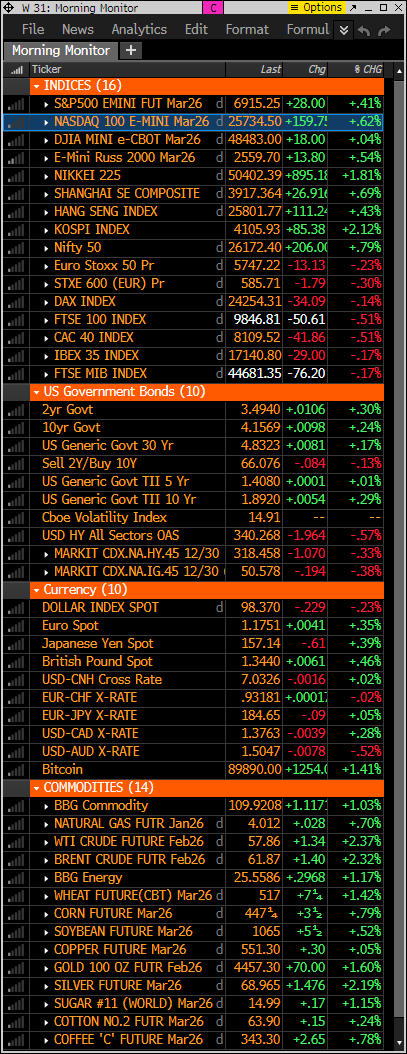

Premarket Price Action

- US equity futures: S&P +0.35%, Nasdaq +0.6%, Dow flat, Russell 2000 +0.45%

- Treasuries: yields +1 bp (flat-to-up across curve; long end slightly firmer in spots)

- Dollar: DXY -0.2% (after last week’s run; yen still soft)

- Crypto: Bitcoin +1.35%

- Commodities: Gold +1.5%, Silver +2.1%, Crude +2.35%, Natural Gas up 2.35% (see crude and natural gas charts below as they could build on top of these gains after recent DeMark buy Setup 9’s)

Premarket Setup

Futures are higher to start the week, extending last week’s year-end bid with AI/tech risk-on tone still the dominant factor. S&P and Nasdaq 100 futures are near and could have a new DeMark Sequential sell Countdown 13 today or tomorrow. Asia: Strong across the board (Japan, Korea, Taiwan standout); tech notably firm (semis and AI-linked names led). Europe: Down ~10–15 bps; defensives and rate-sensitive groups weaker while energy/tech/basic resources relatively better. I will be on Maggie Lake’s YouTube channel live at 4 pm today.

What’s Driving Markets

- AI bid persists: follow-through from last week’s AI leadership, helped by weekend headlines on OpenAI’s improving compute margins and continued AI leadership chatter around large-cap tech.

- Geopolitics lifting crude: Ukraine negotiations remain unresolved and US scrutiny of Venezuelan shipments is rising; oil is catching a bid.

- Macro is quiet: nothing on the calendar today; the tape is more positioning + seasonality than data-driven. Lack of sellers vs strong volume on upside.

- Rates steady, Fed path unchanged: next cut expectations remain centered on March–April, keeping conditions supportive into thin holiday liquidity.

- Short-term S&P 60-minute futures have DeMark Sequential sell Countdown 13’s in play after the bounce late last week.

Macro & Policy Focus

- No major US data today.

- Treasury supply begins: $69B 2-year auction today (then 5s Tuesday, 7s Wednesday).

- Fed messaging: Cleveland Fed’s Hammack reiterated a “steady for some time” posture pending clearer inflation/labor signals—hawkish tone but consistent with recent rhetoric.

- Geopolitical backdrop: Ukraine talks continue without breakthroughs; the oil market is increasingly sensitive to any disruption narratives, especially now with Venezuela.

- NVDA: seeking to begin shipping H200 chips to China customers (mid-Feb timeline).

- OpenAI: reports of improving compute margins on paid products.

- TSLA: Delaware court restored Musk’s 2018 pay package (headline supportive for sentiment, not fundamental).

- NFLX / WBD: Netflix reportedly refinanced part of bridge financing tied to efforts to buy WBD (headline-driven).

- ORCL / OpenAI / data center buildout themes remain in the background, but holiday tape likely limits follow-through.

Key S&P 500 Upgrades / Downgrades – none

What We’re Watching Today

- Thin holiday liquidity: does risk-on broaden beyond AI/tech?

- Oil sensitivity to Ukraine/Venezuela headlines

- Treasury auctions as the week’s main “macro” event

- Yen weakness and USD stability as cross-asset tells

Bottom Line

This is a quiet, seasonal, positioning-driven start to the holiday week, with AI/tech tone still carrying the tape and oil firming on geopolitics. Sentiment is rebounding sharply, but leadership remains concentrated—follow-through requires breadth beyond the usual high-beta complex.

market snapshot

economic reports today

premarket trading

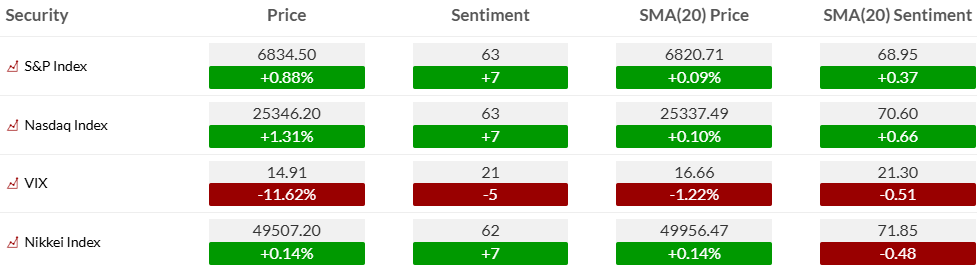

US MARKET SENTIMENT

S&P bullish sentiment: 63%, +7 day/day — notable rebound in optimism after last week’s wobble.

Nasdaq bullish sentiment: 63%, +7 — sentiment snapback confirms tech remains the emotional driver.

VIX sentiment: 21%, -5 — edging toward downside extreme (<20), consistent with fading near-term hedging demand.

Risk framing: sentiment has pushed back above neutral; the next real risk tell is whether it holds

Bond bullish sentiment is hanging around the 50% midpoint level

FX: Yen sentiment 13%, -8 → downside extreme (continued JPY stress post-BOJ). Dollar sentiment 70%, +6 (still elevated).

Crypto: BTC sentiment 17%, +5 → still near downside extreme despite price strength (contrarian setup if risk-on persists).

Commodities: Platinum 88% and Palladium 88% remain upside extremes; Silver sentiment 77%, +7 (hot); Crude sentiment 45%, +5 (improving, not extended).

US MARKETS

S&P futures 60-minute tactical time frame with Sequential and Combo 13 still in play after the recent bounce.

S&P futures daily could qualify the Sequential sell Countdown 13 today. To complete a Countdown bar thirteen must be greater/less than or equal to the close of the 8th bar and the normal pattern of the 13th bar must be greater/less than or equal to the high/low of two earlier bars. The 8th red bar close is 6918

Nasdaq 100 60-minute tactical time frame with new Sequential and Combo sell Countdown 13’s after the recent bounce

Nasdaq 100 futures daily with Sequential on day 12 of 13. 8th red bar close is 25,859 needed tomorrow or in coming days to qualify the Sequential sell Countdown 13.

Extra charts we’re watching

Crude has been in downside trend however I expect higher prices in 2026. New DeMark buy Setup 9 on Friday with price flip up today. 50 day has been resistance from Summer. A “price flip” is defined as a contra-trend move identified by a close that is higher/lower than the close four price bars earlier.

Natural Gas bouncing today after recent buy Setup 9. Recommend buying Natural Gas still

US Dollar Index daily reversing a few days of gains. Mostly remaining in the range from Summer

US 10-Year Yield remains just below the breakout level

Bitcoin Daily holding steady yet I still believe this will qualify into downside wave 5

DeMark Observations – Euro Stoxx 600