This will be the only note today as my youngest daughter just arrived home from California and I want to spend as much time with her and Lee Ann. I wish all of you and your family a wonderful Thanksgiving holiday. I’ll be back on Friday but will probably be in and out of the Slack chatroom today as I will still be trading. If you haven’t joined yet here’s a link to join. THIS note is the longest First Call note ever as I jammed in a lot including a look at Bond ETFs and the major Sector ETFs.

- S&P futures down 0.15% and Nasdaq futures down 0.25%. Follows a mostly higher finish Tuesday that saw stocks end near best levels with help from big tech. Today, European markets are lower following a mixed Asian session. Treasuries firmer with a bit of curve steepening. Dollar index down 0.6%; yen strength a focus. Gold up 1.2%. Bitcoin up 1.2% after two days of decline. WTI crude up 0.3%.

- Tom DeMark cautious comments on Market Watch today.

- Tariffs still the major story with further economic-policy picks by Trump (including Kevin Hassett for the National Economic Council and Jamieson Greer as US Trade Representative) seen as helping the president-elect enact his broad trade plans. At the same time, continued discussion about how Trump may be using more hardline rhetoric as a negotiating tactic to help reshape global trade. Some focus on earnings as well with disappointing updates from a range of larger hardware/software firms. More on the positive side, morning sees the beginning of a 60-day ceasefire between Israel and Hezbollah following weeks of talks.

- A notable array of economic data coming this morning, including October PCE, durable goods, pending home sales, weekly jobless claims, and the second read of Q3 GDP. Week’s series of Treasury auctions concludes today with a $44B sale of 7Y notes (will follow strong auctions for $69B in 2s on Monday and $70B in 5s yesterday). Overseas, German and French consumer confidence data deteriorated. China industrial profits shrank at a slightly quicker pace in October. RBNZ cut OCR by 50 bp to 4.25%, as expected. Note US market closed tomorrow for Thanksgiving Day holiday while Friday will see an early close (at 13 ET).

- DELL hit by sales miss on softer consumer PC demand though also noted record AI server orders and margins surprised to the upside. CRWD Q3 key metrics better but Q4 EPS guide a touch below and unchanged FY25 outlook flagged as a disappointment. WDAY better Q3 seemingly overshadowed by slightly weaker Q4 sub revenue and margin guidance. ADSK guidance was in line and flagged new business growth headwinds. HPQ PC sales light, said growth stronger in back half of year. AMBA beat and raised, highlighting normalizing inventories and ramping automotive wins. Outside of tech, JWN beat with both Nordstrom and Nordstrom Rack ahead, while guide largely unchanged. URBN posted a big margin-driven beat with Anthro the bright spot. GES missed and cut guidance, flagging slow NA customer traffic.

- Key Upgrades/Downgrades: Baird initiates BKNG, EXPE outperform. Kohl’s downgraded to neutral from outperform at Baird. Urban Outfitters upgraded to buy from neutral at Citi. Workday downgraded to neutral from overweight at Piper Sandler. Dick’s Sporting Goods upgraded to buy from neutral at UBS.

market snapshot

economic reports today

premarket trading

US MARKET SENTIMENT

S&P and Nasdaq bullish sentiment remains extreme.

Investors Intelligence Newsletter Sentiment Survey – Still in danger zone

The bulls increased modestly to 61.3%, from 60.0% a week ago. That is the seventh week in the danger zone above 55%, and the most bulls since 64.2% late July. That reading ended seven weeks above 60%. Counts above 60% signal very elevated risk. History shows the peak bull count occurs early in the topping process, and then approaches that peak again near the final top. That could be the current situation.

The latest highs trimmed the bears to 17.7%, from 18.3% and 20.7% the prior two weeks. Again we note the fewest bears since early summer when that figure fell to just 14.9% as the averages reached highs. There was also a small decline for those editors projecting a correction, ending at 21.0% from 21.7% last issue. Those are still relatively depressed levels, down significantly from 33.9% at the start of September. A higher number with correction camp >35% is a decent buying opportunity.

Bond bullish sentiment remains oversold lacking upside momentum

Currency bullish sentiment highlighted with Bitcoin reversal again after recently hitting an extreme 88%. Dollar remains in the extreme zone at 80%

Commodity bullish sentiment was mixed

US MARKETS

S&P futures 60-minute tactical time frame drifted higher and had a new Combo 13 yesterday. A new Setup 9 could see a bounce however if this continues lower a new Sequential Countdown could start and extend downside trend.

S&P futures daily bounced off the 20 day last week. I’m watching the DeMark Reference Close as first support at 5970

Nasdaq 100 60-minute tactical time frame has less momentum vs S&P and yesterday a new Sequential sell Countdown 13 and reversal. Setup 9 might bounce this morning however if downside continues after the Setup 9 a Sequential can start.

Nasdaq 100 futures daily held the 20 day again yesterday. I’m watching 20,783 TD Reference as first support

bond etf update

A reversal up with TLT and IEF Treasury ETFs and a possible reversal down with high yield. I like Treasuries long here for a trade and HYG might be a decent short here.

Extra charts we’re watching

US Dollar Index daily reversal possible and DeMark Propulsion downside target of 104.89. It’s qualified but will need to confirm on Friday. I will follow up if it confirms.

US 10-Year Yield reversal. Note the pending secondary Sequential will cancel with completion of the buy Setup 9 on Friday.

Bitcoin Daily reversal after the last two Combo’s with downside Propulsion target.

Bitcoin bullish sentiment reversal after hitting extreme 88% level

major sector etfs

Comments on charts – If you have more questions, please send an email

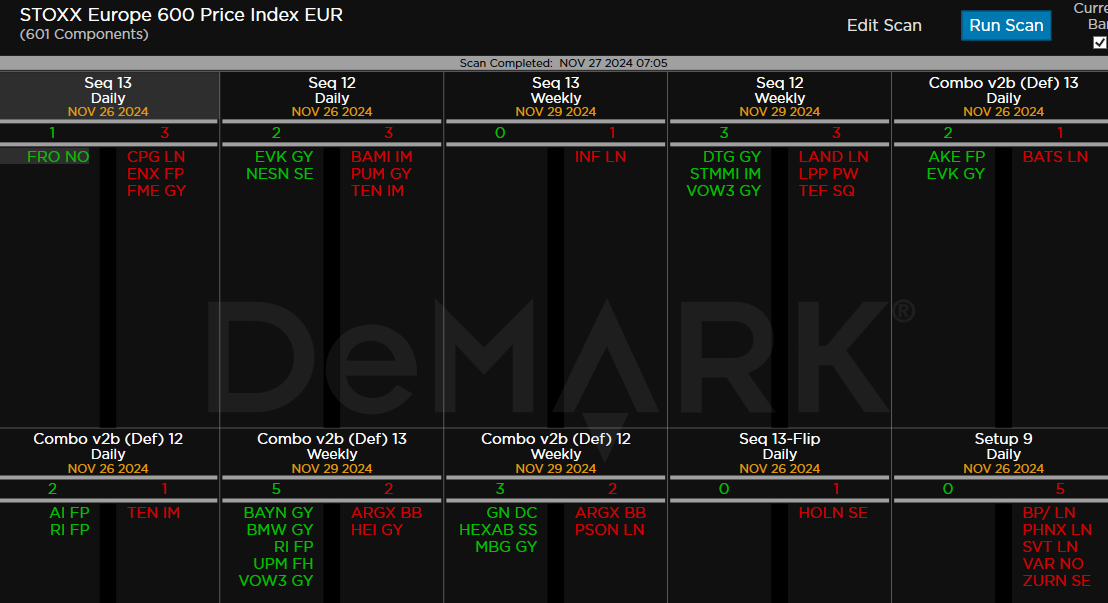

DeMark Observations – Euro Stoxx 600