TOP EVENTS AND CATALYSTS

The week ahead will feature another week of missing key economic figures that should usually be released, as the US government shutdown will delay the data. The BLS will release the CPI on Friday, October 24th, regardless of the shutdown, as this number is required to set Social Security payments. However, everything else will need to wait for the government to reopen. The Fed’s Beige Book will be released on Wednesday afternoon, providing a critical qualitative look at the economy (the Beige Book will still be published despite the shutdown). This will be the final week of Fed speakers before the central bank enters a blackout period ahead of the October 29th Fed decision (but without incremental data, there won’t be much for them to talk about). The shutdown will last at least until Tuesday (the Senate is out of session until then, and it’s not clear when the House will return); markets have been tolerant of the US government shutdown thus far, but people will now start caring a lot more than before, given the dearth of critical data and the absence of paychecks for workers. The World Bank/IMF annual meetings are scheduled for this week in Washington (usually this wouldn’t be a huge event for markets, but it will provide a forum for US and Chinese officials to potentially address the latest escalation in economic/tariff tensions).

For earnings, the major Q3 US reports include: Monday premarket: FAST, Tuesday premarket: ACI, BLK, C, GS, JNJ, JPM, WFC; Wednesday premarket: ABT, BAC, MS, SYF; Wednesday postmarket: SLG, UAL; Thursday premarket: BK, INFY, MAS, MMC, SCHW, TRV, USB; Thursday postmarket: CSX; and Friday premarket: AXP, FITB, RF, SLB, STT, TFC.

The major EU/Asia reports include: Tuesday: Ericsson; Wednesday: ASML; Wednesday late: LVMH); Thursday: Nestle, TSMC; and Friday morning (Publicis).

Two tech conferences take place, including Oracle’s AI World and Salesforce’s Dreamforce.

Weekend News

- Investors are still digesting Trump’s China tariff bombshells from two social media posts on Friday, the first one, which caused stocks to plunge in the final 5 hours of the session and finished at their lows. And a second one after the bell (in which he outlined plans to impose an incremental 100% tariff on Chinese imports starting Nov 1st). Many took heart in the Nov 1st deadline as it left a period of several weeks during which cooler heads could prevail. China published a statement on Saturday night, which was mixed. On the one hand, Beijing sounded defensive and defiant, blaming Trump for failing to honor the détente reached at the Madrid meeting by enacting a series of escalatory actions. However, China also offered reassurances on rare earths, stating that the restrictions imposed last week would have minimal actual impact, and insisting that foreign companies “need not worry” about receiving the desired allocations.

- Today, Trump has posted on social media a possible off-ramp for Chinese President Xi Jinping while issuing a veiled threat that a full trade war would wound China. This suggests that the US wants to maintain pressure on China to reverse its most recent trade moves, while trying to reassure spooked markets that a tit-for-tat escalation isn’t inevitable. This is likely to result in a bounce in equity markets, as crypto, which had experienced steep declines, is rebounding today.

- House Republicans remain dug in on shutdown talks, refusing to countenance an extension of Obamacare subsidies until the government reopens Politico

- WBD (Warner) has rejected PSKY (Paramount)’s initial takeout bid of $20/share. In recent weeks, as being too low (Paramount has some options, including raising its offer, bringing on outside financial partners, or going directly to WBD shareholders) Bloomberg

The Currency and Commodity notes will be published tonight or first thing in the morning.

Market thoughts

It didn’t take much to pop the complacency bubble. Tariffs, which had been off the radar, resurfaced and reminded investors of the risks associated with tariff trade wars (and Trump’s tweets!). The backdrop of investors of all types being “All In”, leveraged, and complacent remains, and essentially a one-day drop might be the start of a risk-off period. It might not be as steep as Friday; however, this has likely woken up some risk managers to dial back their exposures. Nothing is yet oversold, including sentiment, which is holding above the lows seen back in August. With Trump offering an off-ramp of sorts (a mini TACO) to China, expect bounces; however, investors will be more on edge regarding tariff developments.

Adding to the mix of risk is the recent credit earthquakes. Considering that some companies are facing serious debt problems due to the economy, while markets are relatively strong, the cockroach theory is on my list of concerns to monitor. Then we will see Q3 earnings season ramp up with a high bar, expecting strong 8% earnings growth. Bank CEO comments will be in focus with consumer trends and recent credit worries likely to be addressed.

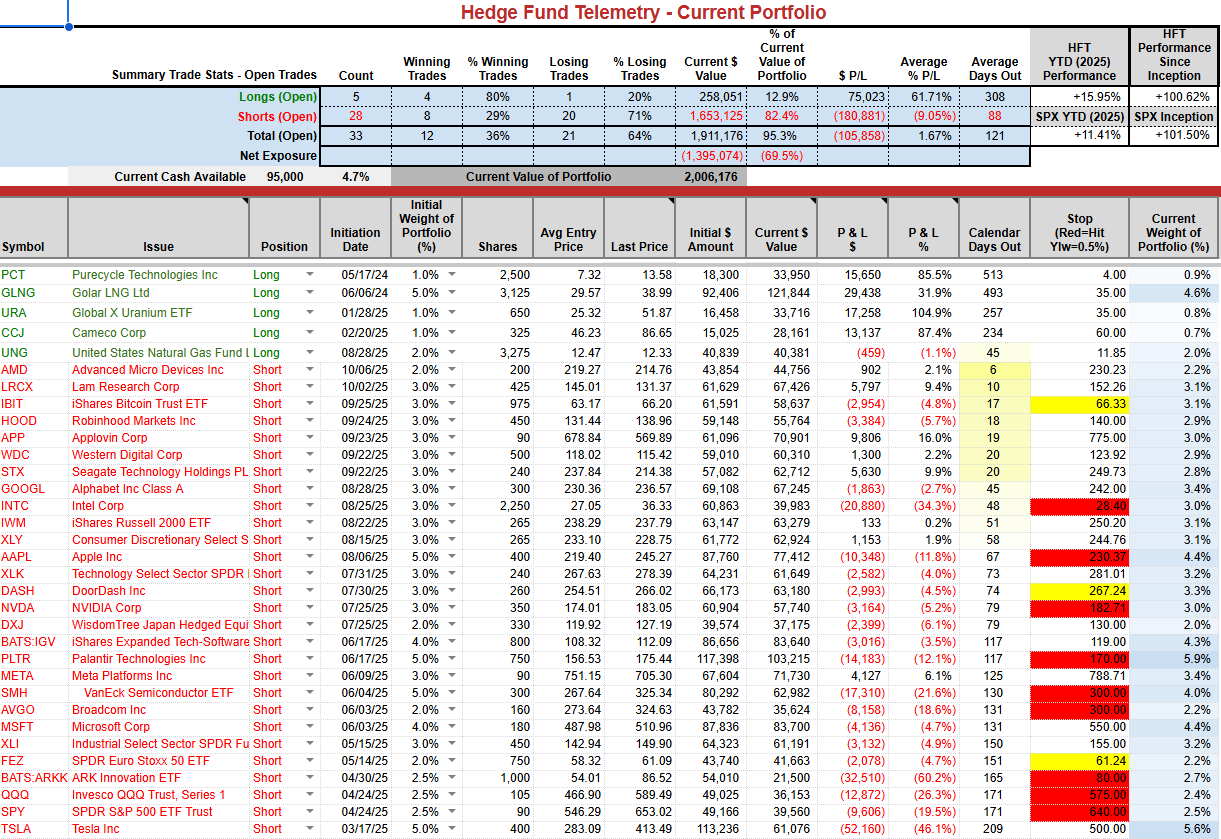

Trade Ideas Sheet update

Friday’s downside move had a significant upside move to +15.95 YTD, compared to the S&P’s +11.41%, which I could see giving back some gains with a market bounce.

Charts we are watching

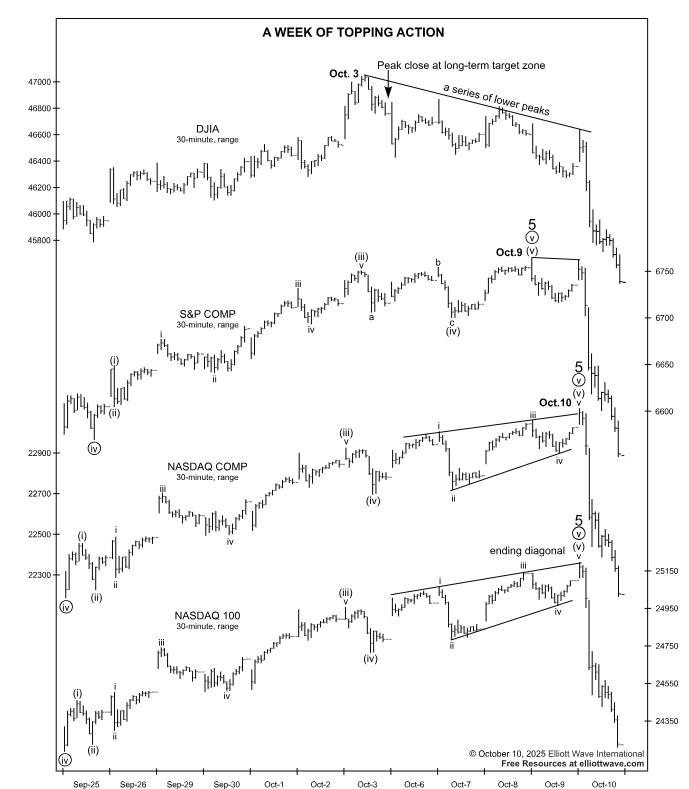

Even before Friday’s action, there were signs of weakening and diagonal triangles. This is from my friends at Elliott Wave, who have been showing a lot of long-term upside targets that they had recently met.

S&P 500 index daily with a significant drop on Friday after the sell Setup 9. It still held the 50 day and it’s been something like 115 days above the 50 day which is unique and rare. This broke the Reference Close and TDST Setup Trend support which will see the pending Sequential and Combo’s cancel this week.

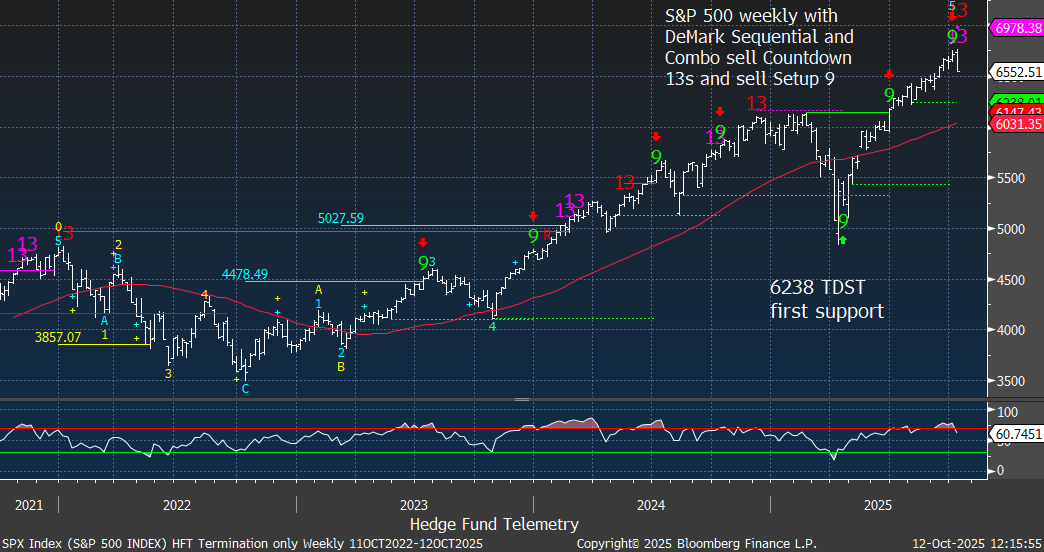

S&P 500 weekly did qualify last week the Sequential and Combo sell Countdown 13s with the previous week’s sell Setup 9. If anything, either this is an intermediate top in wave 5 or a period of stalling ahead.

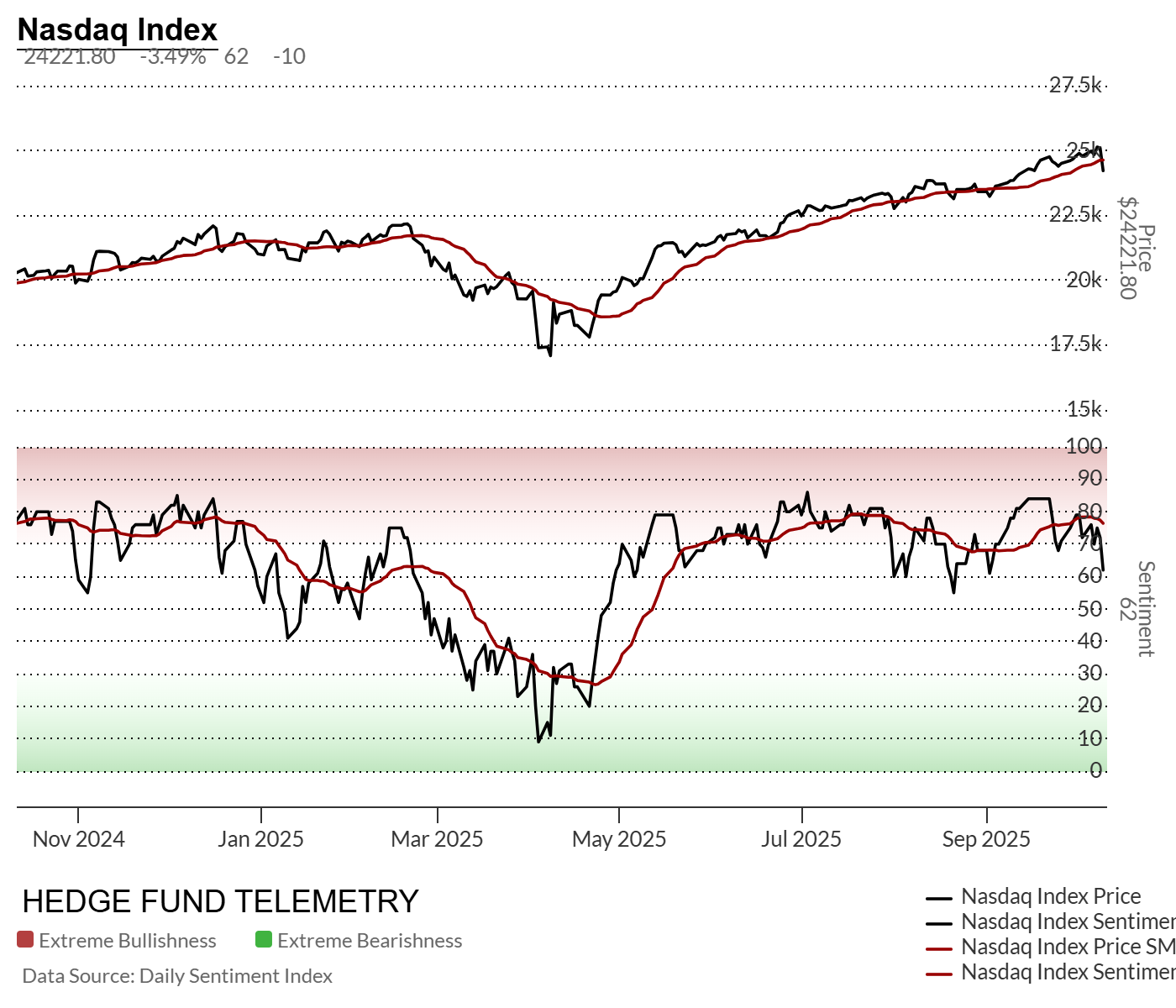

NDX daily also broke some important levels except the 50 day.

Nasdaq weekly with two versions of the Combo 13 (standard default and version 1c). Also cut off is another sell Setup 9. the Sequential is left pending on week 11 of 13. A new high is not necessarily needed for the Sequential 13 as the 8th week high was 24,137 which is lower than the current price.

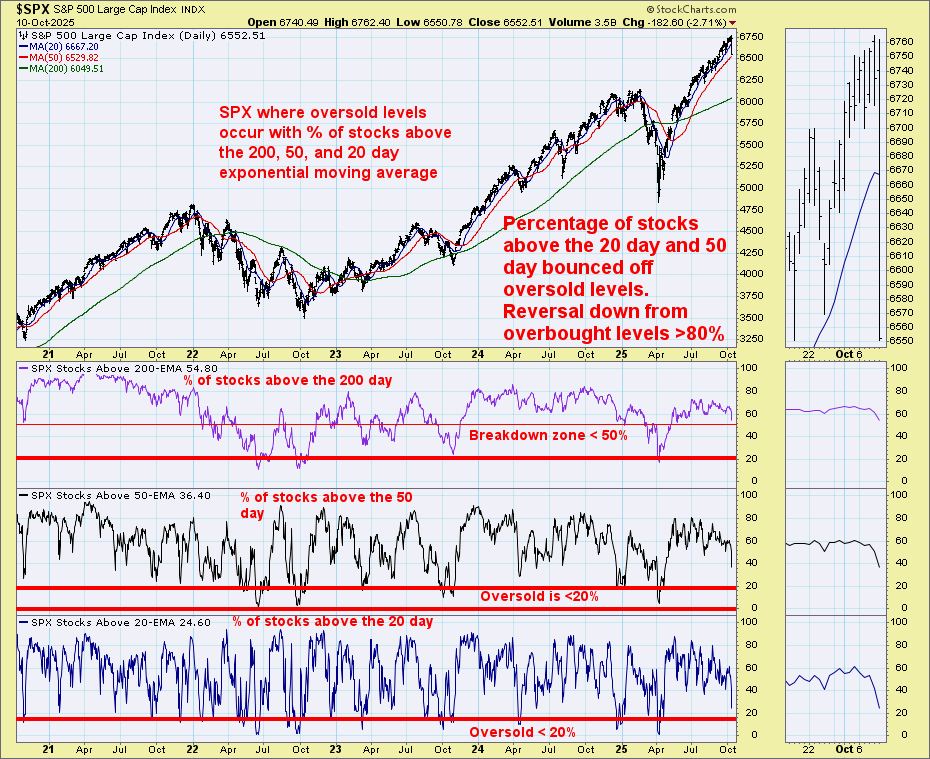

The S&P, Midcap, and Smallcap advance-decline data spiked lower on Friday and are not yet oversold as compared to other buying opportunities.

One of our easiest to replicate and use effectively for good oversold conditions is the percentage of stocks above the 20, 50, and 200 day moving averages. Back in April these were deeply oversold and it gave us conviction on shifting long. Recently these have moved off highs and held above 50%-60%. The narrowing of the mega-cap, which has been doing the majority of the gains, has caused the divergences. Friday’s action shifted these lower, but not at oversold levels.

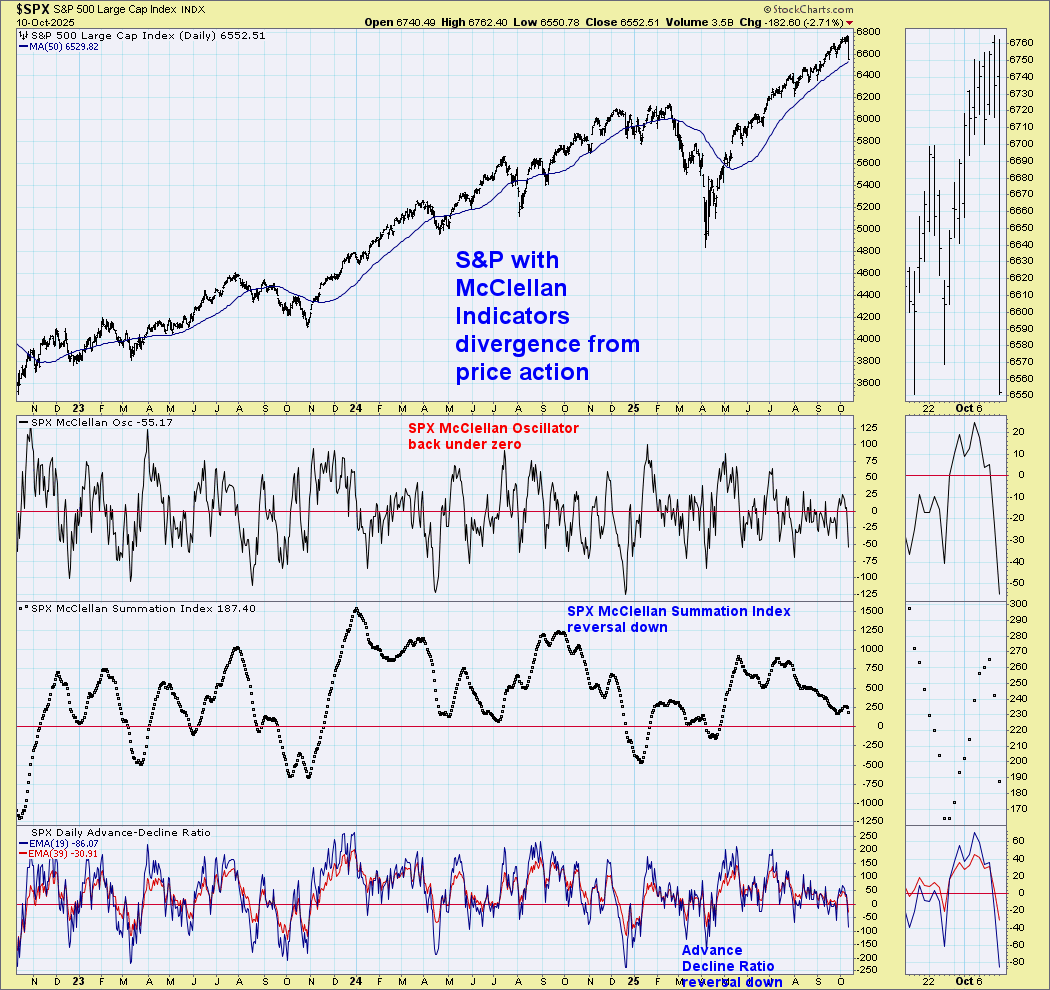

The S&P with the McClellan indicators has been negatively divergent for a while, and after another brief bounce, fell again and is not oversold.

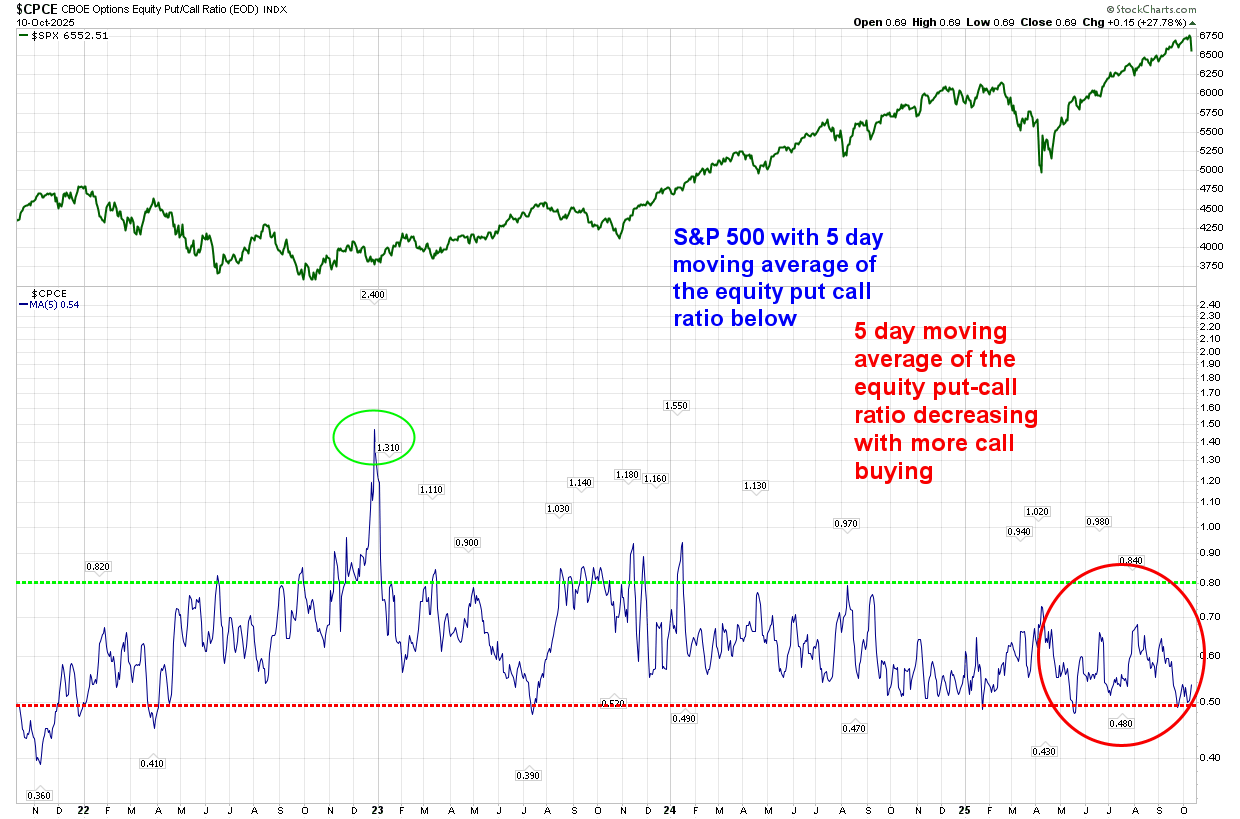

The 5 day moving average of equity put call ratio has been very low with heavy call buying which I have illustrated recently. We will hope to be buyers in the market when this lifts higher. I do think the call buyers will be back if this is just another TACO Trump trade.

The short-term SPY and QQQ momentum indicators turned to sell well ahead of the larger decline. The 50 bar (65 minute/bar) has held since April

US economic data for the week

KEY MARKET SENTIMENT

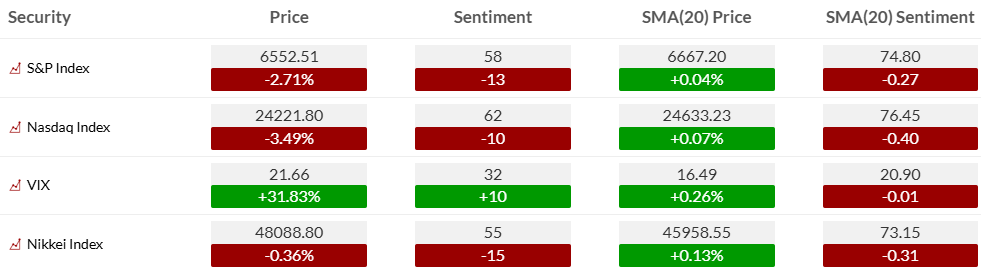

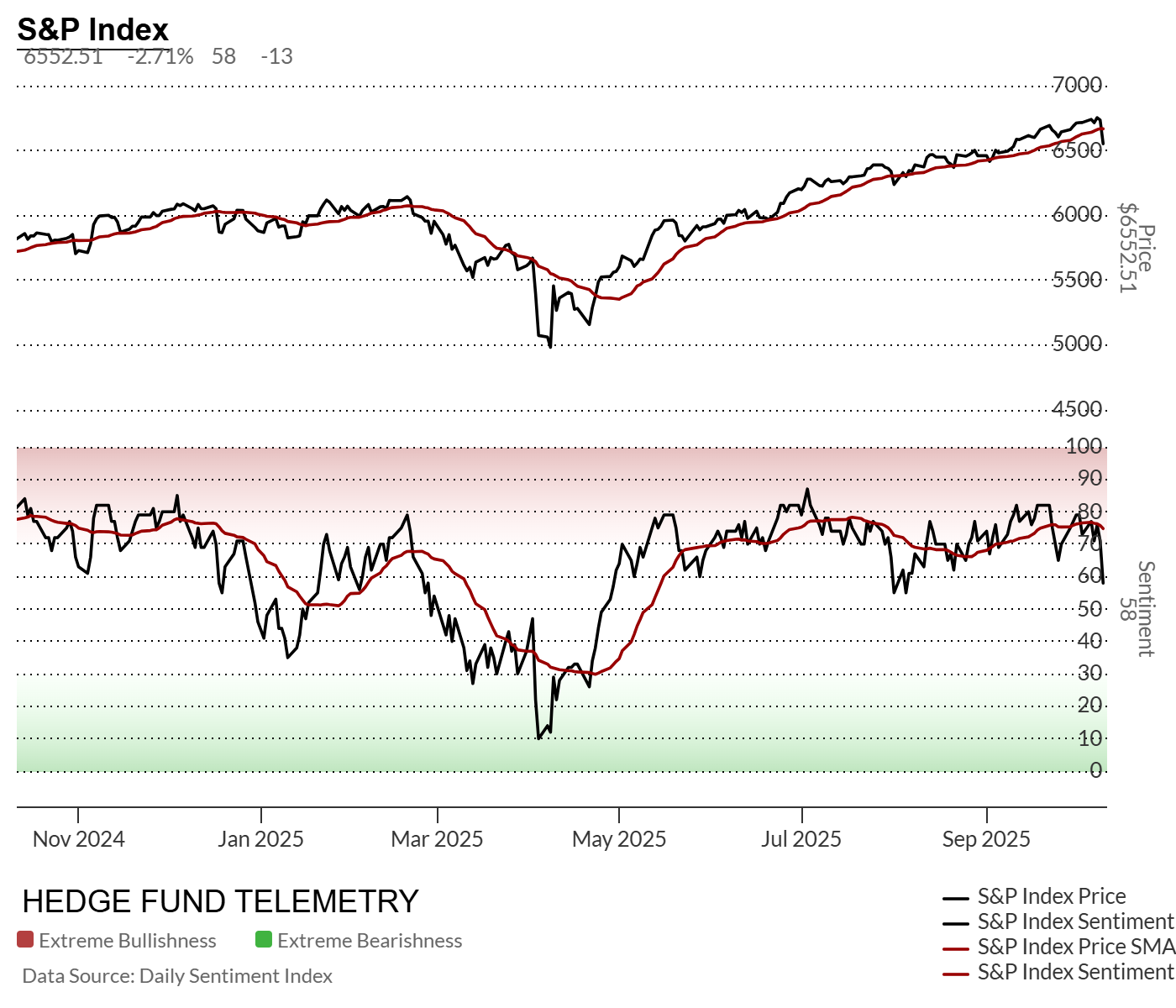

Equity bullish sentiment took a hit on Friday with the significant index declines.

S&P and Nasdaq bullish sentiment both fell significantly on Friday, but remain well above the lows from the summer. Watching the 20-day moving average of bullish sentiment, which is now decreasing again. This will be something to watch on the First Call notes in the coming weeks.

Bond bullish sentiment with a substantial ‘risk off’ type of bid on Friday

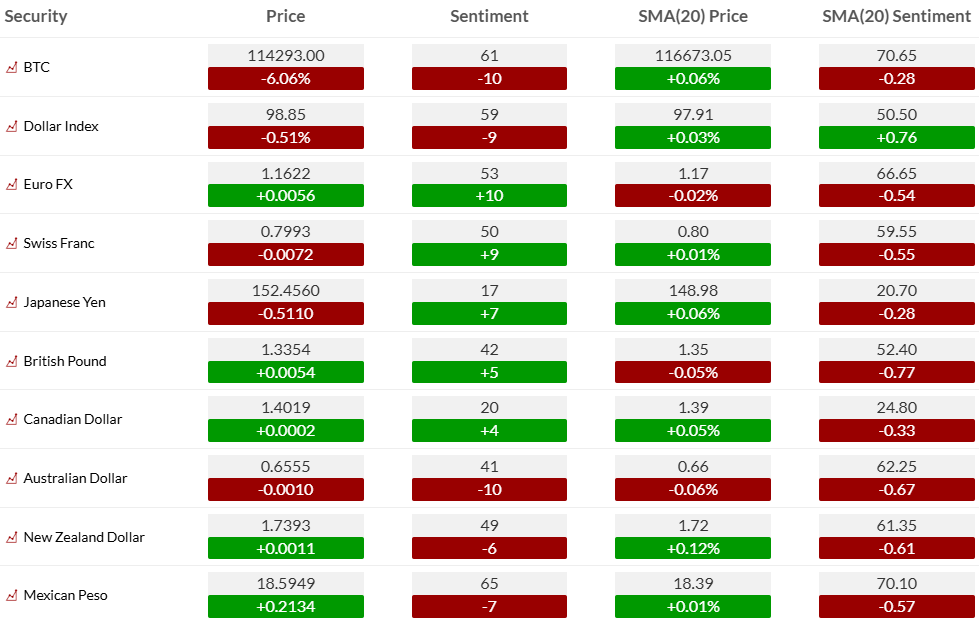

Currency bullish sentiment with US Dollar bullish sentiment dropping hard after reaching the highest level in months. Bitcoin, despite a deep decline, remains well above the 50% midpoint majority level.

Commodity bullish sentiment ex gold and silver it was a rather weak Friday with some large sentiment declines

EARNINGS, CONFERENCES, AND ECONOMIC REPORTS

- Monday 13-Oct:

- Corporate:

- Earnings:

- Pre-open: FAST

- Analyst/Investor Day Events: PLUG

- Brokerage Conference:

- Deutsche Bank Leveraged Finance Conference

- Earnings:

- Economic

- Europe: Industrial Production m/m

- Asia: GDP NSA Y/Y (Preliminary)

- Corporate:

- Tuesday 14-Oct:

- Corporate:

- Earnings:

- Pre-open: ACI, BLK, C, DPZ, FBK, GS, JNJ, JPM, SOTK, WFC

- Post-close: EQBK, HWC, KARO

- Analyst/Investor Day Events: ACRS, BCE, BZH, GANX, GIS

- Brokerage Conference:

- Deutsche Bank Leveraged Finance Conference

- Jefferies Regis Philippines Conference

- Earnings:

- Economic

- US: NFIB Small Business Index, Redbook Chain Store, API Crude Inventories

- Canada: Building Permits

- Europe: CPI y/y, ILO Unemployment Rate, PPI y/y, ZEW Economic Sentiment Indicator

- Asia: CPI y/y, PPI y/y

- Corporate:

- Wednesday 15-Oct:

- Corporate:

- Earnings:

- Pre-open: ABT, BAC, BSVN, CFG, FHN, MS, PLD, PNC, SYF

- Post-close: BANR, EPAC, FR, GSBC, HOMB, JBHT, PNFP, REXR, SLG, SNV, TFIN, UAL

- Analyst/Investor Day Events: BF.B, CRM, DLTR, GCMG, HPE

- Brokerage Conference:

- Deutsche Bank Leveraged Finance Conference

- Jefferies Regis Philippines Conference

- Earnings:

- Economic

- US: MBA Mortgage Purchase Applications, CPI, Empire Manufacturing, DOE Crude Inventories

- Canada: Manufacturing Sales, Wholesale Inventories, Wholesale Trade

- Europe: Trade Balance, CPI y/y, Industrial Production y/y

- Asia: Industrial Production m/m (revised), Retail Sales NSA y/y, Core Machinery Orders m/m

- Corporate:

- Thursday 16-Oct:

- Corporate:

- Earnings:

- Pre-open: BK, CMC, IIIN, KEY, LOOP, MAN, MMC, MTB, SCHW, SNA, TRV, USB

- Post-close: CSX, FNB, GBCI, IBKR, LBRT, OZK, SFNC

- Analyst/Investor Day Events: JEF, VEEV

- Brokerage Conference:

- Jefferies Regis Philippines Conference

- Earnings:

- Economic

- US: Philadelphia Fed Index, PPI, Retail Sales, Business Inventories, NAHB Housing Market Index, Weekly Jobless Claims, EIA Natural Gas Inventories

- Canada: Housing Starts

- Europe: Unemployment Rate, Construction Output y/y, Trade Balance, CPI y/y, Industrial Production y/y

- Asia: Unemployment Rate, Non-Oil Domestic Export NSA Y/Y

- Corporate:

- Friday 17-Oct:

- Corporate:

- Earnings:

- Pre-open: ALLY, ALV, AXP, CMA, FITB, HBAN, INDB, RF, SLB, STT, TFC

- Brokerage Conference:

- European Society of Medical Oncology Congress

- Earnings:

- Economic

- US: Building Permits, Import/Export Prices, Housing Starts, Capacity Utilization, Industrial Production, TIC Flows

- Europe: Unemployment Rate, CPI y/y, PPI y/y

- Corporate:

Thanks to Street Account, Vital Knowledge, and Bloomberg as valued sources.