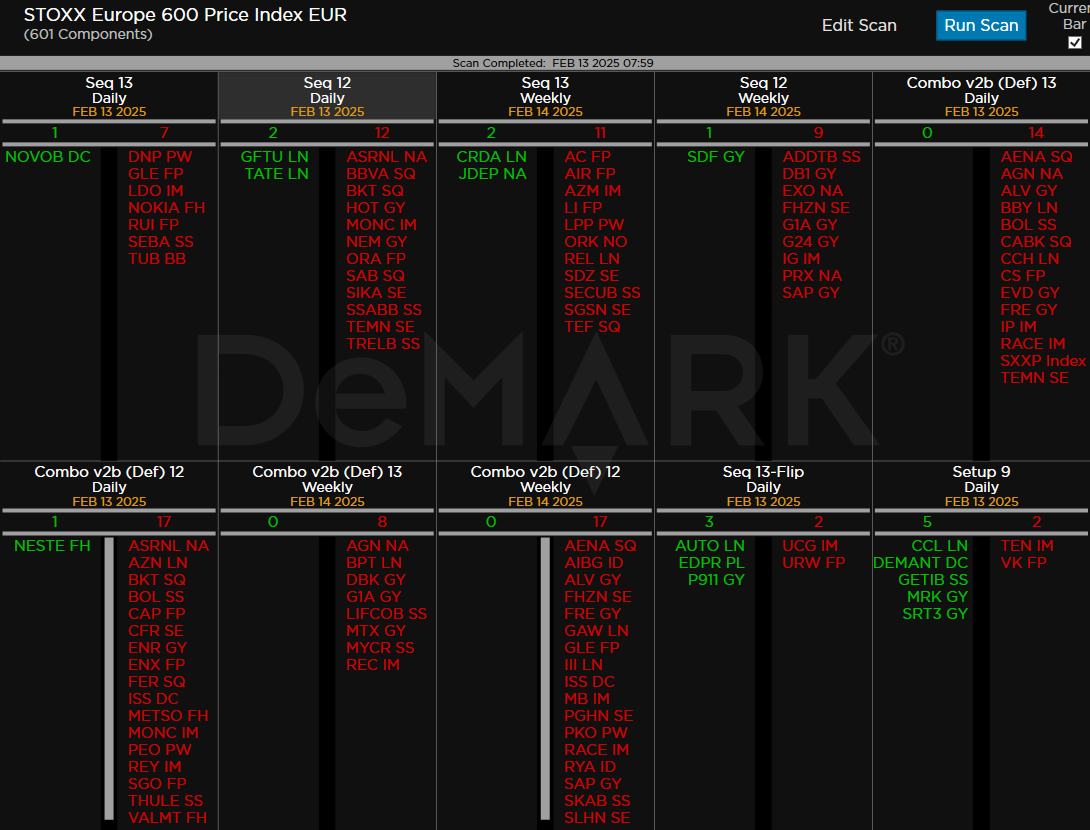

DeMark Observations – Euro Stoxx 600