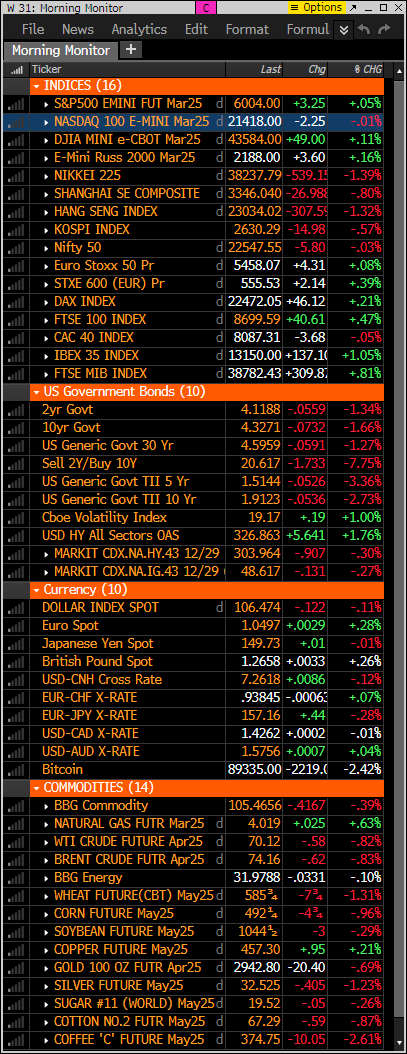

- S&P and Nasdaq futures little changed in Tuesday morning trading. Comes after US equities finished mostly lower on Monday with tech the worst performer, down over 1%, and Mag 7 falling to lowest level since early December. AI capex plays, China ADRs, EVs, builders, machinery, rails and trucking some of the laggards. Healthcare, insurance and travel/leisure among the better performers, while ~60% of the S&P 500 managed to finish in the green. Treasuries seeing strong gains across the curve. Dollar index down 0.1%. Gold down 0.8%. Bitcoin down 2.5% with crypto broad weakness. WTI crude off 0.6%.

- Trade Ideas Sheet: HD top line earnings were fine but guidance was light. It’s up about 0.5% and I will hold my small short for now.

- Short term, I could see a bounce attempt. However, breadth will need to stay strong all day, and mid-day weakness avoided. Late day selling has been happening recently and they say the last hour sellers are the smart money. There has been a lot of risk on, risk off intraday moves in 2025.

- Several moving pieces in play. Trump 2.0 policy uncertainty still seems to be an overhang with recent reiteration that tariffs on Canada and Mexico remain on track to go into effect next month, White House efforts to ramp up restrictions on chip exports to China (weighing on global semis) and the inability of House Republicans to reach a consensus on a reconciliation bill blueprint featuring that TCJA extension. However, market also still skeptical Trump will ultimately go full throttle on tariffs and continue to use tariff threats as more of a negotiating tactic. AI capex theme scrutiny another area of focus despite MSFT reiteration of its capex guidance. At the same time, NVDA expected to deliver another beat and raise tomorrow however concerns over Blackwell delays, Deepseek threat, data center slowing rumors might be brought up in conference call. Heavy retail selling on Monday also flagged following talk last week about waning buying momentum. Recent rate rally may be spun positively given extent to which Fed easing expectations have been priced out.

- Conference Board’s consumer confidence index, Richmond Fed manufacturing index, Case-Shiller 20-city home price index and FHFA house price index on the US economic calendar this morning. Confidence report expected to get some additional scrutiny following weakest University of Michigan consumer sentiment reading since November 2023 late last week. There is also a $70B auction of 5-year notes. Nothing on QT from Fed’s Logan, who called for caution on rate cuts. Fed’s Barr and Barkin scheduled to speak today as well. Washington in focus as well as House may vote on its reconciliation plan outline, though passage uncertain with concerns about cuts to Medicaid one of the bigger areas of concern.

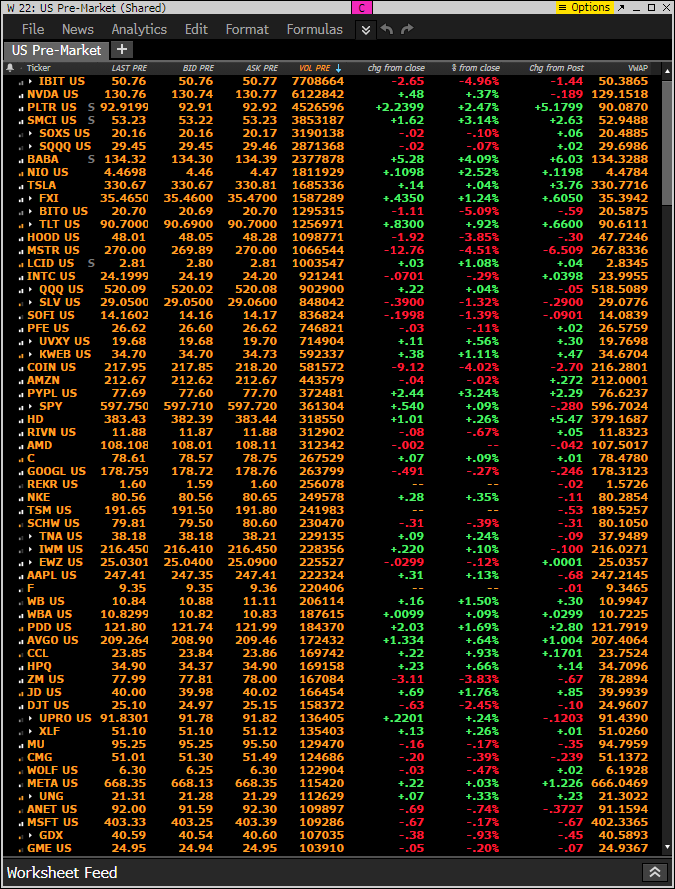

- NVDA reportedly seeing a jump in H20 orders from Chinese firms following DeepSeek breakthrough. HD Q4 better though FY25 guide light. Tesla’s sales in Europe plummeted 45% last month, with only 9,945 cars registered, while the overall EV market saw a 37% surge. LLY lowers Zepbound weight loss prices. ZM weaker with focus on limited on top-line growth. HIMS down big with concerns about 2025 outsized contribution from weight loss. ZION announced $40M share repurchase authorization. KBR Q4 and guidance better than feared given DOGE uncertainty. CLF FCF burn worse than expected. SONO announced $150M share repurchase program. UCTT missed and guided Q1 well below the Street. JACK announced CEO Darin Harris resigned. CHGG down big on much weaker Q1 guidance and noted it has commenced a strategic review process.

market snapshot

economic reports today

premarket trading

Crypto getting hit hard with many of these down 50% or more off highs. This is 24 hour pricing vs 5pm ET which I normally show on note.

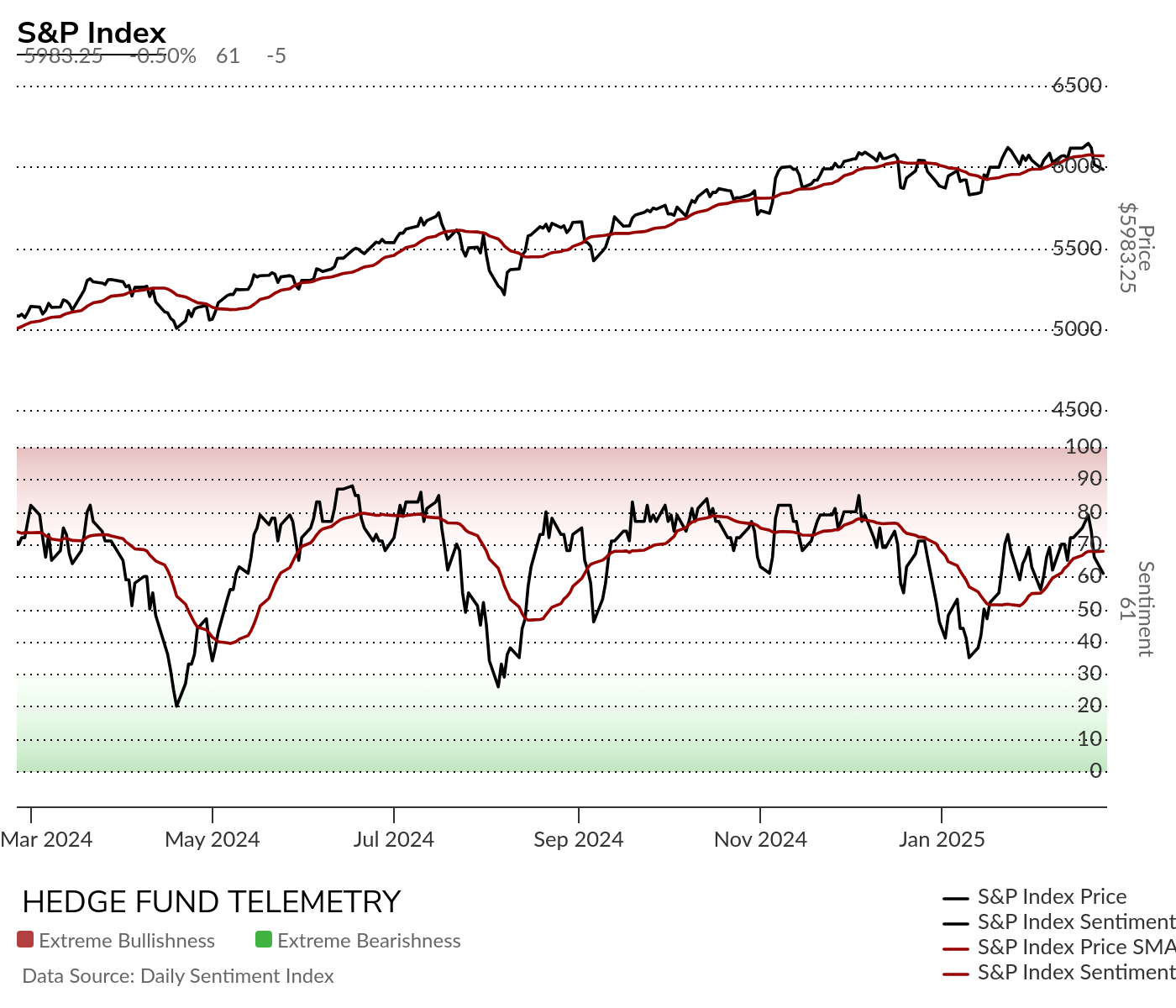

US MARKET SENTIMENT

S&P and Nasdaq bullish sentiment dropped again below the 20 day moving average of bullish sentiment. 50% midpoint majority line remains the important next level to watch. Breaking and holding below could see a deeper move to get oversold, which is something I’d like to see to increase confidence in buying.

Bond bullish sentiment another uptick. Chart below.

Currency bullish sentiment shows Bitcoin sentiment declining but still above the 50% midpoint majority line. Chart below.

Commodity bullish sentiment mostly a downside day

US MARKETS

S&P futures 60-minute tactical time frame has been moving under some support in February but above the early February low.

S&P futures daily back below the 50 day and holding the TDST Setup Trend at 5970. Breaking below (and holding below) could possibly see a test of the 200 day and possibly moving much lower in downside wave 3 below January wave 1 low) to 5680 the potential wave 3 price objective.

Nasdaq 100 60-minute tactical time frame with new DeMark Sequential and Combo 13’s. I could see a bounce attempt.

Nasdaq 100 futures 240 minute is a little concerning with a rare downside Sequential in progress – especially heading into NVDA earnings.

Nasdaq 100 futures daily down moderately early and under the 50 day again. Support at 21,000 where it bounced several times.

Extra charts we’re watching

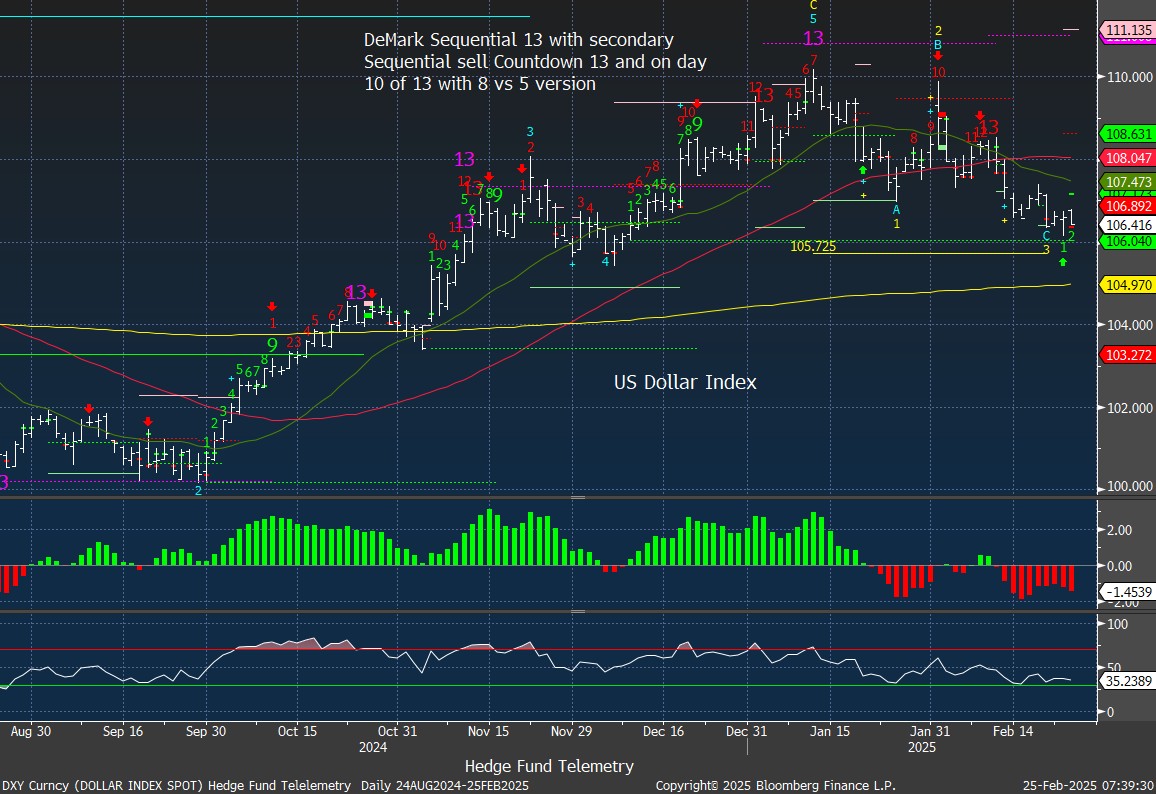

US Dollar Index daily remains weak trying to hold the TDST Setup Trend level at 106.04

US 10-Year Yield down again with Setup on day 5 of 9. Support at 200 day at 4.24% and TDST Setup Trend at 4.18%

Bond bullish sentiment still needs to make a higher high above 40% and even better over 50% the midpoint to signal a strong bond market move.

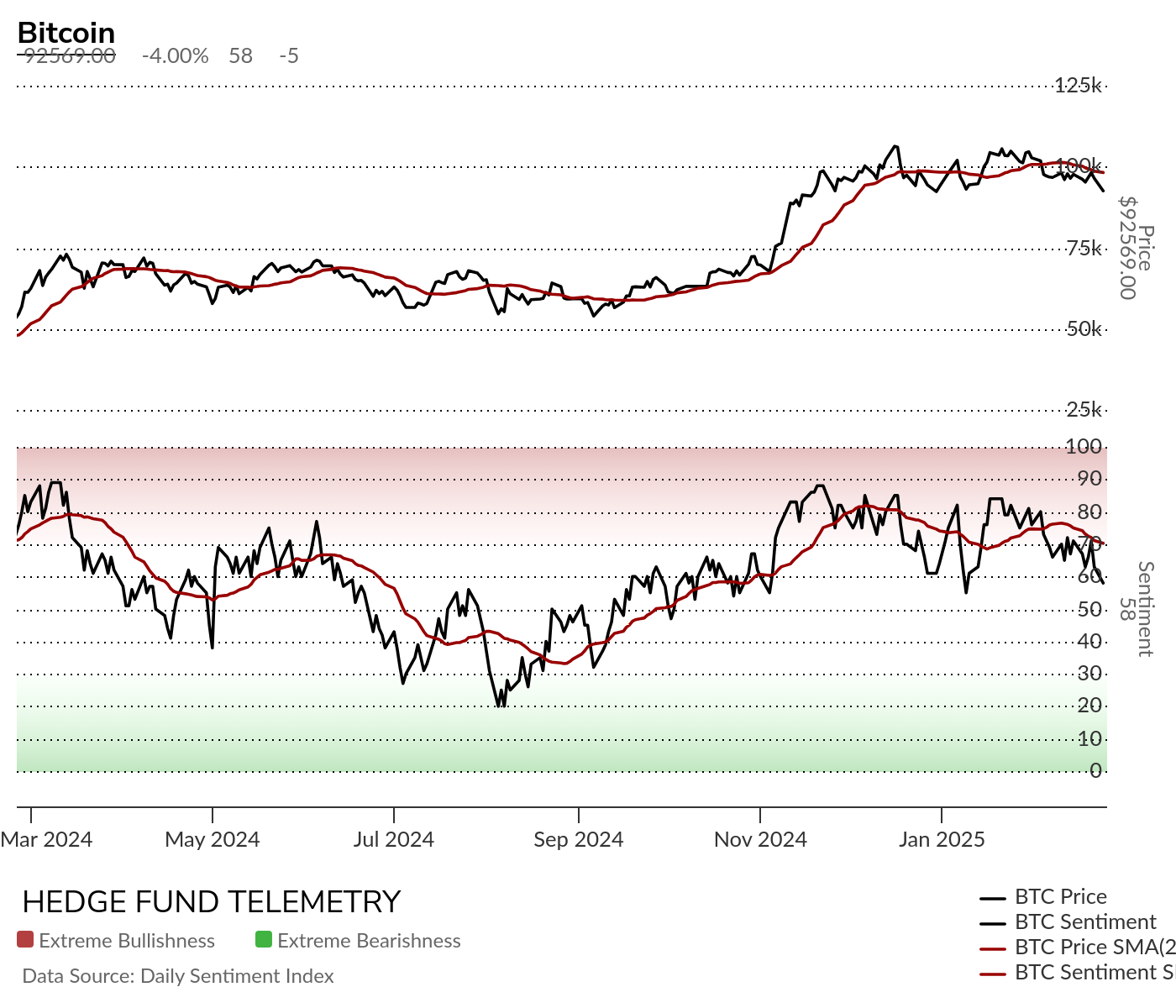

Bitcoin Daily broke the 90k level with crypto under pressure. There has been a downside Sequential in progress so it’s not a huge surprise. Sequential is now on day 5 of 13.

Bitcoin sentiment 20 day moving average has been declining. 50% will be the test.

DeMark Observations – Euro Stoxx 600

Continue high number of Sell Countdown 13’s