Before we begin, an apology to some subscribers who we discovered have not recieved emails. If you ever are missing an email please let us know as some email servers on occasion will send a bounce back which pauses emails. With our new programming team working on improvements starting with the back end processes and soon with some upgrades for the main pages and notes. We are really excited for the rollout of a new knowledge base section, a section for videos and webinars and more. Thanks for your support and patience as we will have more for you in the coming months.

A lot of extra charts including Uranium long exposure, market internals and point and figure bullish percent index updates.

TOP EVENTS AND CATALYSTS

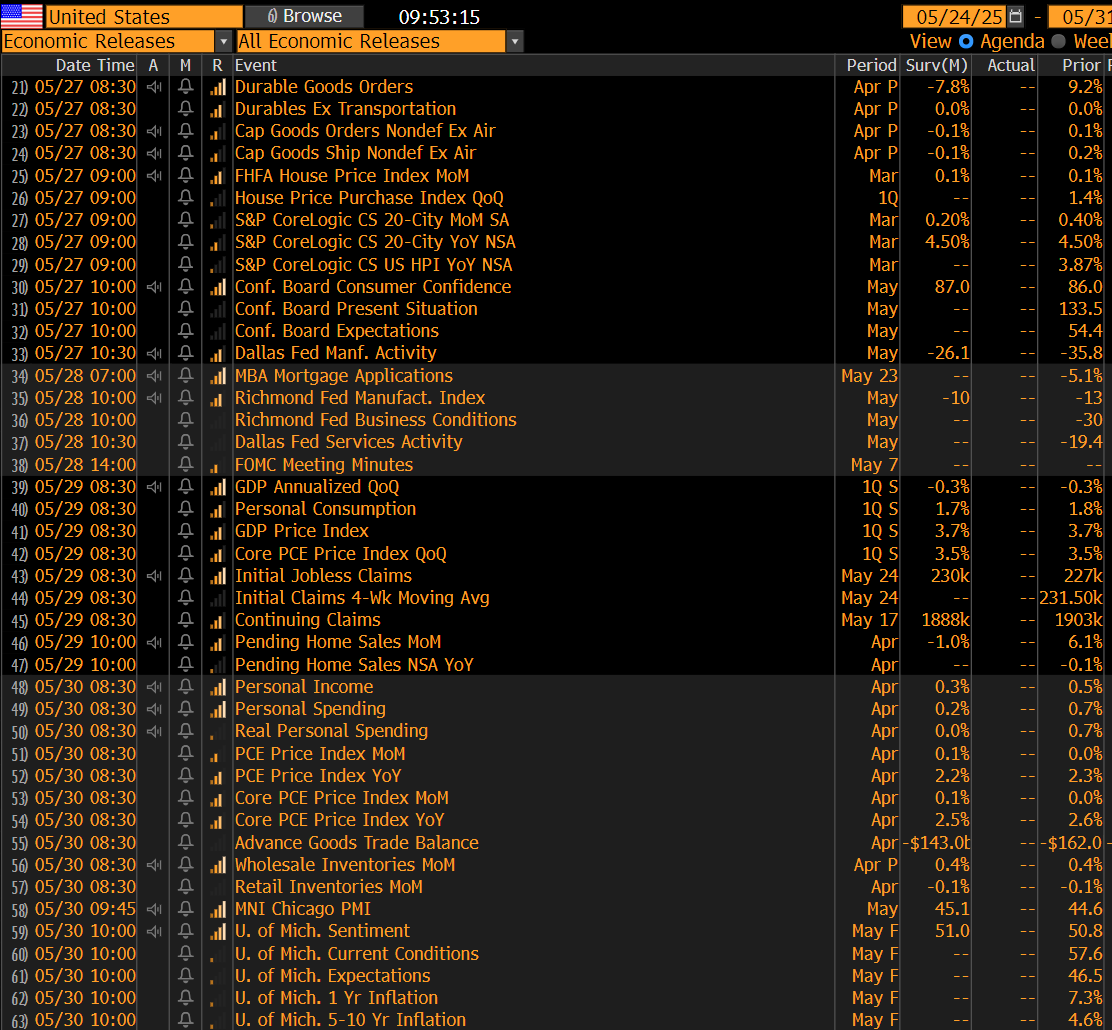

The main economic numbers this week include the US GDP/PCE revisions for Q1 on Thursday, Japan’s Tokyo CPI for May on Thursday night, the US PCE for April on Friday; concensus expects headline and core to tick down 10bps vs. March to +2.2% and +2.5%, respectively, the final Michigan sentiment report for May on Friday; the final inflation numbers should ease vs. the preliminary reading as the flash survey barely captured the US-China Geneva détente), and China’s NBS PMIs for May on Friday night.

On the monetary policy front, there are rate decisions from New Zealand on Tuesday night; a 25bps rate cut is expected and South Korea on Wednesday night; a 25bps rate cut is expected while ECB inflation expectations are published on Wednesday morning and the FOMC minutes on Wednesday afternoon; Fed officials have consistently warned that risks of a higher unemployment rate and higher inflation are both climbing, and investors will be scouring the minutes to see if Powell and his colleagues are slightly more concerned about one side of the mandate over the other. The US-EU trade negotiations will be in focus after Trump’s latest threat to impose a 50% tariff starting June 1.

The major US earnings reports include: Tuesday premarket: AZO, PDD; Tuesday postmarket: OKTA; Wednesday premarket: ANF, CPRI, DKS, M; Wednesday postmarket: A, CRM, HPQ, NVDA, SNPS, VEEV; Thursday postmarket: BBWI, BBY, BURL, HRL, KSS; and Thursday postmarket: COST, DELL, GAP, MRVL, NTAP, ULTA, ZS.

NVDA earnings on Wednesday postmarket will be the earning highlight and I will have a preview. I am planning on holding the current long position.

Weekend News

- Japan hopes to reach a trade deal with the US in time for the G7 Leader’s Summit (which takes place June 15-17) Bloomberg; Japan floats the idea of a joint sovereign wealth fund with the US as Tokyo pushes for an updated trade/economic agreement FT

- Trump’s EU tariff threat from Friday morning was driven by White House frustration with the pace of trade negotiations with Brussels WSJ

- Europe approached trade talks with Washington as if it were talking to an ally but has been met instead with a hostile and bellicose attitude from the White House regarding the relationship (Washington is demanding unilateral concessions from Brussels instead of searching for mutually beneficial scenarios) NYT; Europe will not change its VAT or lower food safety standards, two key demands of the White House NYT

- South Korea’s presidential frontrunner suggests the country will need more time to reach a trade agreement with the US (the South Korean election takes place June 3) CNBC

- The reconciliation bill probably won’t be that stimulative to the economy given the fact that most of the tax relief is simply extending existing rates (vs. cutting them further) while spending cuts will hurt lower-income workers and higher yields (driven by elevated deficits) will raise borrowing costs for everyone Politico

- Bessent on Friday confirmed what media reports have suggested recently – regulators are likely to soon ease the supplementary leverage ratio, a move that could give a boost to Treasuries Bloomberg

- NVDA Nvidia will launch a stripped-down Blackwell-based chip for the Chinese market priced at only $6.5-8K Reuters

- TSLA Tesla – Musk has grown increasingly disenchanted with politics and fears for his own safety and that of his family, which is why he’s pivoting back to business (Musk over the weekend said he’s returning “24/7” to his companies) Washington Post, Reuters

- X US Steel shares surged Friday afternoon after Trump announced on Truth Social that he would allow the company to form a partnership with Nippon Steel, effectively approving the acquisition (although the companies are still waiting for clarification from the White House about how specifically the deal will be structured) WSJ

Charts we are watching

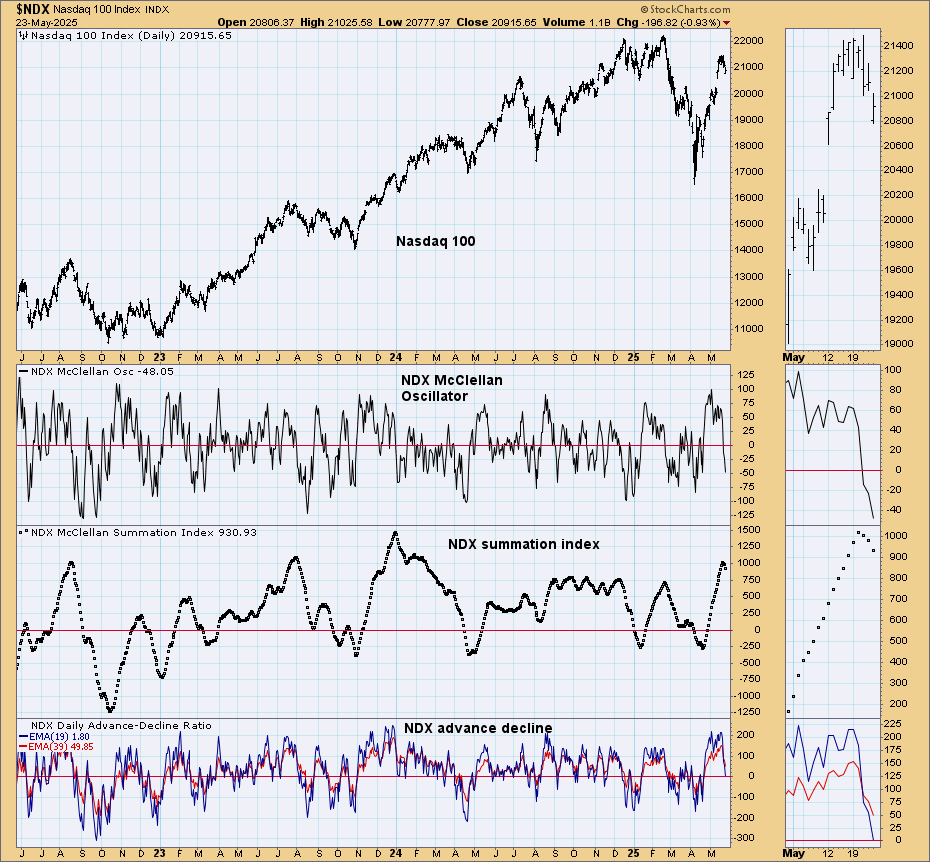

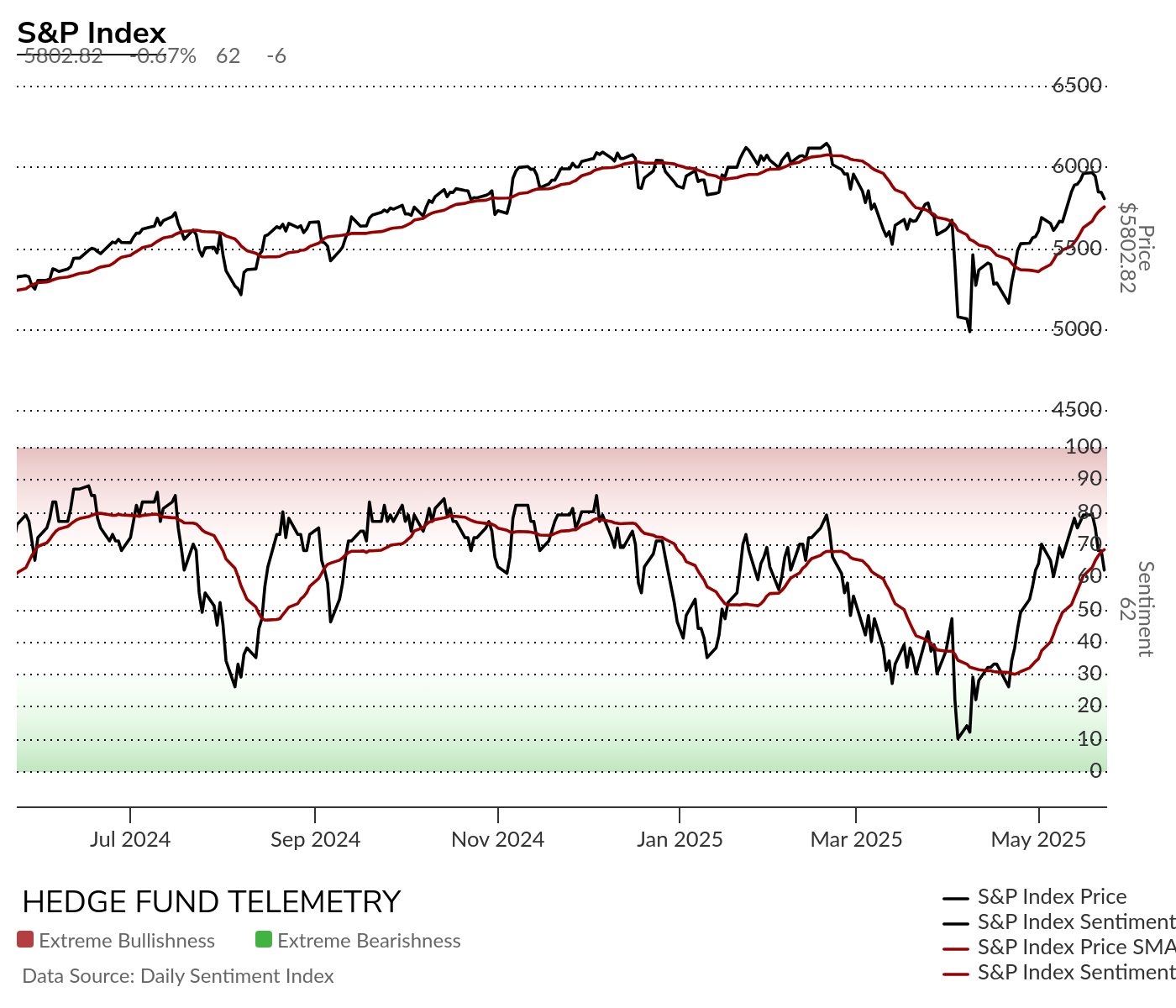

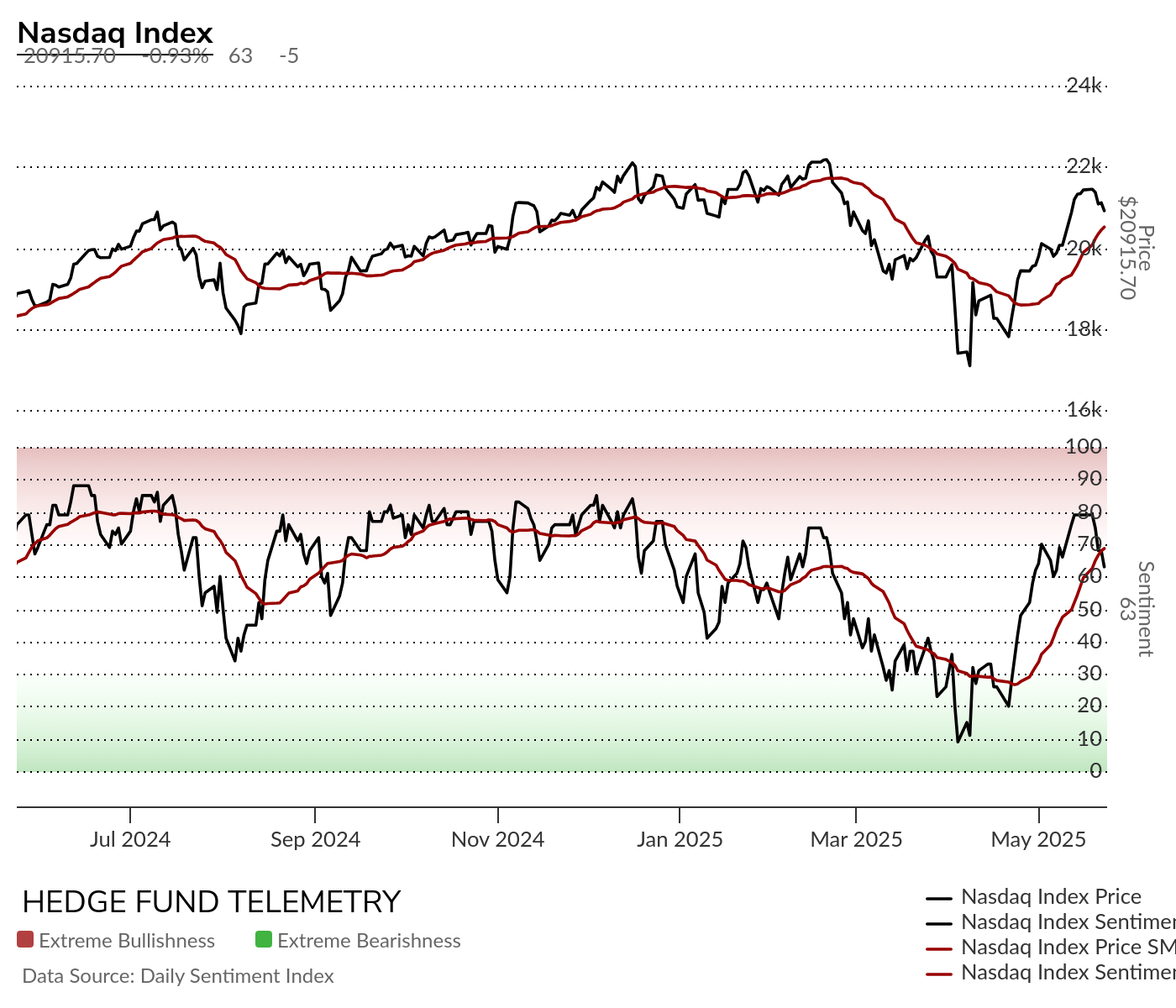

The S&P and Nasdaq 100 charts look identical with recent DeMark Combo sell Countdown 13’s and pending Sequential Countdowns. Downside Setup 3 of 9. If the Setup 9 completes with nine consecutive closes lower than the close four price bars earlier, then the pending Sequential will cancel. I am more focused on the 50 day as the more important support level to watch. (red line)

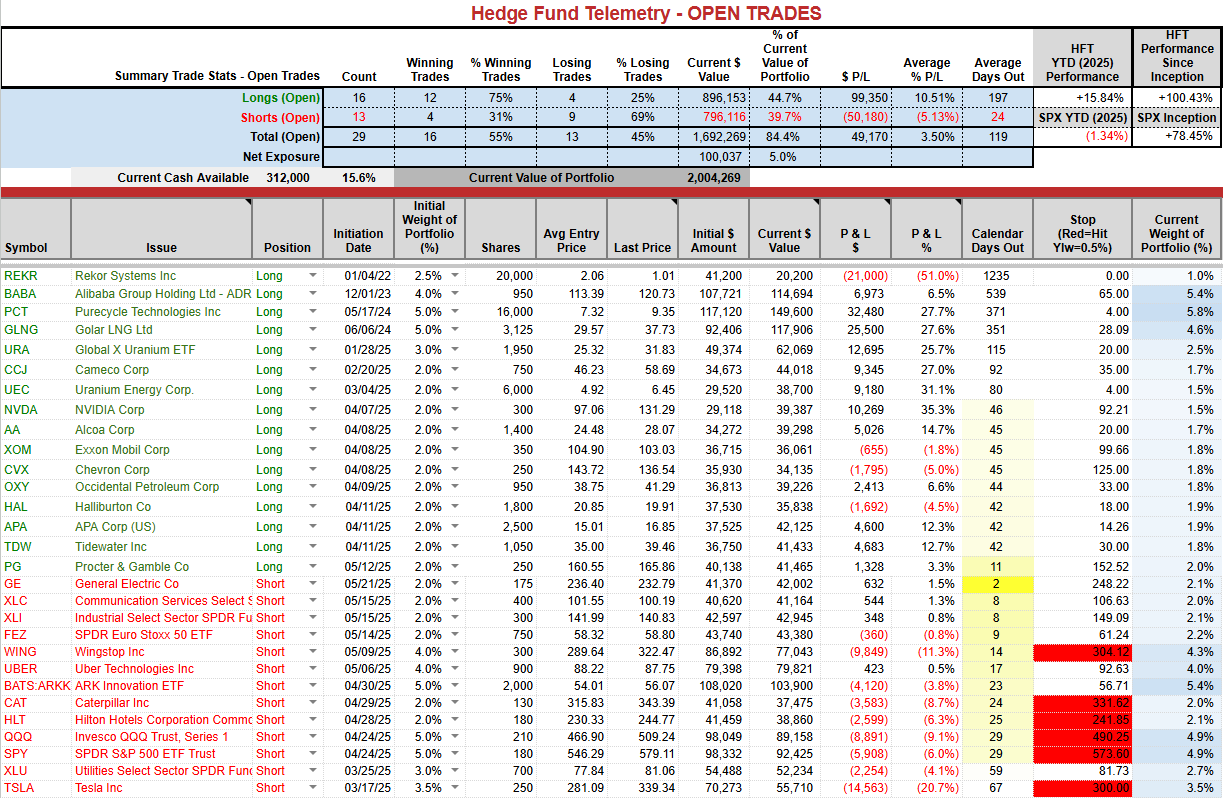

Trade Ideas sheet – uranum Friday surge

The Trade Ideas Sheet PNL closed at a new YTD high at +15.84% thanks to the 7% long weight with three Uranium names. A few problem names that I plan on cleaning up or adding. Since we started tracking the Trade Ideas sheet starting with $1m in 2021 it now is up 100% at $2m. Having the volatility in 2025 has clearly been a positive for our process.

URA, CCJ, and UEC with just mega moves. I do expect some consolidation with some DeMark exhaustion signals developing. I plan on holding a core long position through 2025 and maybe longer.

Internals and bullish percent index update

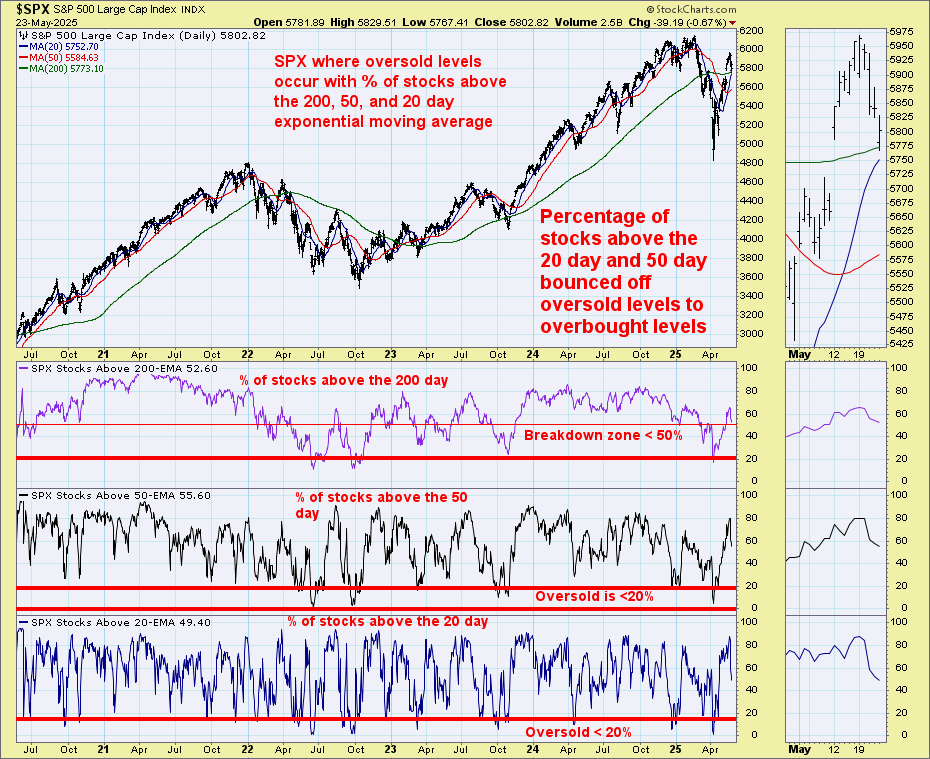

Some internal weakness has started last week as I showed mid week. The S&P percentage of stocks above the 20 and 50 day went from very oversold (when we pivoted net long) and now overbought and reversals down. Nothing significant yet.

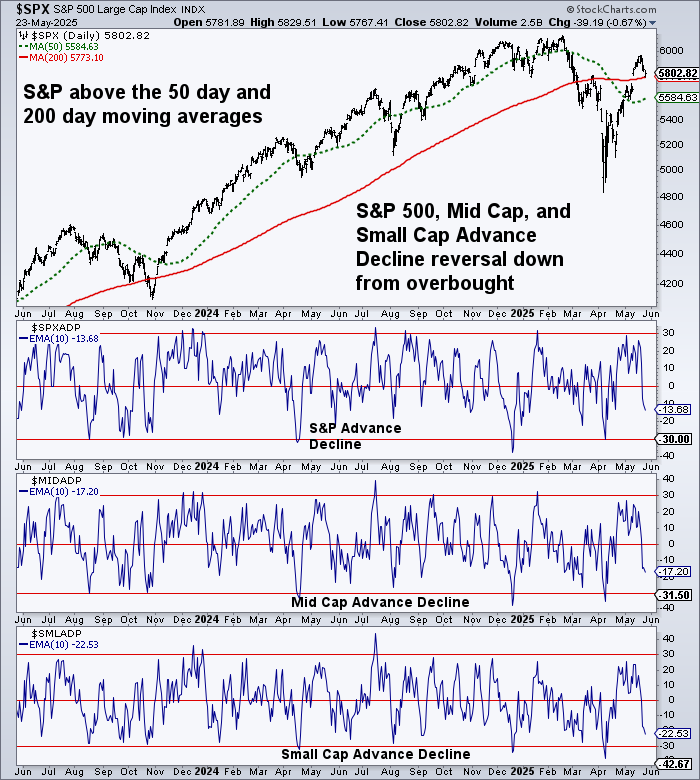

Advance Decline data has dropped very hard from overbought levels.

The 5 day moving average of the equity put call ratio was moderately elevated in early April (with more put buyers vs call buyers). It dropped hard with heavy call buying to levels where it is better to sell equities and bounced in the last week with more put buyers.

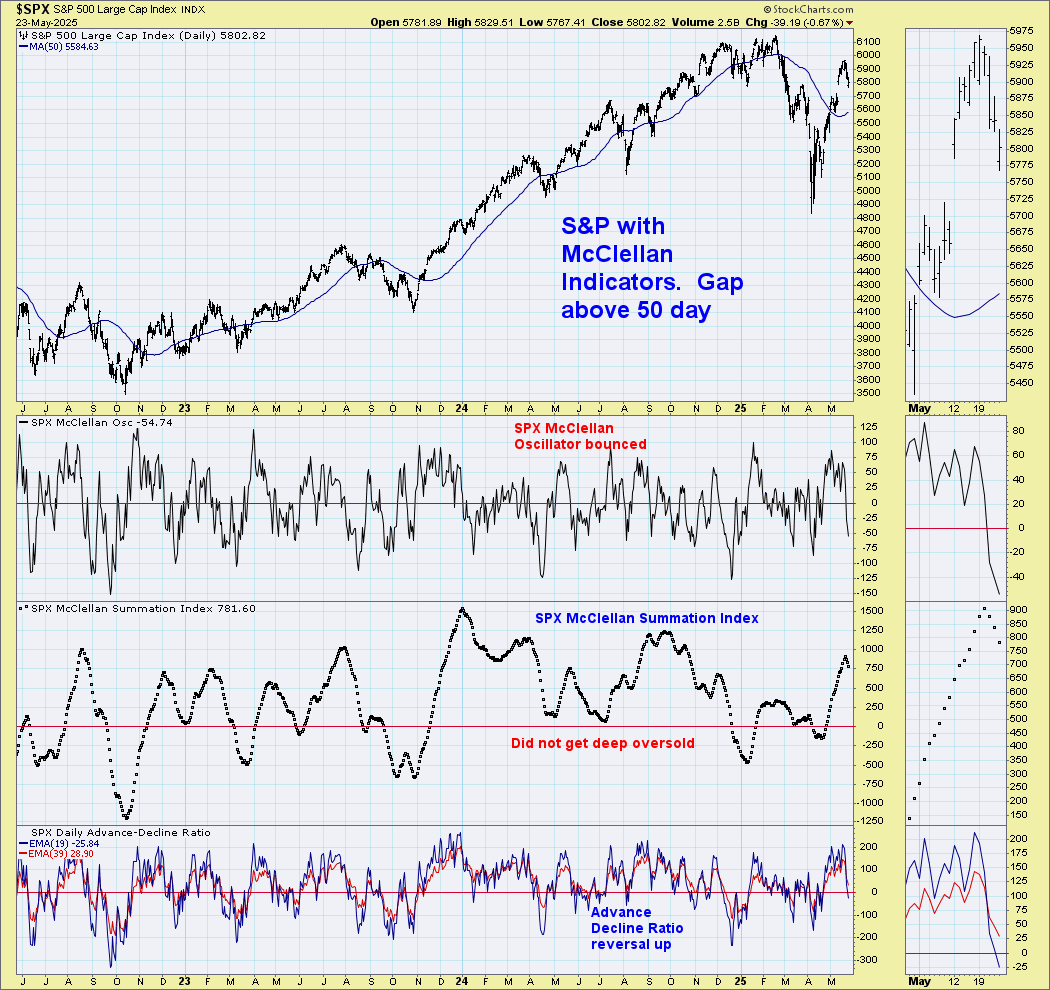

The S&P and Nasdaq 100 with McClellan indicators have now all started to reverse down.

The short term SPY and QQQ momentum indicators remain on sell signals. As a reminder I added these short early as I needed short exposure when I had excessive net long exposure. I figured (hoped) the long exposure would outperform the index short exposure, which worked out well.

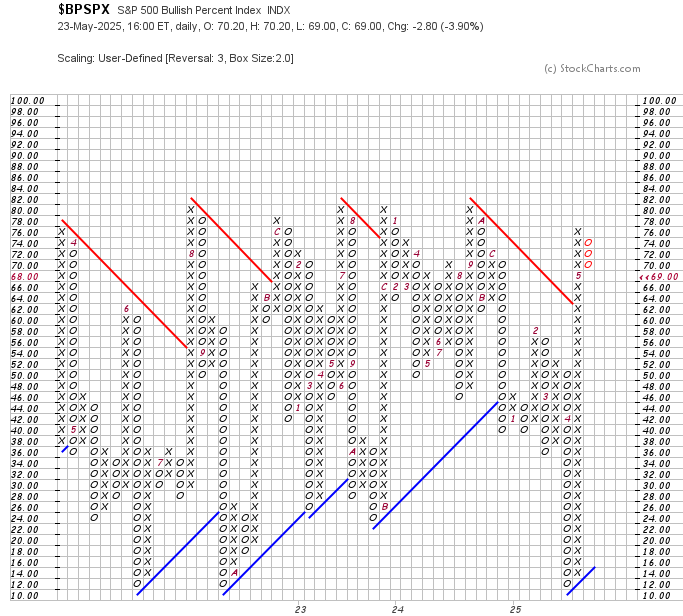

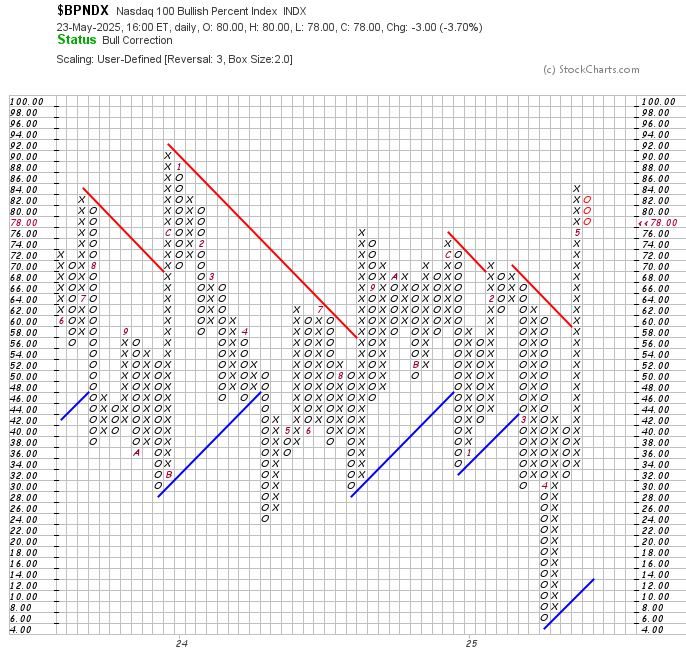

The Point and Figure bullish percent indexes in April were at DEEP oversold levels which was another indicator that helped us have the conviction to shift from net short to net long. The reversals up for both S&P and Nasdaq 100 bullish percent indexes have been unreal moving to now overbought levels. Reversals back into a column of 0’s are downside reversals. For more about Point and Figure bullish percent indexes click here.

US economic data for the week

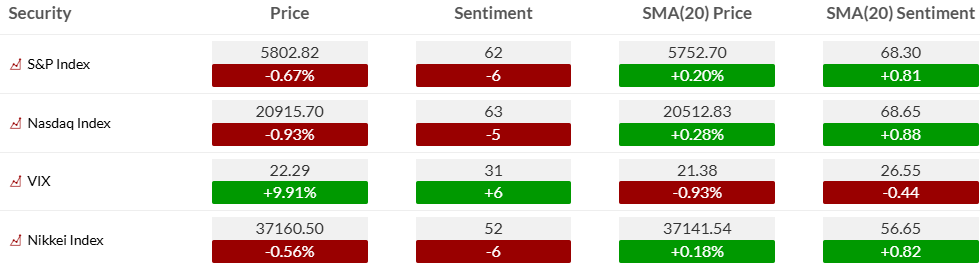

KEY MARKET SENTIMENT

Equity bullish sentiment declined to low 60% level on Friday after hitting 79% earlier in the week.

S&P and Nasdaq bullish sentiment reversals under the 20 day moving average of bullish sentiment.

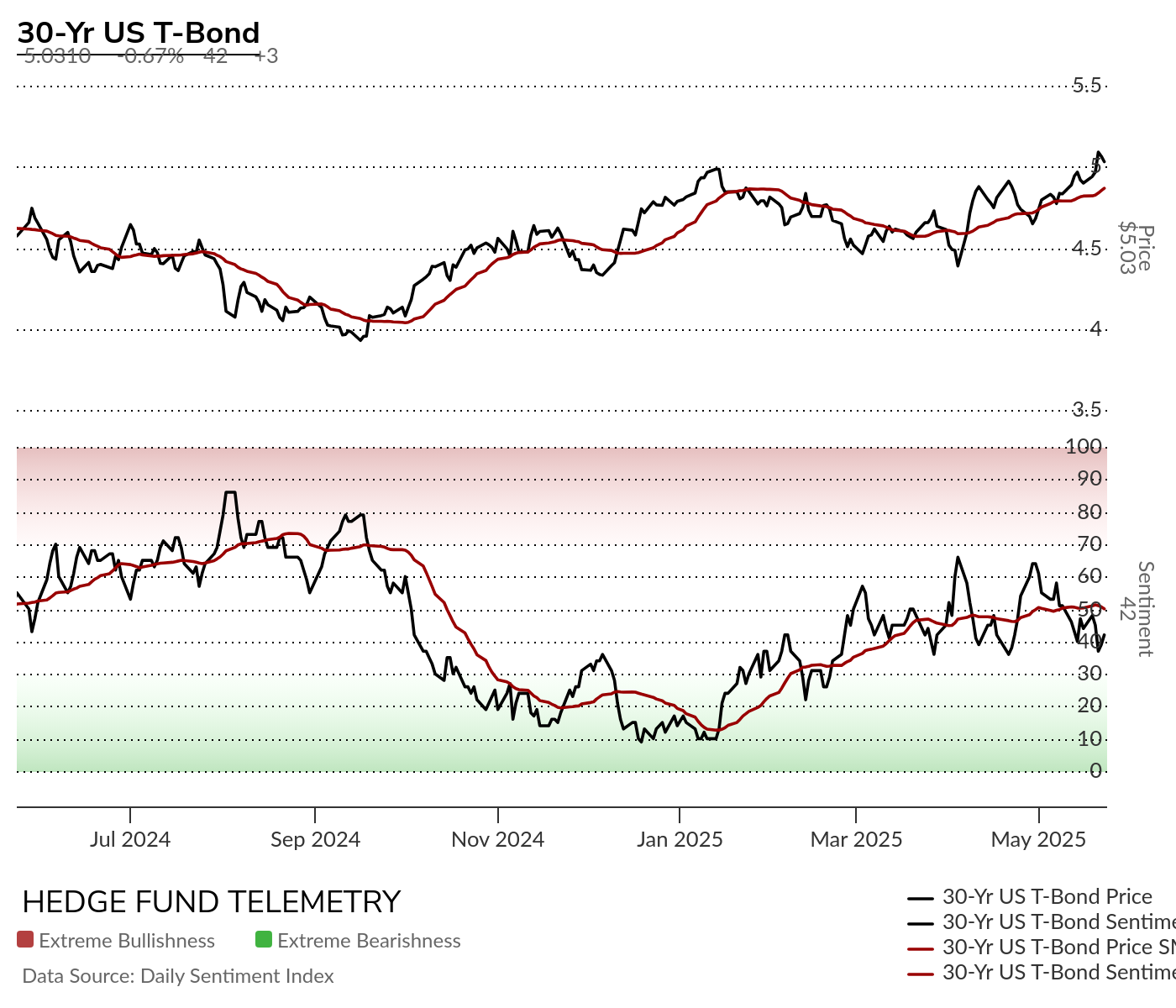

Bond bullish sentiment has support ~40% area. Sentiment at the January highs with 30 year yield was much lower so it’s possible sentiment can break down if rates continue higher.

Currency bullish sentiment with US Dollar bullish sentiment moving lower and is not quite fully oversold. Bitcoin sentiment dropped back below the extreme zone

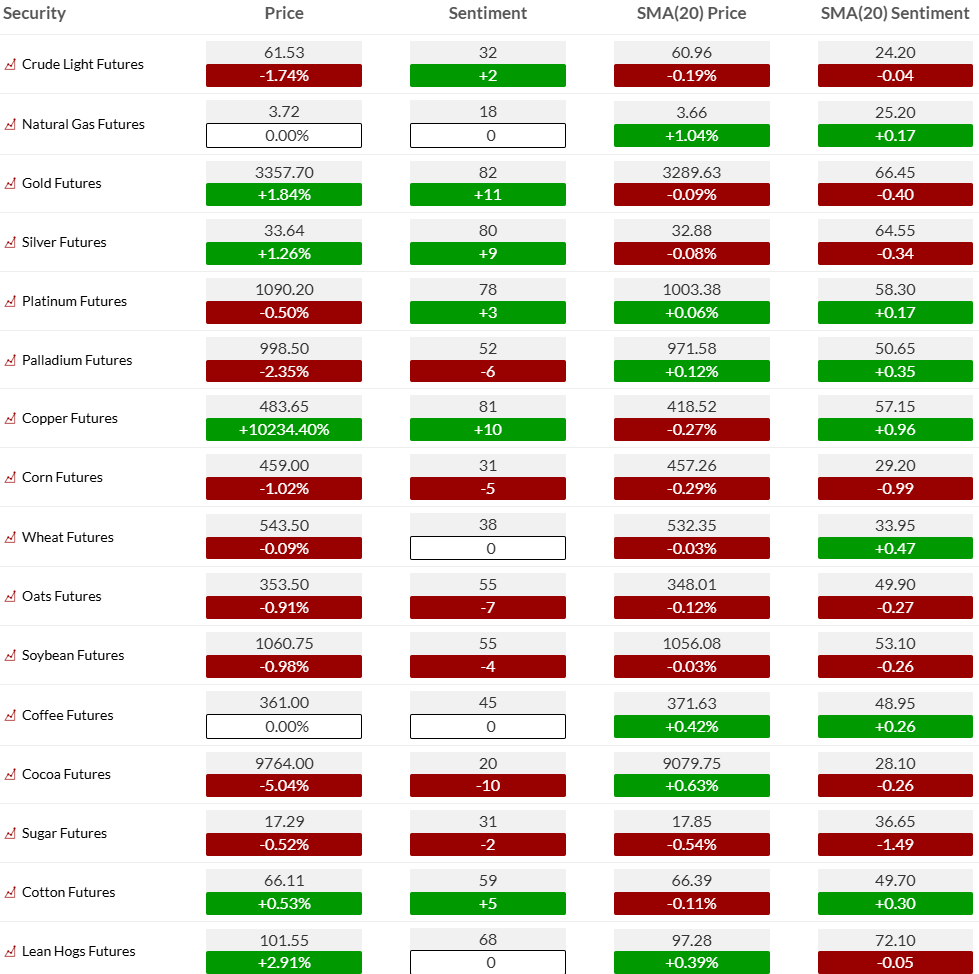

Commodity bullish sentiment highlighted with most metals sentiment in the extreme zone >80%

EARNINGS, CONFERENCES, AND ECONOMIC REPORTS

- Monday 26-May: US Markets Closed for Memorial Day Holiday

- Corporate:

- Earnings:

- Pre-open: EH

- Post-close: JOYY

- Brokerage Conference:

- Erste Bank Conference

- SAP Sapphire

- Erste The Finest CEElection Equity Conference

- Earnings:

- Economic

- Europe: PPI y/y

- Asia: Manufacturing Production NSA Y/Y

- Corporate:

- Tuesday 27-May:

- Corporate:

- Earnings:

- Pre-open: AZO, GLNG, PDD, SKY

- Post-close: API, BOX, OKTA, SMTC, SQM

- Analyst/Investor Events: TCX

- Brokerage Conference:

- SAP Sapphire

- Erste The Finest CEElection Equity Conference

- Kepler Chevreux ESG Conference

- Ambit Capital Titans of Tomorrow Conference

- Nirmal Bang Investor Conference

- Stifel Virtual Ophthalmology Forum

- Piper Sandler Virtual Lung Symposium

- Deutsche Bank dbAccess European Champions Conference

- TD Cowen Oncology Innovation Summit

- Raymond James Silver Conference

- KeyBanc Industrials & Basic Materials Conference

- TD Cowen Technology, Media and Telecom Conference

- UBS Asian Investment Conference

- Louisiana Energy Conference

- Citi Macro & Pan-Asia Investor Conference

- Earnings:

- Economic

- US: Durable Orders, FHFA House Price Index, Consumer Confidence, Redbook Chain Store, API Crude Inventories

- Europe: Retail Sales y/y, GfK Consumer Confidence, Preliminary CPI y/y, Economic Sentiment Indicator, PPI m/m

- Corporate:

- Wednesday 28-May:

- Corporate:

- Earnings:

- Pre-open: AMBR, ANF, CMCO, CPRI, DKS, ICCM, ITRN, KC, M, MNRO, PLAB, REX, RSVR, SOTK, VNET

- Post-close: A, AI, CRM, ELF, HPQ, NCNO, NDSN, NOAH, NTNX, NVDA, OOMA, PHR, PSTG, S, SNPS, UHAL, VEEV

- Analyst/Investor Events: BIVI, COHR, FA, MRKR, PFGC, YMAB

- Brokerage Conference:

- SAP Sapphire

- Erste The Finest CEElection Equity Conference

- Deutsche Bank dbAccess European Champions Conference

- TD Cowen Oncology Innovation Summit

- Raymond James Silver Conference

- KeyBanc Industrials & Basic Materials Conference

- TD Cowen Technology, Media and Telecom Conference

- UBS Asian Investment Conference

- Louisiana Energy Conference

- Citi Macro & Pan-Asia Investor Conference

- Craig-Hallum Institutional Investor Conference

- BofA Emerging Markets Corporate Conference

- Evercore ISI Nothing But Net Internet Investors Summit

- DS Investment & Securities Corporate Day

- Jefferies Technology Public Company Conference

- Stifel Jaws & Paws Conference

- Bank of America Power, Utilities and Alternative Energy Conference

- Deutsche Bank Global Financial Services Conference

- Jefferies Software & Internet Conference

- Jefferies eVTOL Summit

- Bernstein Strategic Decisions Conference

- B&K Securities Trinity India Investor Conference

- PDUFA: ETON (ET-400)

- Earnings:

- Economic

- US: MBA Mortgage Purchase Applications, FOMC Minutes, DOE Crude Inventories

- Europe: PPI y/y, Core Retail Sales m/m, Retail Sales y/y, Trade Balance, Unemployment Rate, Consumer Goods Spending m/m, PPI m/m, Final GDP q/q, Final GDP y/y, CPI y/y

- Corporate:

- Thursday 29-May:

- Corporate:

- Earnings:

- Pre-open: ALAR, AMWD, BBW, BBWI, BURL, CAL, DSX, DXLG, FL, FUTU, HLNE, HRL, JG, KSS, MOV, ROIV, SPTN

- Post-close: AEO, AMBA, COO, COST, DELL, ESTC, GAP, MRVL, NGL, NTAP, PATH, PD, RRGB, ULTA, ZS

- Analyst/Investor Events: ASH, NOTV, PAAS, SGMT, XPOF

- Brokerage Conference:

- Erste The Finest CEElection Equity Conference

- KeyBanc Industrials & Basic Materials Conference

- TD Cowen Technology, Media and Telecom Conference

- UBS Asian Investment Conference

- Louisiana Energy Conference

- Citi Macro & Pan-Asia Investor Conference

- Jefferies Technology Public Company Conference

- Stifel Jaws & Paws Conference

- Bank of America Power, Utilities and Alternative Energy Conference

- Deutsche Bank Global Financial Services Conference

- Jefferies Software & Internet Conference

- Jefferies eVTOL Summit

- Bernstein Strategic Decisions Conference

- B&K Securities Trinity India Investor Conference

- Goldman Sachs Leveraged Finance and Credit Conference

- Barrington Research Spring Investment Conference

- Benchmark Co. Healthcare House Call Virtual Conference

- Lytham Partners Spring Investor Conference

- Morgan Stanley ASEAN Conference

- Earnings:

- Economic

- US: GDP (first revision), Pending Home Sales, Weekly Jobless Claims, EIA Natural Gas Inventories

- Canada: Current Account

- Europe: Retail Sales y/y, Business Confidence, Consumer Confidence

- Asia: Industrial Production m/m, Unemployment Rate, CPI Tokyo y/y, Industrial Production m/m (preliminary), Retail Sales y/y, Retail Sales m/m

- Corporate:

- Friday 30-May:

- Corporate:

- Earnings:

- Pre-open: SCVL, TIGR

- Brokerage Conference:

- Citi Macro & Pan-Asia Investor Conference

- Bernstein Strategic Decisions Conference

- B&K Securities Trinity India Investor Conference

- American Society of Clinical Oncology Meeting

- Earnings:

- Economic

- US: Core PCE, Personal Spending, Personal Income, Wholesale Inventories, Chicago PMI, Michigan Consumer Sentiment (Final)

- Canada: GDP

- Europe: Retail Sales, Final GDP y/y, Nationwide House Price Index y/y, Retail Sales y/y, Preliminary CPI y/y, KOF Leading Indicator, GDP y/y, M3 Money Supply y/y, Unemployment rate, Preliminary GDP (second) y/y, PPI y/y

- Asia: Housing Starts y/y, Non Manufacturing PMI y/y, official Manufacturing PMI y/y

- Corporate:

Thanks to Street Account, Vital Knowledge, and Bloomberg as valued sources.