Market Setup

Risk is repricing lower ahead of a catalyst-heavy week, with macro and geopolitical inputs now converging. Positioning had been complacent (elevated sentiment across equities and commodities), but the sharp deterioration in Middle East stability alongside a volatility spike (VIX +13%) is forcing de-grossing yet volume has remained muted – no capitulation yet.

Sentiment has rolled hard but not fully capitulated:

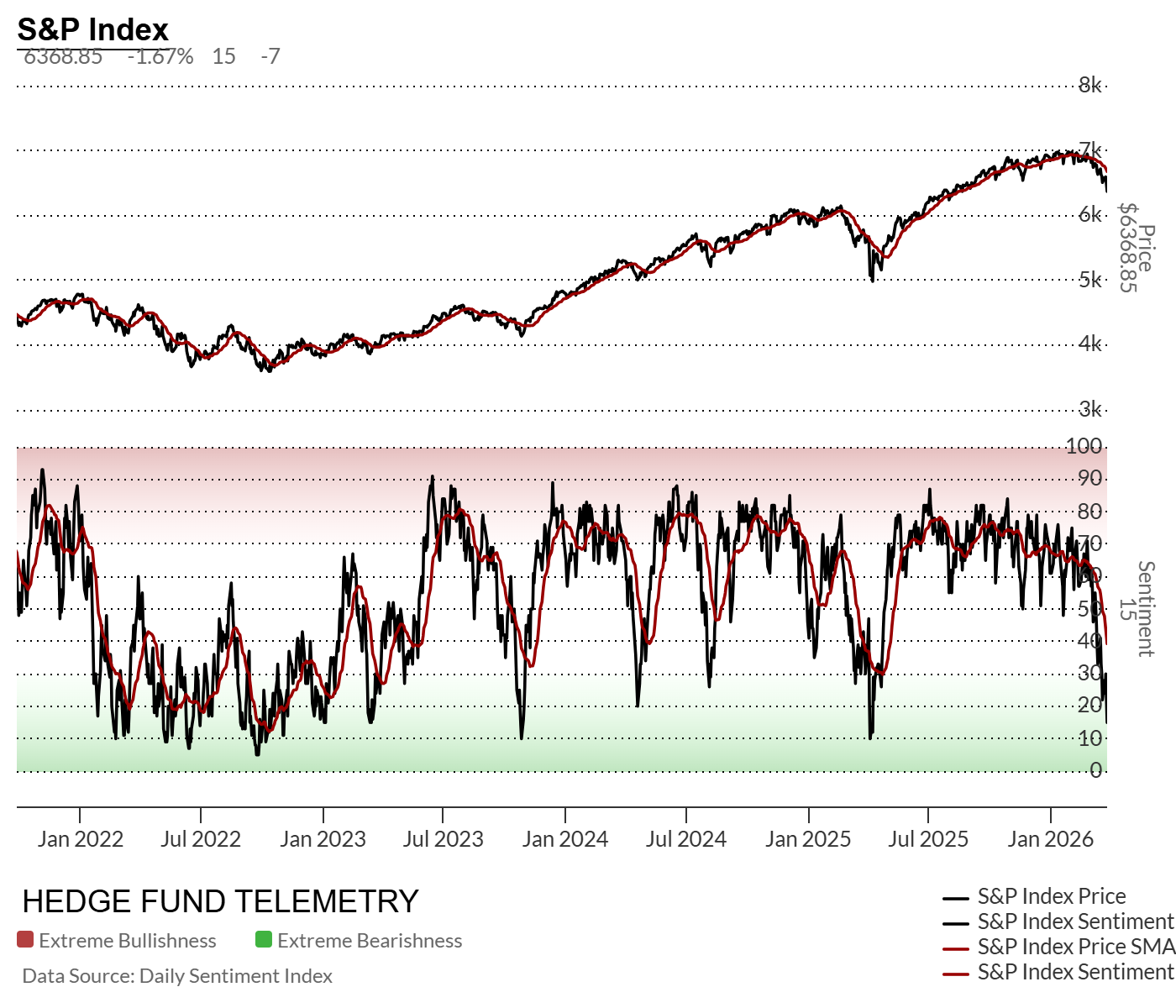

- S&P sentiment: 15 (↓7 d/d) → in extreme territory (<20)

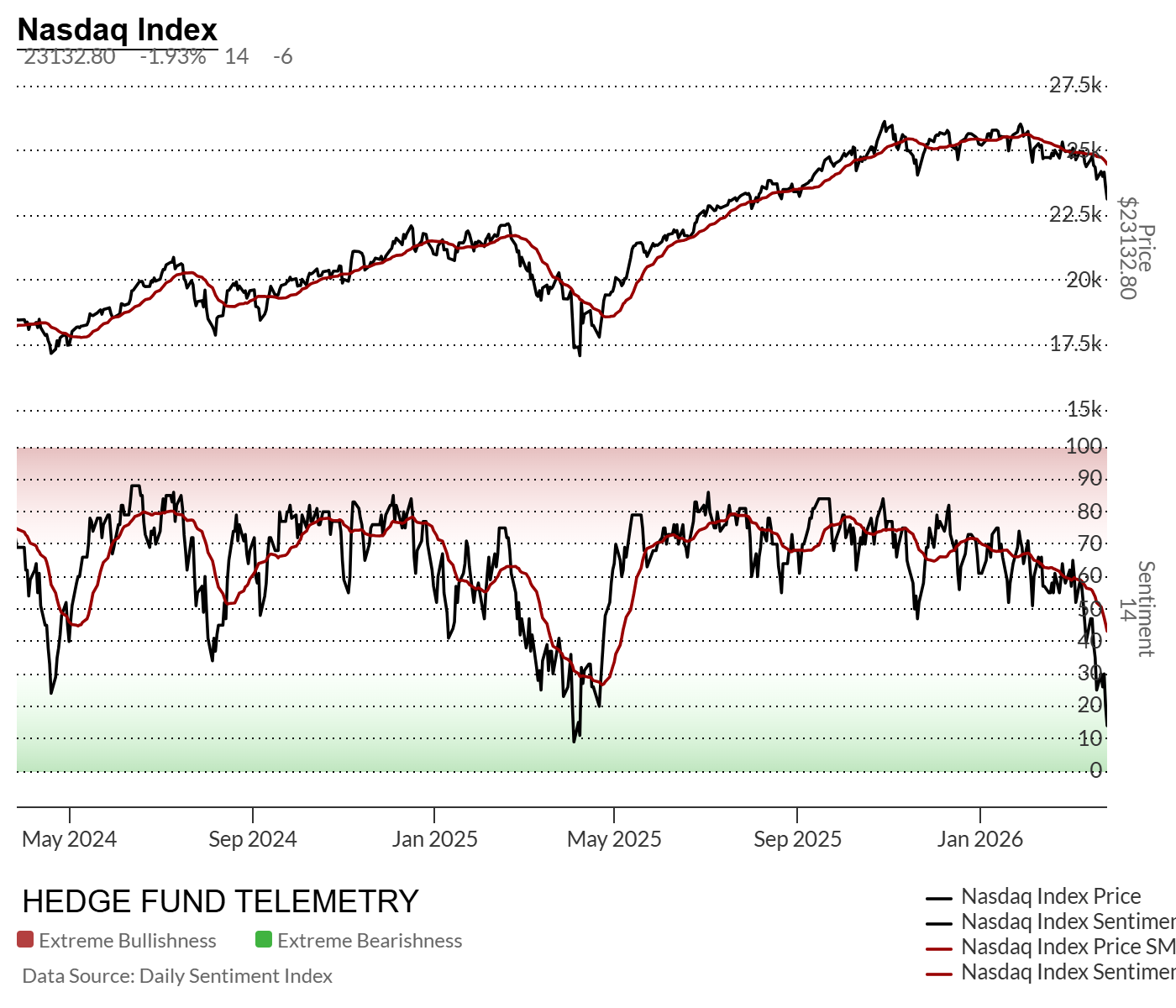

- Nasdaq sentiment: 14 (↓6 d/d) → same setup

- Both are now well below 20-day averages (~40+), signaling downside momentum but also building conditions for reflex rallies

- DeMark Sequential and Combo Countdowns in progress with both equities and bonds, a dangerous situation.

- A look at market internals below

Rates backing up + USD firming → tightening financial conditions into growth-sensitive data.

This is a high-velocity tape: macro + geopolitics + positioning unwind.

THE BIG PICTURE INTERIM NOTE WILL BE OUT EARLY THIS EVENING. Thank you with gratitude to all who signed up.

Designed for investors who think like portfolio managers, not day traders. Best suited for:

- Hedge funds

- Professional traders

- Asset allocators

- Family offices

- Serious individual investors

$250 / year or $400 for a two-year discount option Use this link to sign up now.

This is the introductory pricing for the first 1000 subscribers. I have also been told I have underpriced this, so I can and will raise prices in the future. If you sign up for the introductory price offer, it will renew at this price for life.

The focus will shift between equities, macro, rates, commodities, and currencies depending on where the most important opportunities and risks exist. If you have any questions, please email.

Key Catalysts for the Week Ahead

Market Structure

- Positioning unwind accelerating after complacency peak (equities + commodities)

- Volatility regime shifting higher (VIX 77 sentiment, +10 d/d)

- Systematic CTA strategies likely reducing exposure into weakness

Macro Data

- ISM Manufacturing (Wed): Directional signal on growth re-acceleration vs. stall

- Payrolls (Fri): Critical after prior weak print (-92K → Street +50K)

- REMEMBER MARKETS WILL BE CLOSED FRIDAY WITH JOBS DATA RELEASE

- I believe US futures will be open – need to confirm.

- JOLTS / Confidence / Retail Sales cluster → labor + consumption trend clarity

Central Banks / Policy

- No major Fed decision, but data will reprice rate path expectations

- Inflation prints (Tokyo, Eurozone CPI) → global policy divergence risk

Geopolitics

- Middle East escalation broadening (Iran + proxies + Houthis)

- Key risk: Hormuz + potential Bab al-Mandab disruption expansion

- Oil shock now feeding into inflation + growth tradeoff

Sector / Idiosyncratic

- Tesla deliveries (key sentiment driver for growth/AI complex)

- Defense, energy, shipping → leadership vs. tech/growth fragility

Earnings Calendar

Monday

Post-Market: RZLV – Rezolve AI; FTHM – Fathom Holdings; PRGS – Progress Software

Tuesday

Pre-Market: FDS – FactSet; MKC – McCormick; SNX – TD SYNNEX

Post-Market: NKE – Nike; PLAY – Dave & Buster’s; RI – Peregrine; PVH – PVH Corp

Wednesday

Pre-Market: CAG – Conagra; CALM – Cal-Maine; LW – Lamb Weston; MSM – MSC Industrial; TLRY – Tilray

Thursday

Pre-Market: AYI – Acuity Brands; ANGO – AngioDynamics; CCG – Cheche Group; LNN – Lindsay Corp

Friday

Markets Closed (Good Friday)

Economic Calendar

Monday

Tokyo CPI (Mar); China NBS PMIs (Mar)

Tuesday

Eurozone CPI (Mar); JOLTS; Consumer Confidence; Chicago PMI; API Crude; FHFA House Price Index

Wednesday

ADP Employment; ISM Manufacturing; Retail Sales; PMI Manufacturing Final; Business Inventories

Thursday

Initial Jobless Claims; Continuing Claims; Challenger Job Cuts; Trade Balance

Friday

Nonfarm Payrolls; Unemployment Rate; Avg Hourly Earnings; ISM Services; PMI Services Final

REMEMBER MARKETS WILL BE CLOSED WITH JOBS DATA

What We’re Watching This Week

- Do equities hit true capitulation (<20 sentiment) or stabilize above it?

- Volume has been light which needs to show spike for capitulation

- Oil reaction to geopolitics: continuation vs. exhaustion (crowded long)

- Labor data (NFP): confirms slowdown vs. false alarm

- ISM + global PMIs: growth re-acceleration vs. stall

- VIX behavior: spike-and-fade vs. sustained regime shift

Bottom Line

This is a transition week: from complacency → instability.

Positioning is unwinding, but not yet washed out. That creates a two-way tape:

- Near-term downside risk persists (macro + geopolitics + positioning)

- DeMark Sequential Countdowns on the downside in progress with equities

- DeMark Sequential Countdowns on the upside in progress with Treasury rates

- Internals are moving to oversold levels but are not quite there yet

- And sentiment is approaching levels where tactical longs become viable

The key is sequencing:

- Weak data + escalation → further downside

- Stabilization (or de-escalation) → sharp reflex rally given positioning reset

This is no longer a low-vol grind — it’s an inflection environment.

Weekend News

- Primary Geopolitical Themes

- Conflict expanding: Iran + proxies (Iraq, Yemen) increasingly active

- Houthis entering conflict materially raises global shipping disruption risk

- US military posture escalating (troop deployments, planning scenarios)

- Macro Policy Signals

- Oil supply shock risk remains non-linear (Hormuz + potential second chokepoint)

- Saudi pipeline at capacity → limited offset capacity

- Market now pricing stagflationary impulse risk

- Sector / Single-Stock

- Energy bid + crowded (Crude sentiment 85, already extreme)

- Metals bid but lagging trend vs. SMA → late-cycle participation

- Crypto/Bitcoin weak → risk appetite deterioration signal

Charts we are watching

The S&P 500 daily has had a rolling top from October, with the rolling part starting this month. This has broken all of the levels I’ve been highlighting and has a DeMark Sequential on day 7 of 13 and Combo on day 9 of 13. On the Big Picture interim note I will have more time frames with some updated levels to watch as I expect further downside ultimately.

The S&P 100 has a rolling top as well with the Sequential only on day 3 of 13 and Combo on day 7 of 13. The S&P 100 is more correlated with the Nasdaq 100 since the meat of the market mega-caps dominate this index as well.

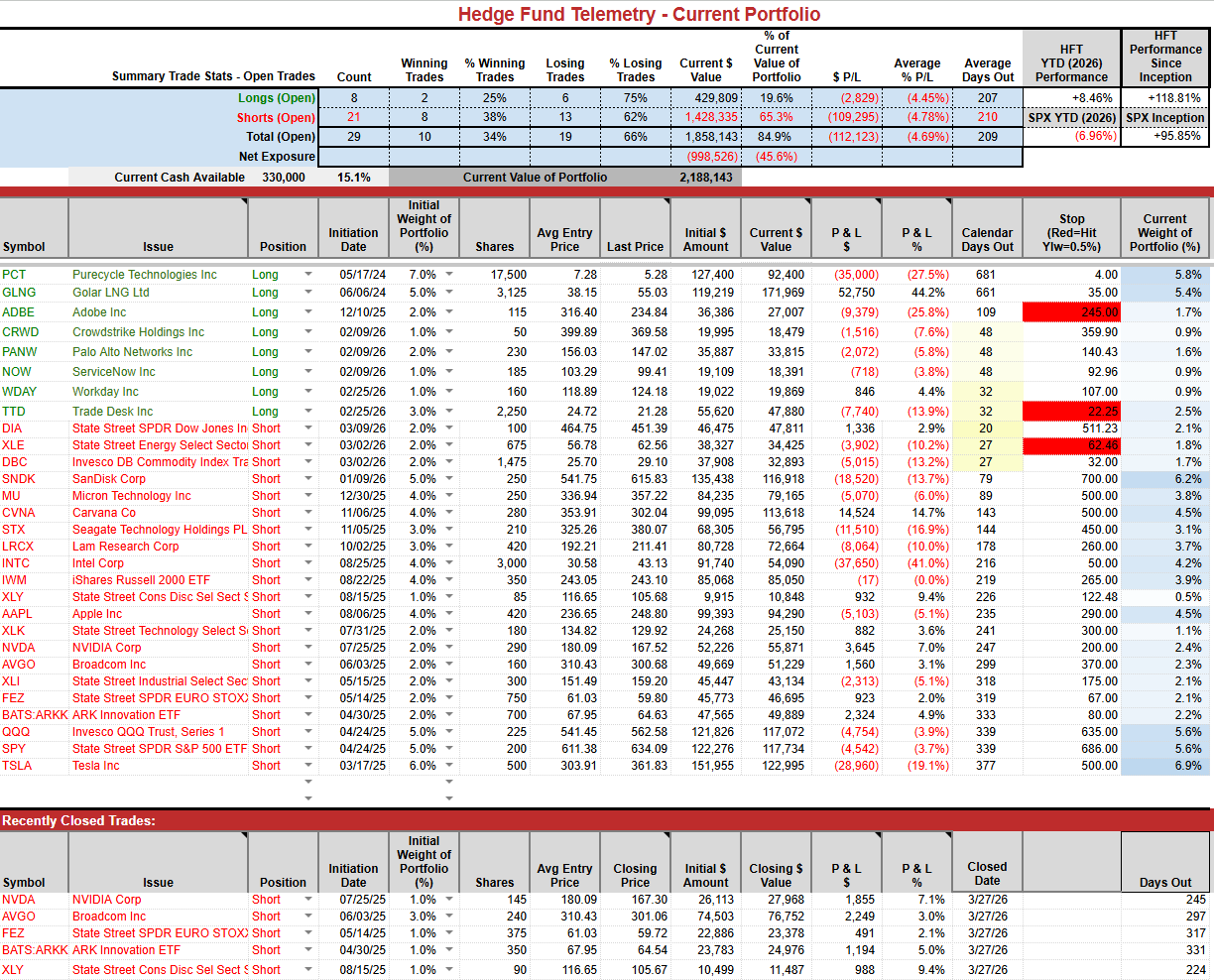

Portfolio update

Updated with the recent covers from Friday. Very pleased with the overall PNL and still believe the tech shorts have more downside risk due to the continued high concentration. PANW CEO bought $10 million worth of stock on the recent drop. The software longs have positive insider buying/option grants, which keep me long these. I plan on adding to XLE and DBC if peace breaks out and have started building a list of names I want to buy. There is one mega-cap on that list; I might add it this week.

Internals – update

Internals are moving towards oversold levels; however, on balance, it’s not quite at the levels that would signal a buying opportunity, much like we have spotted in the past.

Whippy action from earlier in the week saw the advance-decline data increase and then fall. There were some hoping for a Zweig breadth thrust, but that didn’t confirm. I’d like to see these get to 30% or lower for a clear buying opportunity.

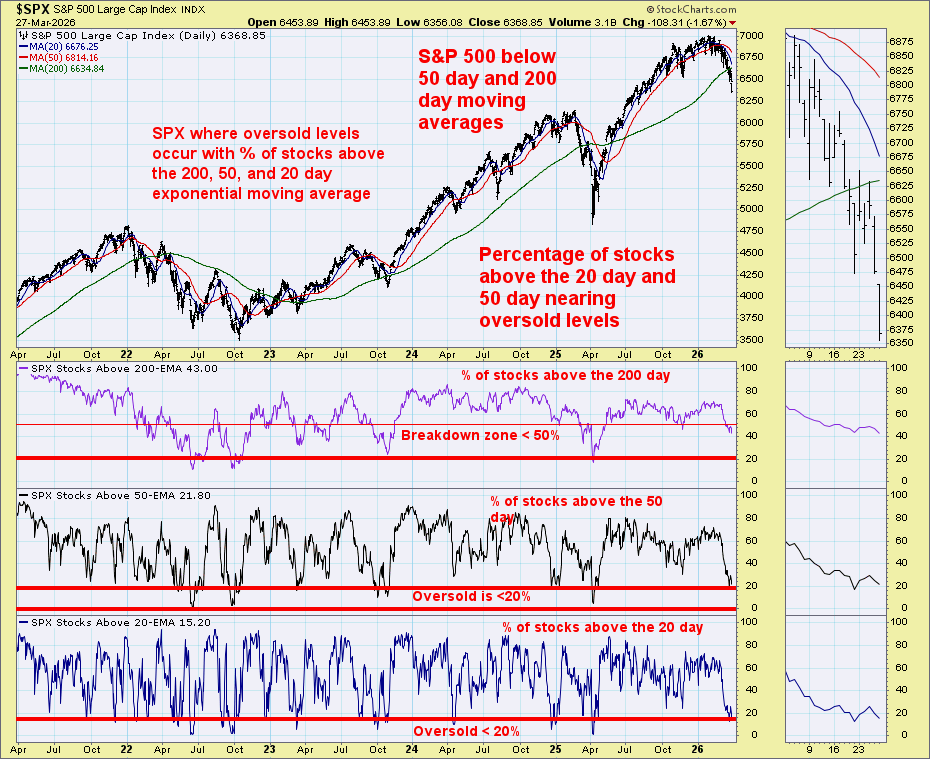

One of the simplest internals I watch is the percentage of stocks above the 20-, 50-, and 200-day moving averages. After steady action holding around 60% they finally broke with the 20 day and 50 day just at the oversold level but as we have seen in the past they can and might go even lower. When the 200 day percentage gets under 50% it confirms it is a serious pullback

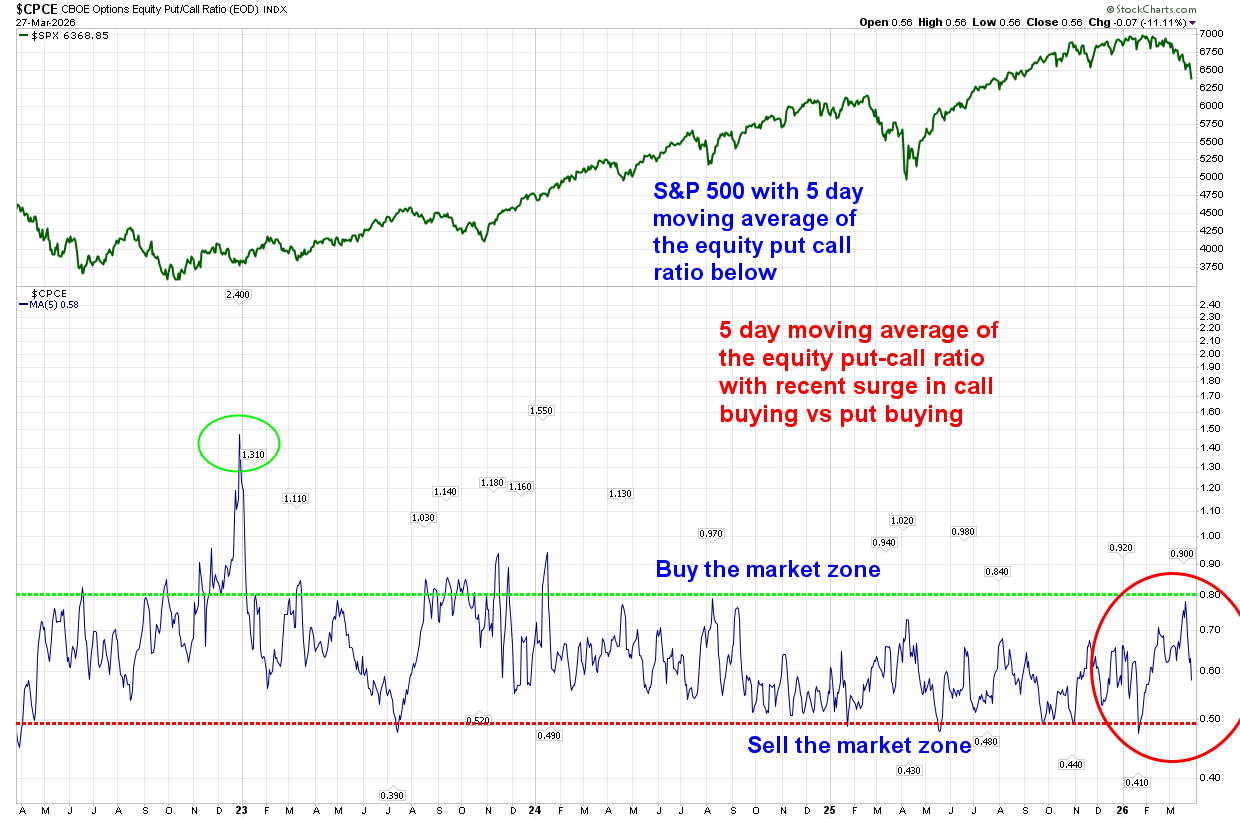

The 5-day moving average of the equity put-call ratio dropped sharply this week, indicating a shift from recent heavy put buying to call buying. I figure it was the start of the week, with Trump’s de-escalation comments, that lured call buyers back only to get hammered later in the week. This could also have put pressure on the markets, with call buyers unwinding their bullish bets. I’ll update this during the week to see if the rolling 5-day changed, which I bet it did.

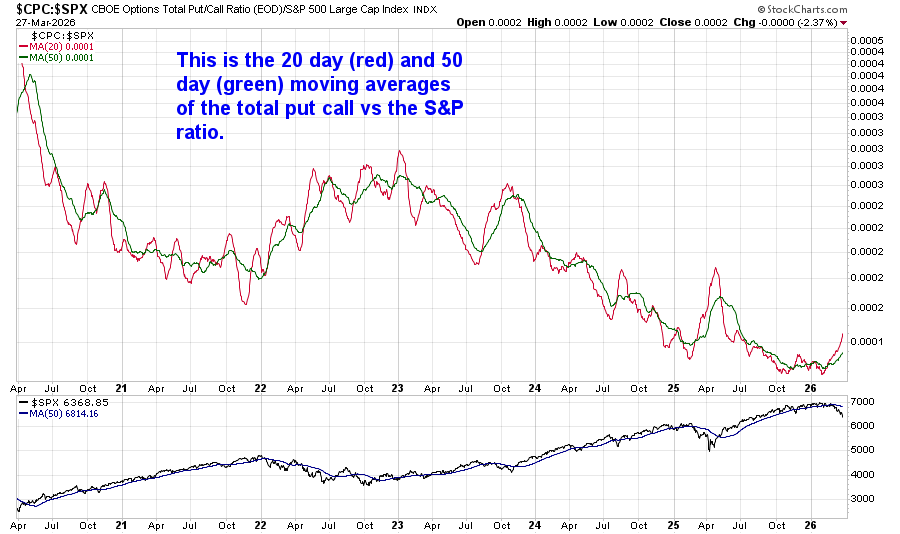

The put-call vs. S&P ratio 20-day moving average has started to turn and doesn’t reflect the near-term 5-day call buying. Could this be similar to the 2022 period when this lifted for a year with a bear market? Time will tell.

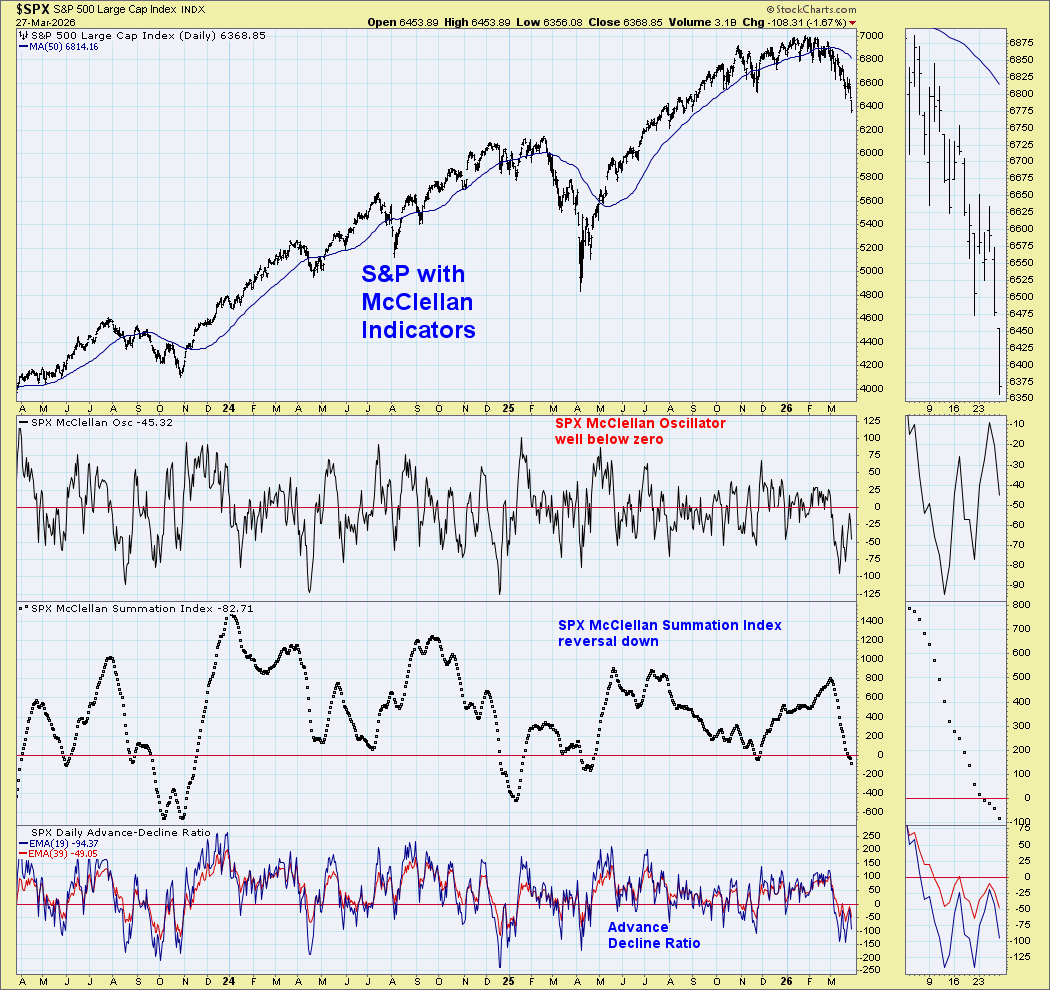

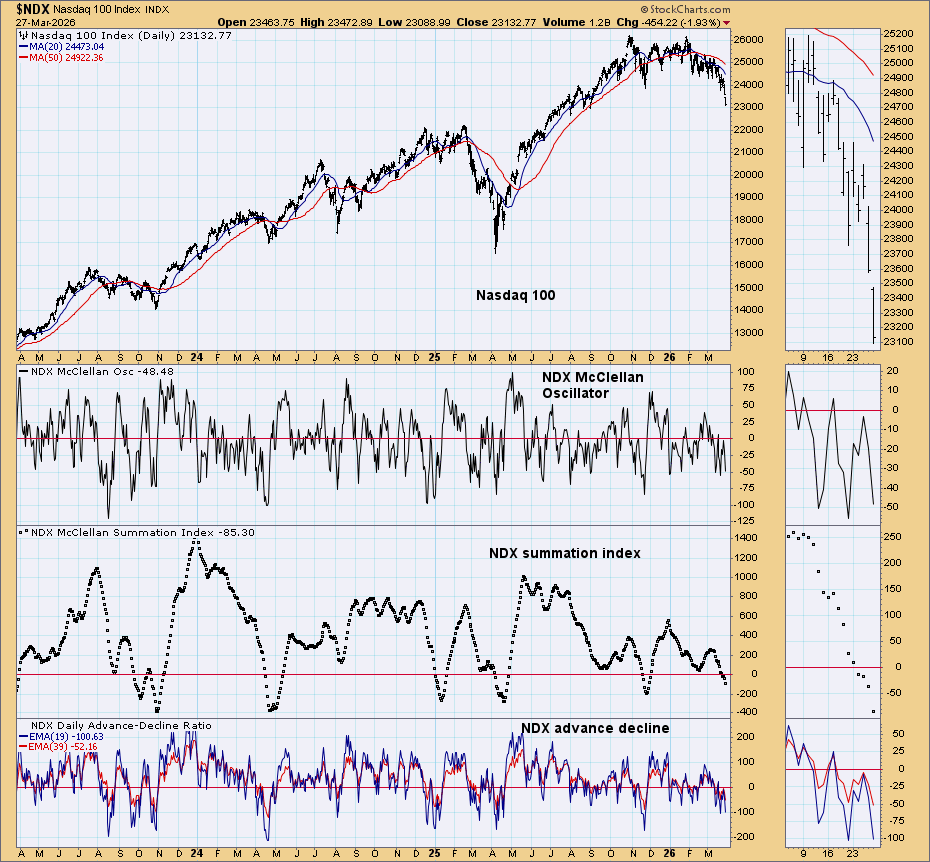

The S&P and Nasdaq 100 with McClellen indicators are moving lower despite a near-term lift with the Oscillator and A/D data. The Summation Indexes are both below zero and could move lower before a bottom is found.

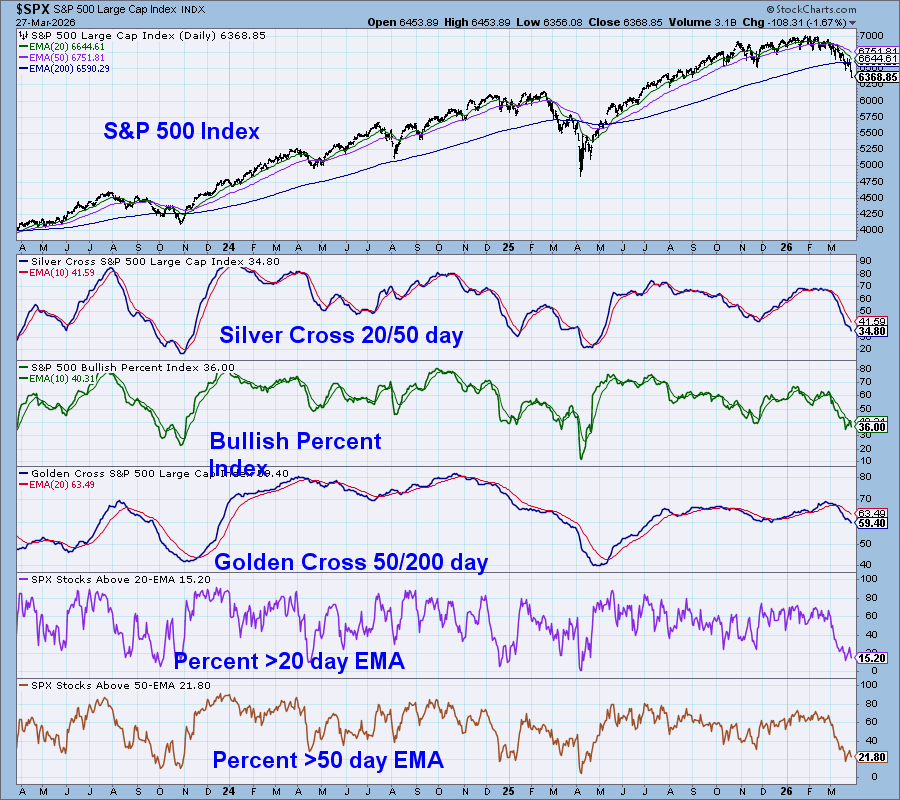

This has an assortment of some of the indicators combined together for the S&P. The Silver Cross data is dropping (see below) while the Bullish Percent Index is at 36% with some other market declines seen bottoms at lower levels (also see below). The Golden Cross 50 day crossing below the 200 day is at 59% and has room and time to see lower levels. The exponential moving averages of % above the 20 and 50 day are getting to oversold levels – exponential MA’s weight near term action vs Simple Moving Averages – shown above.

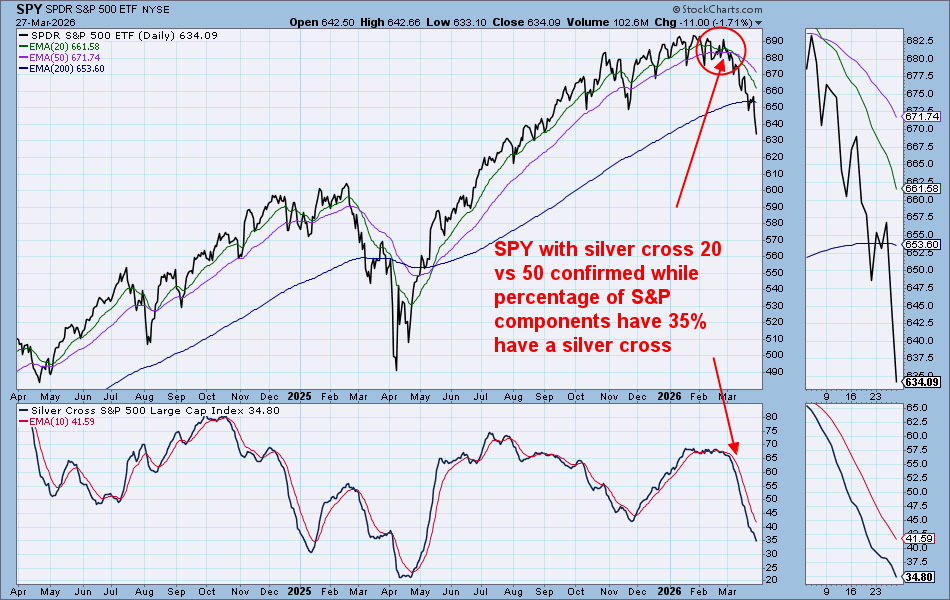

This shows a close up of the Silver Cross 20/50 day moving average cross. The last few weeks finally started to see more stocks breakdown with the cross.

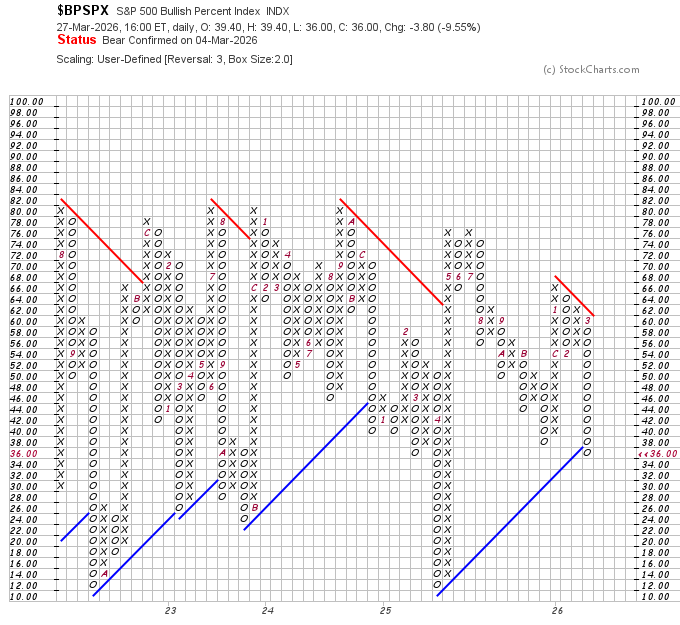

The S&P Point and Figure Bullish Percent Index is making a new low and is at 36% in a column of O’s which is bearish. This level is the lowest level going back to last April/May. For more info on Point and Figure Bullish Percent Indexes click here.

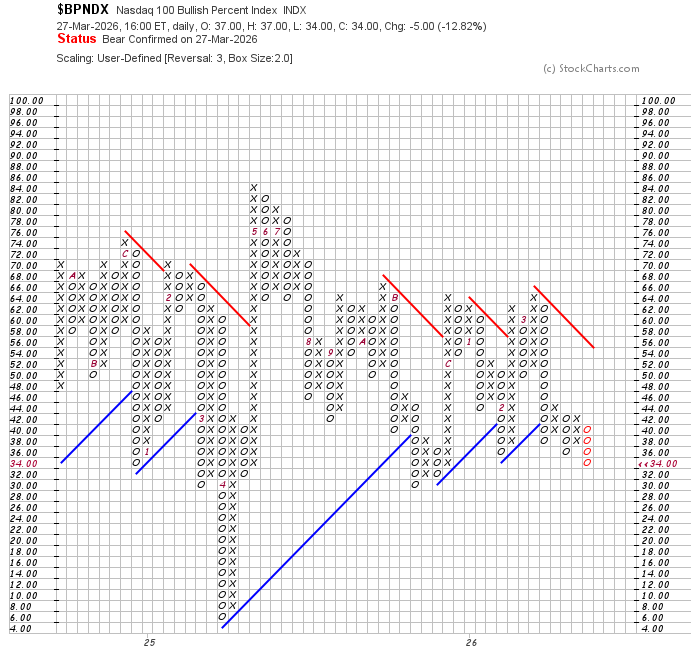

The Nasdaq 100 Bullish Percent Index is also making a new YTD low in a downside column of O’s. The 30% level has been a lever where there is some support, except that if it breaks, it could be similar to a year ago, when it moved to a crash-like level at 6%.

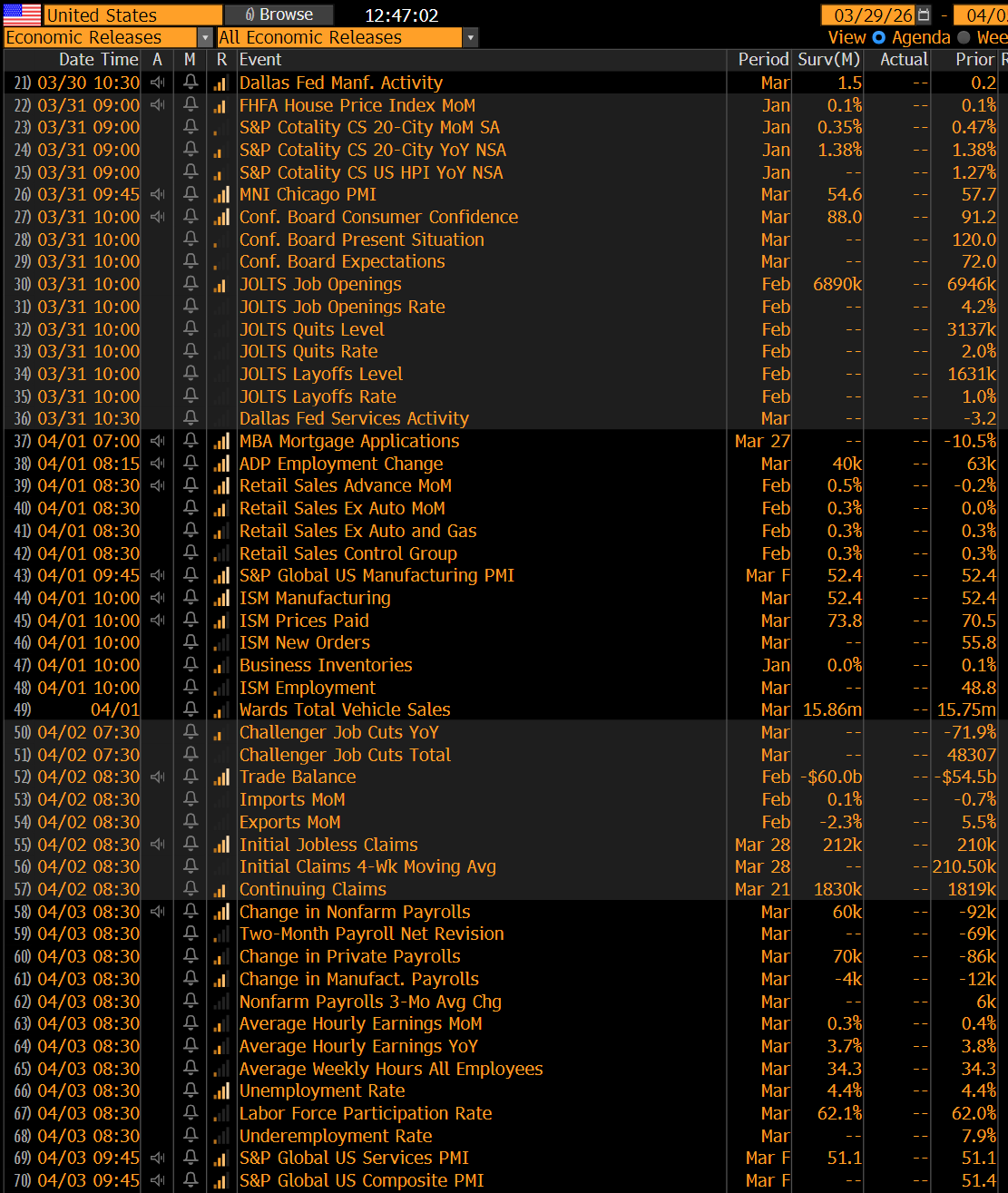

US economic data for the week

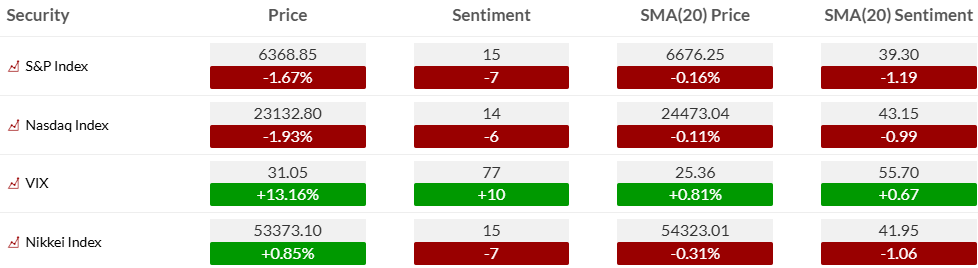

KEY MARKET SENTIMENT

Equities

- Rapid deterioration but not yet full capitulation

- Key level: <20 confirms exhaustion / tactical low setup

- Current setup: downside momentum + approaching reflex zone

I adjusted the time period for both S&P and Nasdaq bullish sentiment – which you can do on the site too. Sentiment is a condition and not by itself a trigger. It might move into a period like 2022 when sentiment remained mostly under 50% with bounces and fails – bear market behavior. The internals and DeMark indicators aren’t giving vibes of a V-bottom.

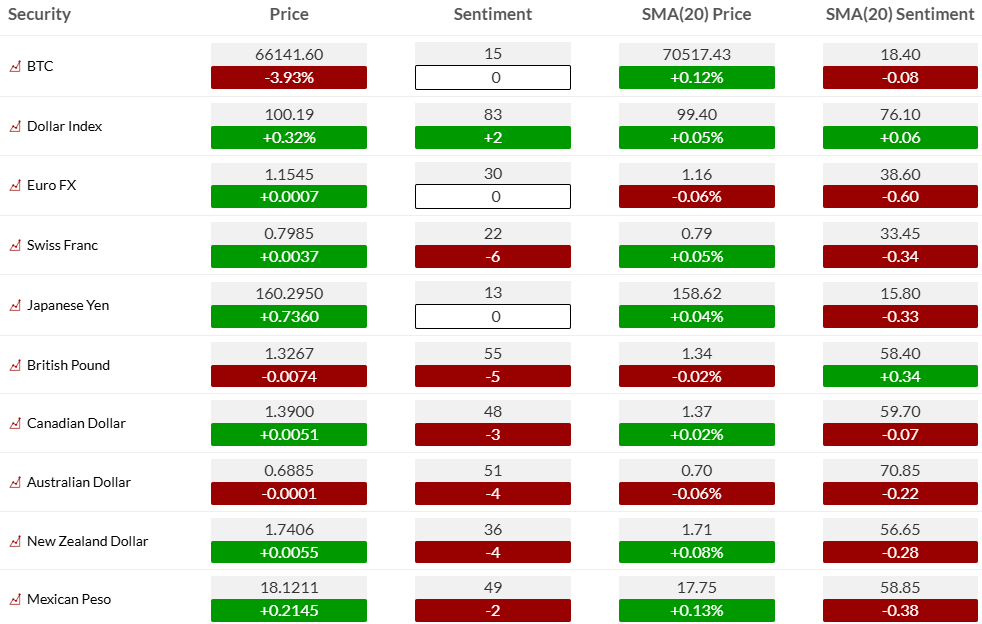

Treasury Rates

- Bond sentiment still moving lower with 30 year at 28% bulls → DeMark Sequential Countdowns in progress on the upside with rates

- No capitulation levels yet

Currencies

- USD continues firming now in the extreme zone at 83%

- Bitcoin remains oversold at 15% bulls yet it’s been in depressed zone from November –

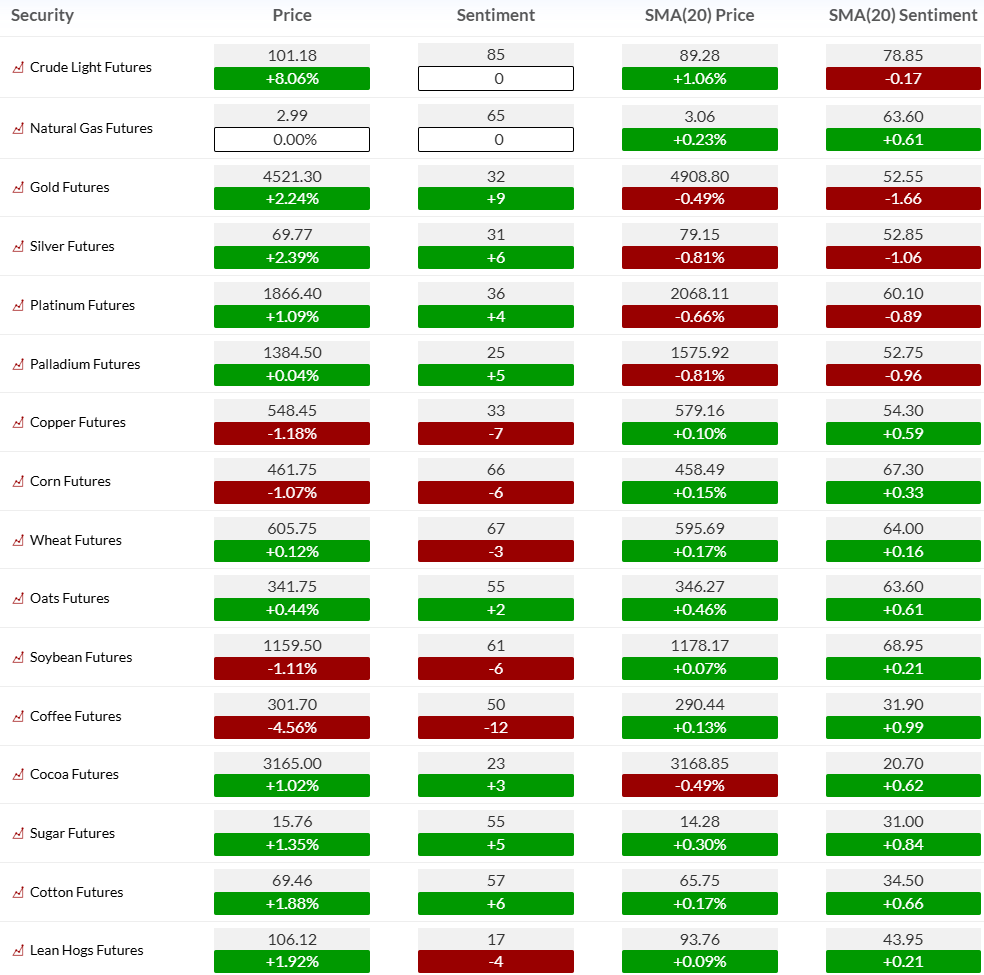

Commodities

- Crude extremely crowded (85 sentiment unchanged) → asymmetric risk if de-escalation

- Broad commodities saw some bounces but mostly below the 20-day moving average of bullish sentiment → weak trend quality

- Metals bounced on Friday, led by Gold

EARNINGS, CONFERENCES, AND ECONOMIC REPORTS

- Monday 30-Mar:

- Corporate:

- Earnings:

- Pre-open: BCAX, CBAT, FRMI, IMSR, NA, NMRA, PAVM, PDSB, RZLV

- Post-close: AIRJ, BLNE, CVV, DFDV, FTHM, HQI, HSDT, INLX, INMB, INV, LTRN, LVLU, PHR, PRGS, RNXT, SGMO, SPCE, SPRU, ZSPC

- Brokerage Conference:

- American Academy of Dermatology Meeting

- American College of Cardiology Scientific Conference

- Natixis Utilities Fixed Income Day

- World Vaccine Congress

- Earnings:

- Economic

- Europe: PPI y/y, Retail Sales y/y, KOF Leading Indicator, BoE Mortgage Approvals, M4 MoneySupply m/m, Economic Sentiment Indicator, CPI y/y, Preliminary CPI y/y, PPI m/m

- Asia: Industrial Production m/m, Unemployment Rate, CPI Tokyo y/y, Industrial Production m/m (preliminary), Retail Sales y/y, Retail Sales m/m, Non-Manufacturing PMI y/y, official Manufacturing PMI y/y.

- Corporate:

- Tuesday 31-Mar:

- Corporate:

- Earnings:

- Pre-open: AIRO, AMS, BKYI, CHA, CSAI, DTST, ELWT, FDS, FRMM, IMNN, INKT, JFIN, JILL, LNSR, MKC, PRPL, PVLA, SLSN, SNX, TE, TONX, TOYO, XTNT

- Post-close: AUID, BCHT, BHST, BIRD, BNZI, BRFH, BTBT, BYND, GENK, NCNO, NKE, NNDM, NWTG, NXGL, PLAY, PROP, PVH, REKR, RILY, SIDU, SPWH, VENU

- Analyst/Investor Events: PWR, HSY, RGLD

- Brokerage Conference:

- American Academy of Dermatology Meeting

- World Vaccine Congress

- Van Lanschot Kempen European Real Estate Seminar

- Wood EME NYC Conference

- Kepler Cheuvreux Aerospace & Defence Conference

- John Tumazos Very Independent Research Virtual Conference

- PDUFA: 4523.JP (INQOVI), 500124.IN (Reditux), ACAD (DAYBUE STIX), ARGX (VYVGART HYTRULO), ASND (SKYTROFA), AZN.LN (Calquence), AZN.LN (IMFINZI), bentracimab, GSK.LN (Penmenvy), GSK.LN (Shingrix), LLY (OMVOH), LLY (ZEPBOUND), NVCR (Optune (device)), TALICIA, TEVA (PONLIMSI), Tolebrutinib

- Earnings:

- Economic

- US: Redbook Chain Store, FHFA House Price Index, Chicago PMI, JOLTS, Consumer Confidence, API Crude

- Canada: GDP m/m

- Europe: Final GDP y/y, GDP SA y/y (final), Nationwide House Price Index y/y, Retail Sales y/y, Consumer Goods Spending m/m, PPI m/m, Preliminary CPI y/y, Unemployment Rate, Flash CPI y/y

- Asia: Housing Starts y/y, Tankan Manufacturing Index, Tankan Non-Manufacturing Index, Trade Balance

- Corporate:

- Wednesday 01-Apr:

- Corporate:

- Earnings:

- Pre-open: CAG, CALM, LW, MSM, NKLR, TLRY

- Post-close: BSET, FC, PENG

- Analyst/Investor Events: MP

- Brokerage Conference:

- World Vaccine Congress

- Earnings:

- Economic

- US: MBA Mortgage Purchase Applications, ADP Employment Report, Retail Sales ex Autos, Retail Sales, PMI Manufacturing Final, Business Inventories, ISM Manufacturing Index

- Europe: Retail sales y/y, Manufacturing PMI, SVME PMI, Unemployment Rate, Unemployment rate

- Asia: CPI y/y

- Corporate:

- Thursday 02-Apr:

- Corporate:

- Earnings:

- Pre-open: ANGO, AYI, CCG, LNN, NAMM

- Analyst/Investor Events: BKTI, AKBA

- Brokerage Conference:

- World Vaccine Congress

- Earnings:

- Economic

- US: Challenger Job Cuts, Initial Jobless Claims, Continuing Jobless Claims, Trade Balance

- Canada: Trade Balance Goods

- Europe: Retail Sales y/y, CPI y/y

- Corporate:

- Friday 03-Apr:

- Corporate:

- PDUFA: IONS (SPINRAZA)

- Economic

- US: Nonfarm Payrolls, Unemployment Rate, Average Weekly Hours, Average Hourly Earnings, PMI Services Final, ISM Non-Manufacturing Index

- Europe: Industrial Production m/m

- Corporate:

Thanks to Street Account, Vital Knowledge, and Bloomberg as valued sources.