TOP EVENTS AND CATALYSTS

The week ahead will be extremely busy, with many major macro and Q4 earnings catalysts with five out of the seven Mag 7 stocks. On the macro front, major events include China’s NBS PMIs for January tonight, the Bank of Canada rate decision Wednesday morning; a 25bps rate cut is expected; the FOMC rate decision Wednesday afternoon; no rate change is expected, the ECB decision Thursday morning; a 25bps rate cut is expected, the US GDP and PCE for Q4 Thursday; the consensus is looking for GDP +2.6%, the US PCE for December Friday; the consensus for core to hold steady vs. November at +2.8%, and the US Employment Cost Index for Q4 Friday. The RFK Jr. nomination hearing is set to take place Wednesday, with Gabbard on Thursday.

The majority of the US market cap is reporting Q4 earnings this week. Important earnings include: Monday premarket: T; Monday postmarket: NUE; Tuesday premarket: BA, GM, LMT, RCL, RTX, SYF; Tuesday postmarket: BXP, CB, QRVO, SBUX; Wednesday premarket: ADP, BABA, EAT, GLW, OTIS, TMUS; Wednesday postmarket: CHRW, IBM, LRCX, META, MSFT, NOW, TSLA, URI, WDC; Thursday premarket: BX, CAT, CI, CMCSA, DOW, LUV, MA, NOC, PHM, UPS; Thursday postmarket: AAPL, DECK, INTC, KLAC, V; and Friday premarket: ABBV, CHTR, CVX, ETN, LYB, XOM.

Important European earnings include Tuesday: SAP, LVMH; Wednesday: Akzo Nobel, ASML; and Thursday: ABB, BBVA, Deutsche Bank, Electrolux, Glencore, Nokia, Sanofi, Shell, STM, and Roche.

This week, I will have several earnings preview notes, including the most relevant companies’ reports. The Currency and Commodity weekly notes will be sent/posted shortly after this note. Enjoy the NFL playoffs today!

Weekend News

- Trump insiders warn markets not to get too comfortable: incremental tariffs are still coming (“Tariffs are coming in the next couple months — broad based, universal tariffs…the president is serious about the universal tariff”) Politico

- Chinese stocks spiked on Friday in the US thanks in part to media reports highlighting how the Trump 2.0 team has been more benign toward Beijing than feared (although it’s only been a week); according to the SCMP, Sec of State Rubio told his Chinese counterpart that the US does not back Taiwan’s independence, while Trump said he’d “rather not” impose additional tariffs on Chinese imports.

- Trump reiterated over the weekend the US would eventually take Greenland and recently held a phone call with Denmark’s PM during which Greenland was discussed, and that conversation apparently went “very badly,” suggesting geopolitical tensions around this topic could escalate going forward FT

- TikTok: Trump said there would be a decision on what to do with TikTok within the next 30 days (the White House is apparently working on a proposal whereby Oracle and a group of outside investors would assume control of the app’s US operations, with ByteDance retaining a stake Reuters

Strong growth with Mag 7, yet very crowded

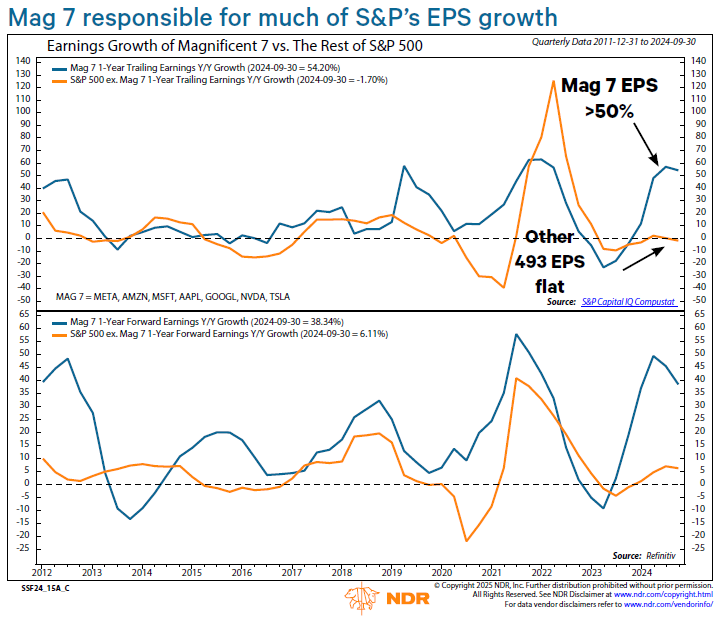

I thought I’d share some charts from my friends at Ned Davis Research, with 5/7 of the Mag 7 reporting this week. Mag 7’s earnings growth has been very strong, with most of the strength being in NVDA (reporting later in February). AAPL and Tesla have not been growing but have seen dramatic earnings multiple expansion in price. Price action the day after the last earnings reports for the five reports was mixed with META -4%, MSFT -6%, TSLA +22%, AAPL -1%, and AMZN +6%. Tesla earnings were ‘better’ but still down YoY, yet it was the hype with Musk promising 20-30% growth in deliveries in 2025, Robo-taxi, and robots coming in 2025.

Earnings growth for the S&P ex Mag 7 493 is expected to grow each quarter in 2025, and Mag 7 growth is expected to be at 20%. The hypergrowth for the Mag 7 from mid-2023 to the end of 2024 is expected to moderate. Both estimates seem high, typically seeing lower growth expectations moving down as the year progresses. The only clear earnings grower will be NVDA as they continue to supply the hyperscalers.

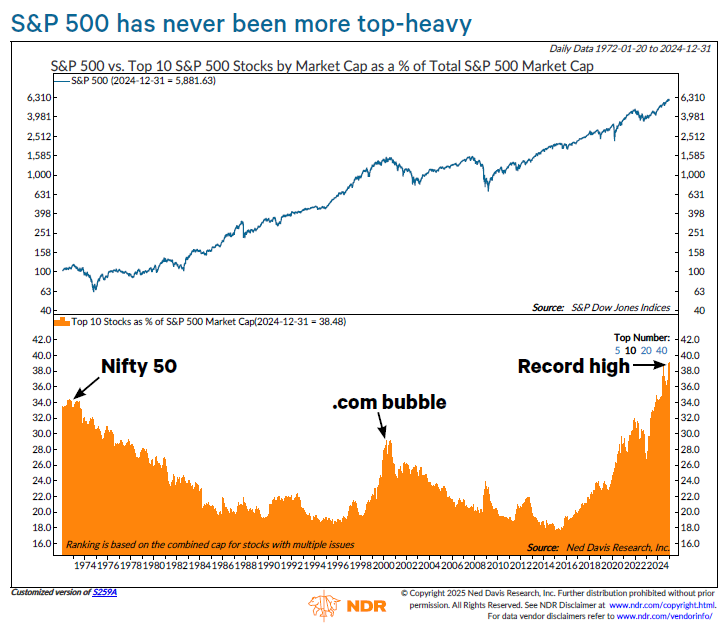

The top ten S&P stocks comprise 38.5% of the S&P, putting much pressure on these companies to continue gains.

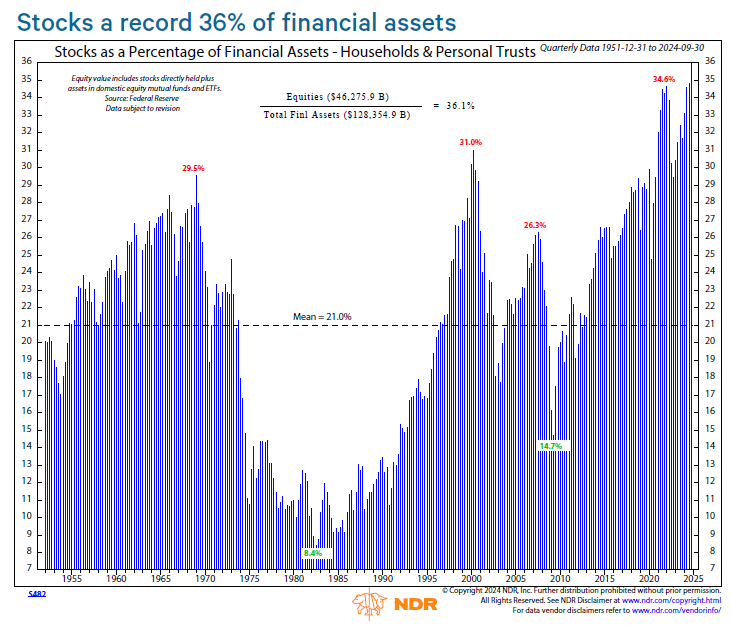

It’s hard for those to say there’s cash on the sidelines when the percentage of household financial assets is this high at 36%.

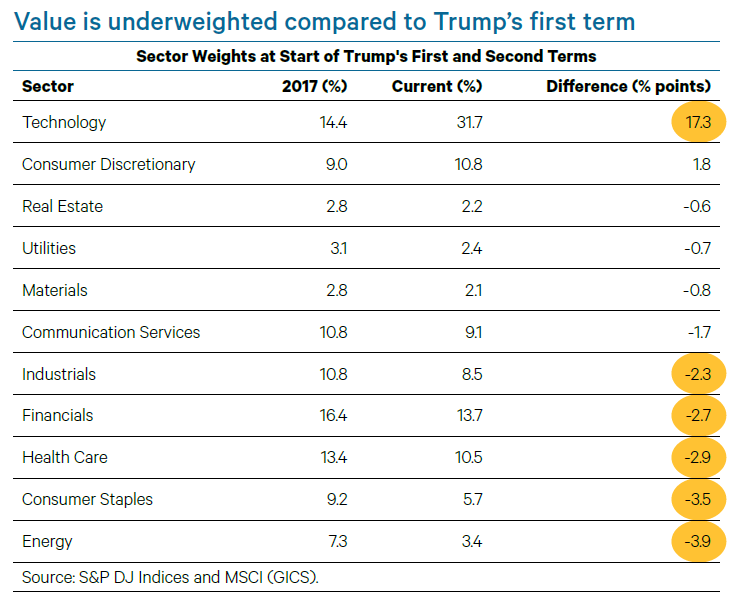

And we know where people have invested, primarily in tech and consumer discretionary. This shows the weightings of the S&P sectors today vs the start of Trump 1.0. The weighting gain in technology, 32%, from 14%, is extraordinary, illustrating the crowding in tech. Again, the market will rely on tech to outperform in 2025.

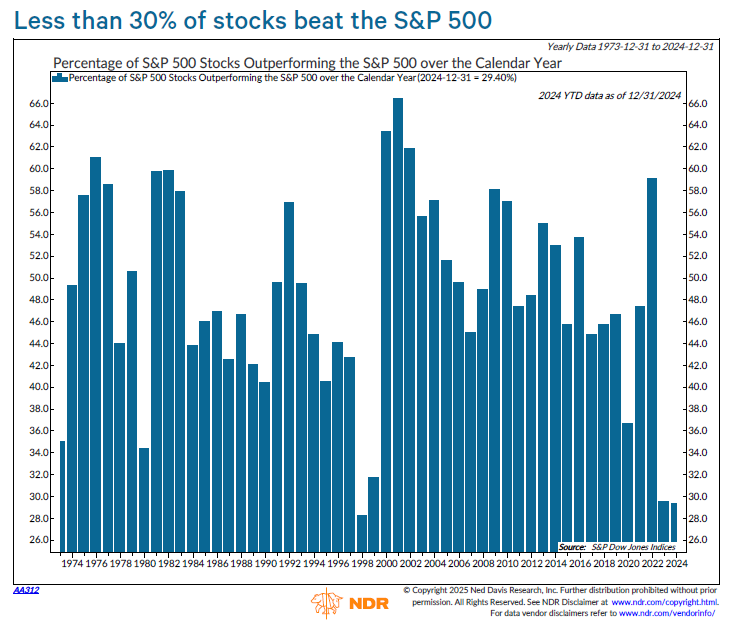

I’ve shown this chart in the past, and it gives me much hope for broadening out in 2025. The tech bubble from 1998 to 1998 burst in 2000, and markets broadened. However, it should be noted that indexes were lower due to the narrow attribution with technology, leading to the downside. A similar but not as dramatic situation occurred after 2020-2021, with a sharp spike in 2022 in companies beating the S&P. This is how I see it possible to see us beat the market in 2025 as we did in 2022.

US economic data for the week

KEY MARKET SENTIMENT

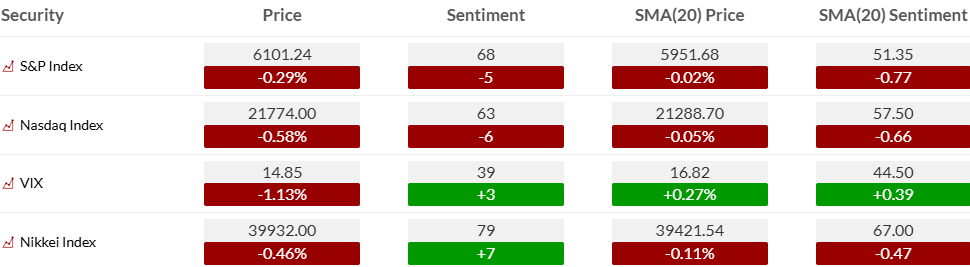

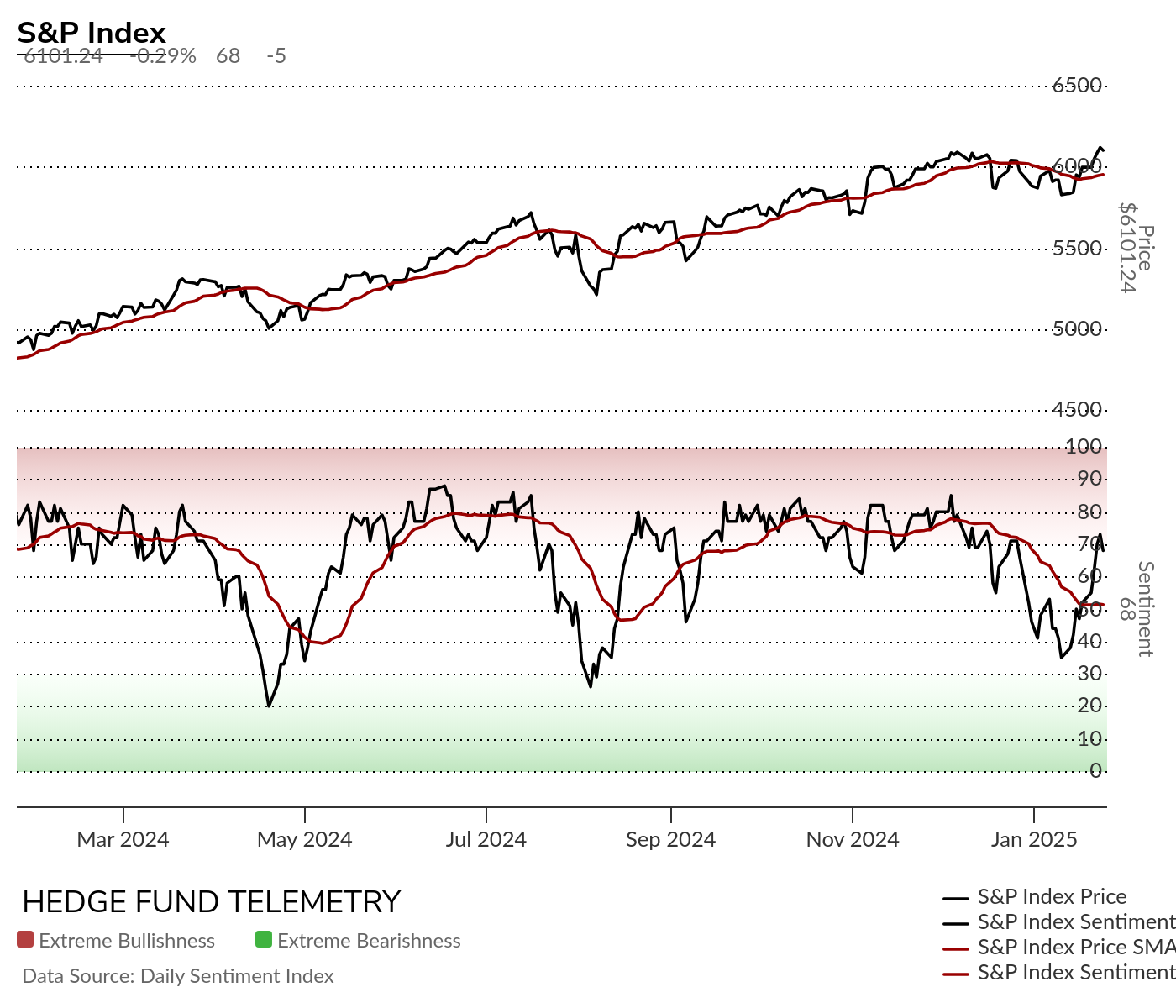

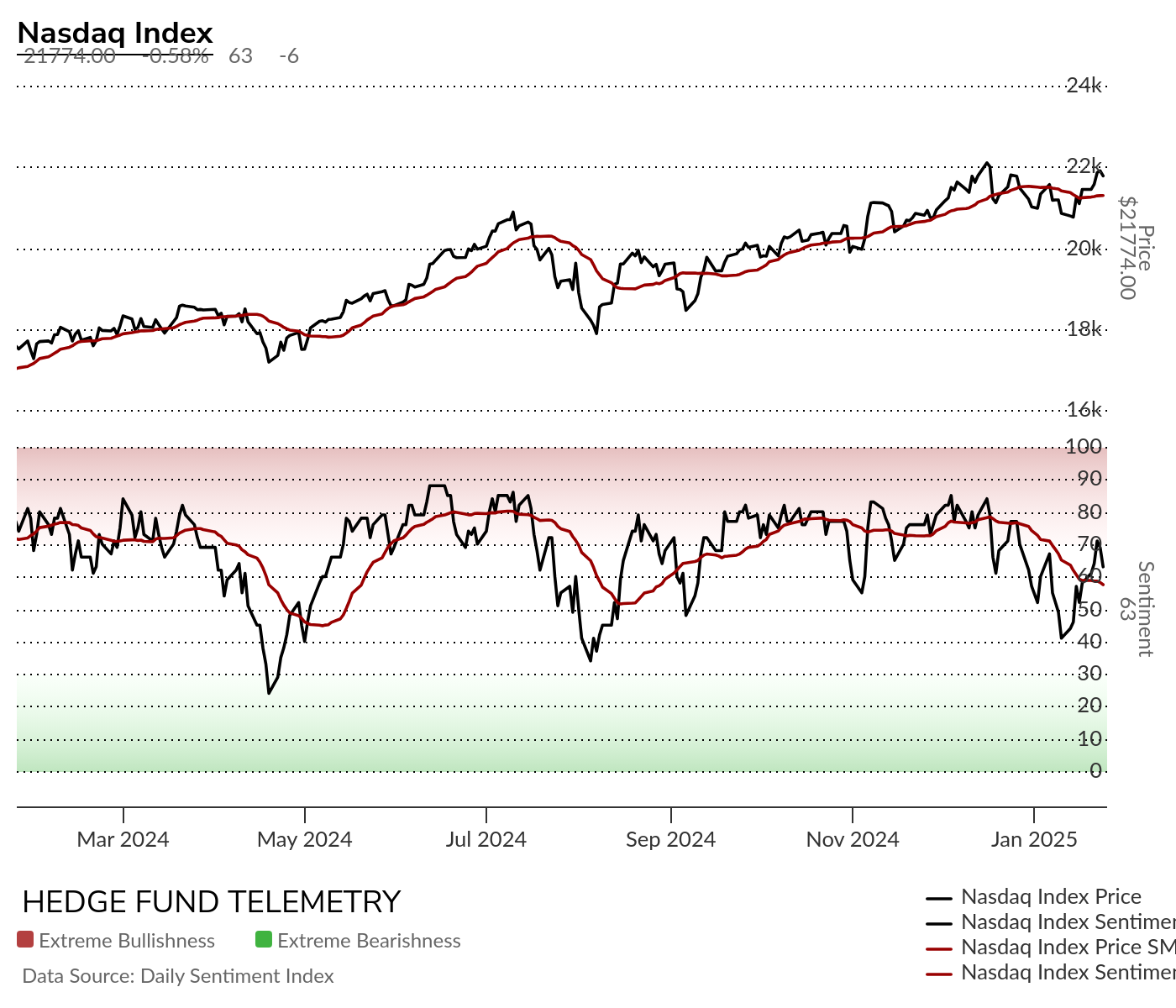

Equity bullish sentiment backed off from recent gains in the last week on Friday

S&P and Nasdaq bullish sentiment hasn’t been able to get to fully oversold conditions, and the latest move lower didn’t get even close to being oversold. It’s possible the move was another lower high bounce divergent from price action.

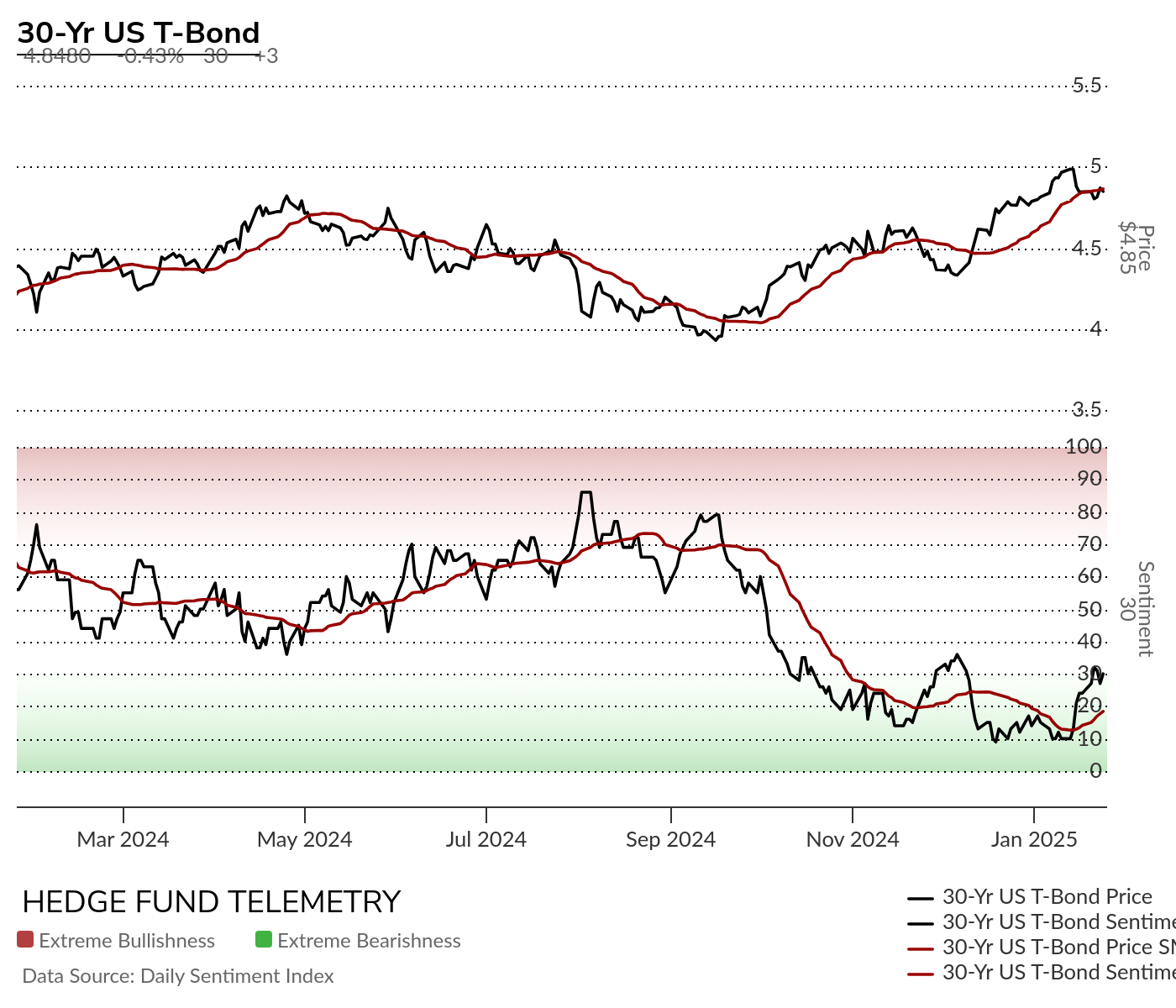

Bond bullish sentiment was recently very oversold at 10% and has bounced but still has more work on the upside to clearly shift the trend.

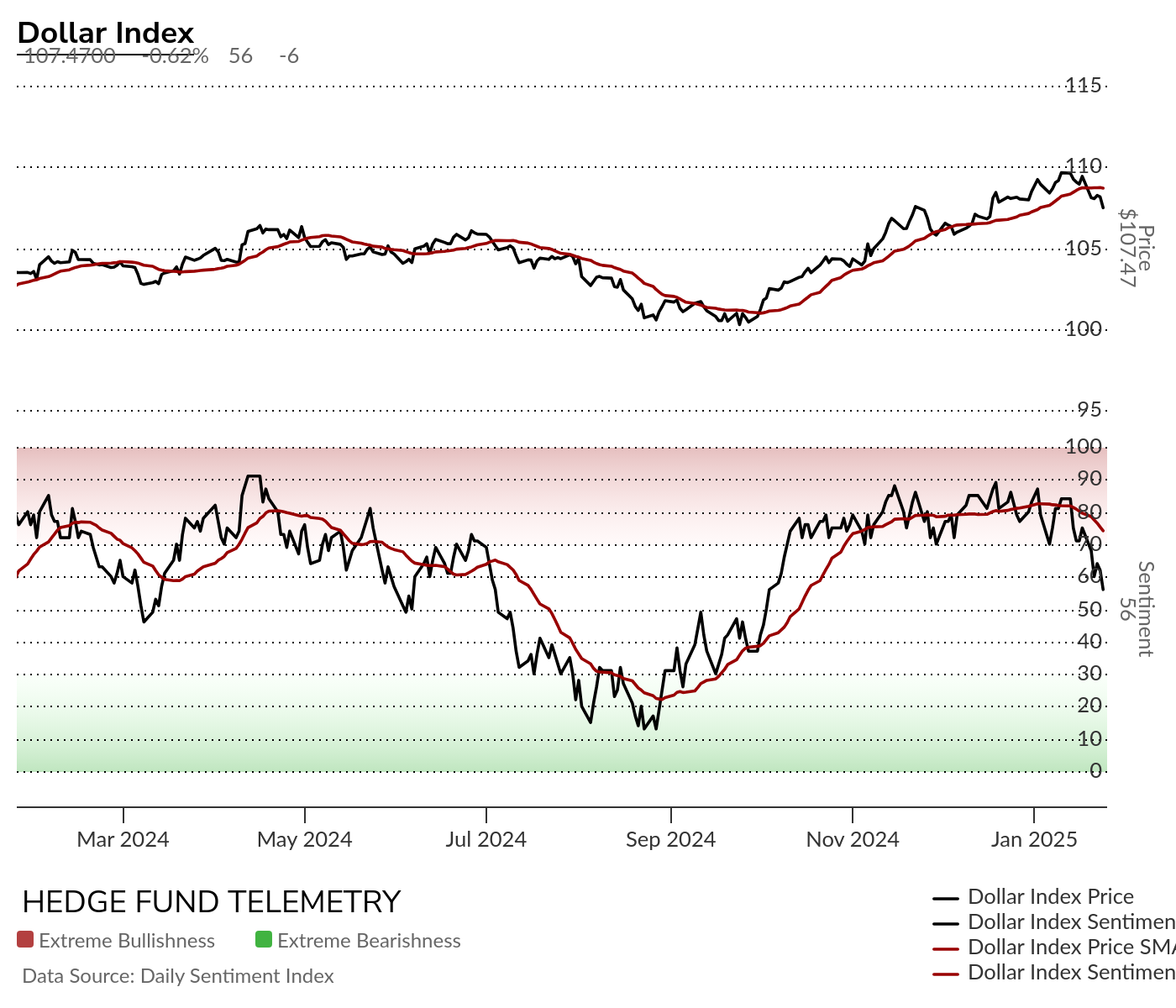

Currency bullish sentiment with US Dollar bullish sentiment moving lower again – nearly at the 50% midpoint majority level. Keep an eye on this, as I will discuss it throughout the week.

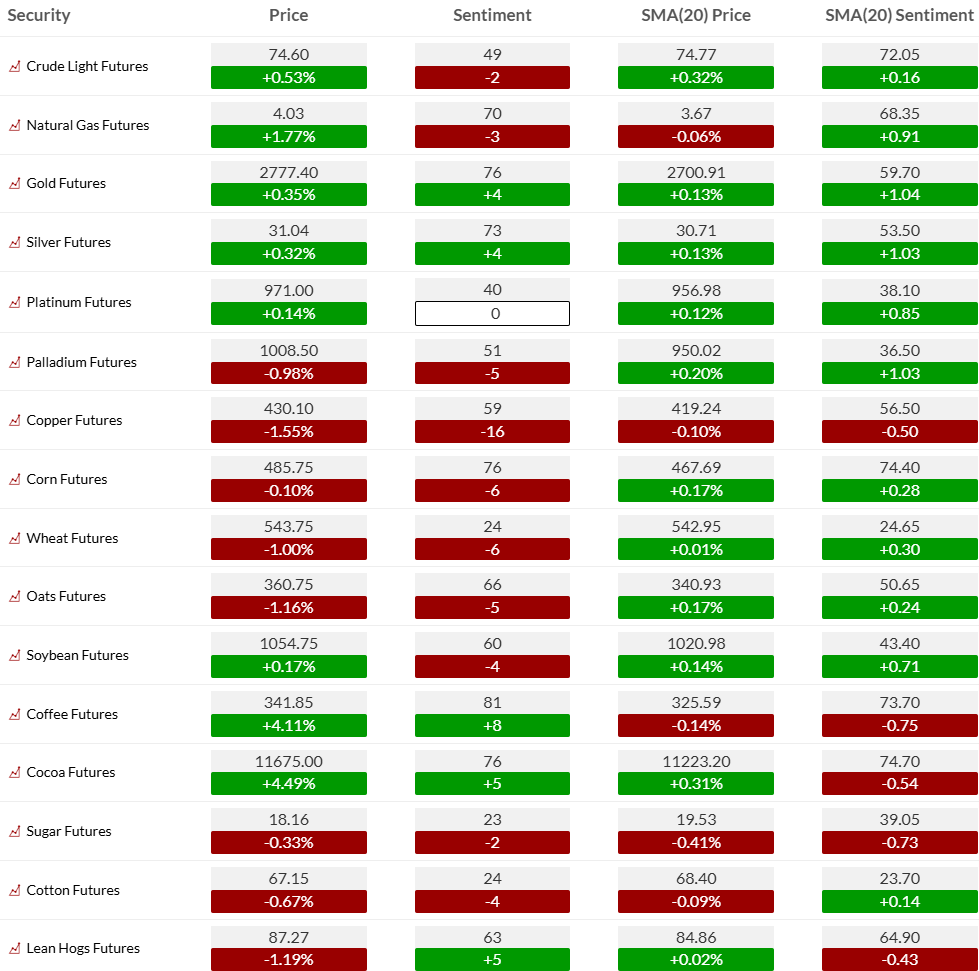

Commodity bullish sentiment has been highlighted with Crude bullish sentiment moving below the 50% midpoint level falling all last week. Gold and Silver remain in the elevated zone >70%.

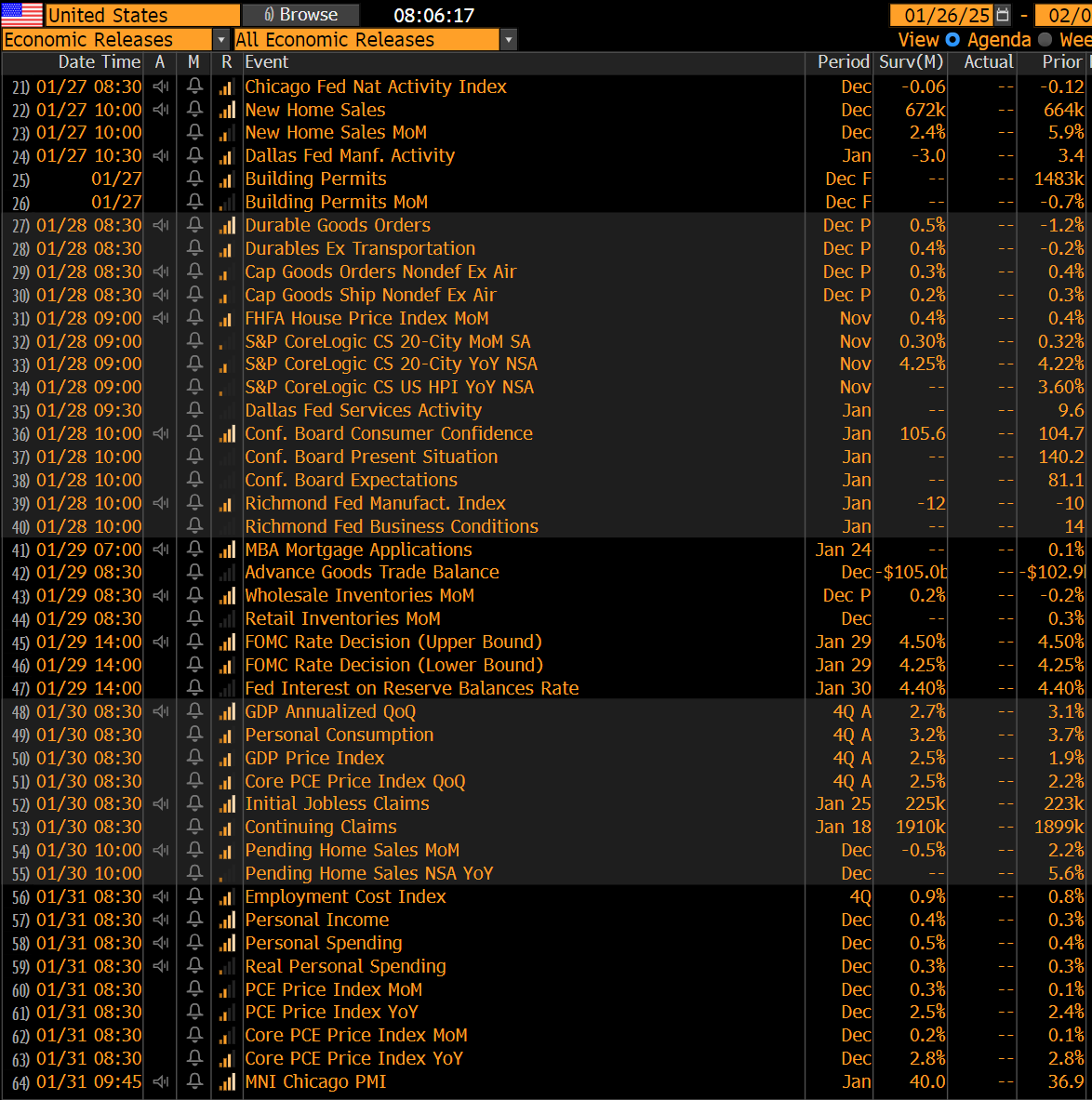

EARNINGS, CONFERENCES, AND ECONOMIC REPORTS

- Monday 27-Jan:

- Corporate:

- Earnings:

- Pre-open: BMRC, BOH, DX, HOPE, OXLC, SOFI, T

- Post-close: AGNC, ARE, BRO, CR, EFSC, ELS, FSBC, GGG, HBCP, HMST, NBTB, NUE, PCH, PFBC, SANM, SBCF, SFBS, TRNS, WAL, WRB, WSFS:

- Brokerage Conference:

- ABA Insurance Risk Management Forum

- Cleantech Forum North America

- Projects & Money in Infrastructure Market

- Earnings:

- Economic

- US: New Home Sales

- Europe: Trade Balance, Retail Sales y/y, IFO Business Climate

- Corporate:

- Tuesday 28-Jan:

- Corporate:

- Earnings:

- Pre-open: ADNT, BA, BPOP, CAC, CVLT, GM, IVZ, JBLU, KMB, LMT, PCAR, PII, PROV, QRVO, RCL, RTX, SYF, SYY, WRLD, XRX

- Post-close: ASH, AX, BXP, CB, FCF, FFIC, FFIV, FRST, GAU, HAFC, HLI, LC, LFUS, LRN, MANH, MTAL, NXT, PFS, PKG, RNR, RNST, SBUX, SYK, TRMK, UMBF, VBTX

- Analyst/Investor Events: EOSE, NPCE, SABS, YUM

- Syndicate: +SFD IPO (~$870M raise)

- Brokerage Conference:

- ABA Insurance Risk Management Forum

- Cleantech Forum North America

- Projects & Money in Infrastructure Market

- UBS Latin America Investment Conference

- DesignCon

- Microcap Conference

- International Production and Processing Expo

- Earnings:

- Economic

- US: Durable Orders, FHFA House Price Index, Consumer Confidence, API Crude Inventories

- Europe: Core Retail Sales m/m, Consumer Confidence

- Corporate:

- Wednesday 29-Jan:

- Corporate:

- Earnings:

- Pre-open: ADP, AIT, AVT, BLFY, CODA, CPF, DHR, EXP, EXTR, FLEX, GD, GLW, GPI, HESM, LII, MHO, MNRO, MSCI, NAVI, NDAQ, NSC, OTIS, PB, SBSI, SF, SLGN, TEVA, TMUS, VFC, WNC

- Post-close: AMP, AXS, BHE, BRKL, BSET, BWB, CALX, CCS, CHRW, CLB, CLS, CMPR, DLB, ETD, FIBK, HWKN, IBM, LBRT, LEVI, LRCX, LSTR, META, MSFT, MTH, MXL, NFG, NLY, NOW, RJF, SEIC, SIGI, TER, TSLA, TTEK, TWO, URI, WASH, WDC, WHR, WM, WOLF

- Analyst/Investor Events: KLYG, PHIO

- Brokerage Conference:

- ABA Insurance Risk Management Forum

- Cleantech Forum North America

- Projects & Money in Infrastructure Market

- UBS Latin America Investment Conference

- DesignCon

- Microcap Conference

- International Production and Processing Expo

- PDUFA: Elamipretide

- Earnings:

- Economic

- US: MBA Mortgage Purchase Applications, Wholesale Inventories, FOMC Meeting, DOE Crude Inventories

- Europe: Preliminary GDP y/y, GfK Consumer Confidence, Business Confidence, Consumer Confidence, M3 Money Supply y/y

- Corporate:

- Thursday 30-Jan:

- Corporate:

- Earnings:

- Pre-open: ABG, ALGM, AOS, AVY, BC, BFH, BHLB, BIP, BX, CAH, CAT, CFR, CHKP, CI, CIVB, CMCSA, CNOB, CNX, CRS, CSWI, DGX, DOV, DOW, DT, FFWM, FLG, FLWS, FRME, IP, KEX, LAZ, LHX, LUV, MA, MAN, MBLY, MBUU, MMC, MO, MPX, MUR, NOC, NTCT, ONEW, OSK, PH, PHM, RES, ROP, RPT, SCSC, SHW, SILC, SIRI, SKYW, SNDR, STBA, TMO, TSCO, TT, UPS, VLO

- Post-close: AAPL, ABCB, AJG, APPF, ATGE, BKR, BZH, COUR, DECK, EMN, FHI, FINW, FISI, GEN, GSIT, HIG, HTH, INTC, KLAC, LPLA, OLN, ORC, PPG, RMD, STEL, TBBK, TEAM, V, VIAV, WY

- Analyst/Investor Events: POST, SR

- Syndicate: +BBNX IPO (~$113M)

- Brokerage Conference:

- DesignCon

- Microcap Conference

- International Production and Processing Expo

- Santander Iberian Conference

- PDUFA: Treograft, VRTX (suzetrigine)

- Earnings:

- Economic

- US: GDP, Pending Home Sales, Weekly Jobless Claims, EIA Natural Gas Inventories

- Europe: PPI y/y, Consumer Goods Spending m/m, Preliminary GDP q/q, Retail Sales y/y, Unemployment Rate, Preliminary GDP y/y, Nationwide House Price Index y/y, Preliminary CPI y/y, KOF Leading Indicator, BoE Mortgage Approvals, M4 MoneySupply m/m, Unemployment rate, Economic Sentiment Indicator, CPI y/y, Preliminary (first) GDP y/y, PPI m/m

- Asia: Unemployment Rate, CPI Tokyo y/y, Industrial Production m/m (preliminary), Retail Sales y/y, Retail Sales m/m

- Corporate:

- Friday 31-Jan:

- Corporate:

- Earnings:

- Pre-open: ABBV, ALV, AON, ARCB, BAH, BBU, BEN, BEP, BMI, BR, CHD, CHTR, CL, CVX, ETN, FHB, GNTX, GWW, JHG, LYB, OMF, PSX, RBC, VRTS, VSTS, WT, XOM

- Syndicate: +INR IPO (~$260M)

- PDUFA: AXSM (AXS-07)

- Earnings:

- Economic

- US: Core PCE, Personal Spending, Personal Income, Employment Cost Index, Chicago PMI

- Canada: GDP m/m

- Europe: Retail Sales, Retail Sales y/y, Retail sales y/y, PPI m/m, Preliminary CPI y/y, PPI y/y

- Asia: Housing Starts y/y, Trade Balance

- Corporate:

Thanks to Street Account, Vital Knowledge, and Bloomberg as valued sources.