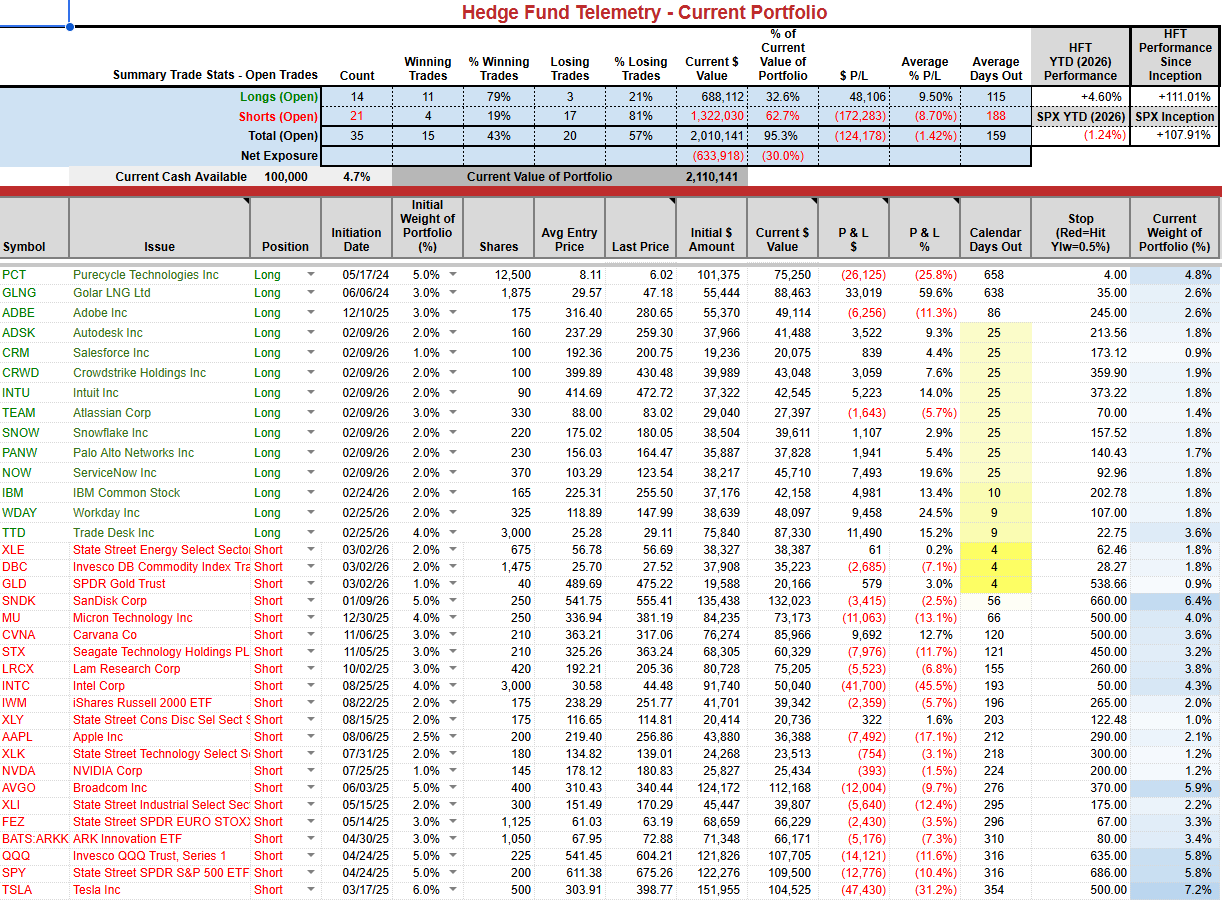

- Happy Friday, everyone! It’s been hairy in the markets this past week and seemingly every week this year. I am gratified with the positioning and performance of a few of our themes. Volatility creates opportunity, and we’ve been finding it. Our PNL is leading the S&P by 500bps, and having both longs and shorts generating alpha creates some PNL durability. As I said recently, I have a lot of alpha I expected to work and move the PNL, which has moved 10% from its recent low to its current level, +4.6% vs S&P, -1.25%. It’s a long year and a lot more work to do.

- The markets during times of war will shift between the narratives of containment and escalation. Today, it’s escalation leading the narratives.

- Software vs semi’s are starting to work, more so by software recovering while most semi’s are well off highs.

- The Iran war has continued, with widespread, obvious fears about oil supply and shipping shocks. I had dinner with Paulo Pereira this week, and he outlined some risks in the energy markets. He has expected higher crude prices, which oil companies typically hedge, locking in gains. Some of the energy company stocks have stopped rising in sync with crude prices. That might be partly the hedge. The risk for hedged companies is that crude prices spike again, causing a squeeze that would hurt energy companies. He’s the expert and has more to talk about on his Substack. I was asked why energy companies stopped going up in sync, and again, that is my short take.

- Inflation data has been coming in stronger, and the February CPI is due next week. One big contributor to inflation declining in the 2nd half of 2025 was a drop in gasoline prices. Gasoline prices bottomed in mid-January and rose by 6.75% by the end of February. People will comment next week regarding the CPI: gasoline prices rose because of the Iran war, but the data were already in before the war, and now, from the January low, gasoline prices are up 19%. Therefore, expect the next few months of inflation data to show these increases. Add in prices for industrial metals and other commodities that have also lifted to filter into higher inflation data.

- “The worst case scenario” was the comment by Fed Governor Austin Goolsbee regarding higher inflation and weaker jobs data. Stagflation risk isn’t something the Fed can wave its magic wand at and fix both problems together.

- The major indexes have moved within a narrow range since October, while dispersion has remained elevated, partly due to crowded positioning on both the long and short sides. I remain focused on exploiting the positioning crowding.

- At times, there are times to plant seeds in the ground and times to prune the fruit. It can be the same way with a portfolio. I’m bullish on Pure Cycle and bought this a while back at a lower price (and it went lower) and sold at a higher price, locking in 125% gains. I was specific that I would buy it back lower, which I have, including adding more recently. The company is in a much better position than it was the last time it traded at this price. It’s a high-risk, high-reward type of stock with the management doing a great job of eliminating each short thesis. The CEO said 2026 is about customers after perfecting the plastic recycling plant and a few other short thesis narratives. The company has 140 potential customers trialing their product. Governments have future mandates for companies to source recycled plastic. For me, it’s not a matter of if but when the customers sign on.

- Months ago, I wrote about how new rules allowing retail investors to invest in private companies/credit through various ways, including ETFs. Giving PE firms this liquidity was a risk, as I saw that dumping illiquid stuff into retail accounts wasn’t going to end well. Now we’re seeing gates or limits on withdrawing funds from those vehicles. If you have ever invested in a PE fund and tried to get out, you know exactly what I’m talking about. It’s not cockroach theory; it’s Roach Motel: you can check in, but you can’t check out.

- This story, “Meet the finest boys in finance,” is getting some attention. Not in a good way for the finest boys. In a memoir published this week, former Chief Executive Officer Lloyd Blankfein recalled a 1986 incident when Jim Cramer, then a 31-year-old retail broker at Goldman, boasted of his wealth to the New York Times. “There isn’t anything I see in a store that I can’t buy,” Blankfein added: “He was gone from the firm shortly thereafter.” Inverse Cramer was born!

- A proposed class action against prediction market Kalshi should’ve paid out $54 million on a market speculating when Iran’s Supreme Leader Ali Khamenei would vacate his role after he was killed during US and Israeli airstrikes. The complaint alleges Kalshi didn’t adequately disclose a “death carveout” until after news of Khamenei’s death spread, and instead lured more traders into “yes” positions while knowing it wouldn’t deliver payouts. Hard pass for me and prediction markets trading.

- I’m excited for Baseball season to start up. Shohei Ohtani hit a grand slam yesterday for Japan over Taiwan 13-0 in the World Baseball Classic. The game was called after seven innings under the mercy rule, which is being used in the WBC. The game is called after five innings if a team leads by 15 runs or more or after seven if the lead is 10 or more.

- I used to run a March Madness pool for our firm. Should I do one for Hedge Fund Telemetry subs? How much per entry? If anyone wants to help with this, let me know.

- F1 season starts this weekend with the Australian Grand Prix. New cars, new power units, a few new drivers, and a new US team. Mercedes looks very good, Ferrari too. Red Bull and McLaren might be a touch below their recent championship performance. With the time difference, don’t tell me who won.

- Headed to the hospital to meet my new grandson. I feel grateful for my healthy and growing family. And grateful for all the continued support for Hedge Fund Telemetry. Welcome to those newer subscribers, and thank you. Have a nice weekend!

Quick Market Views

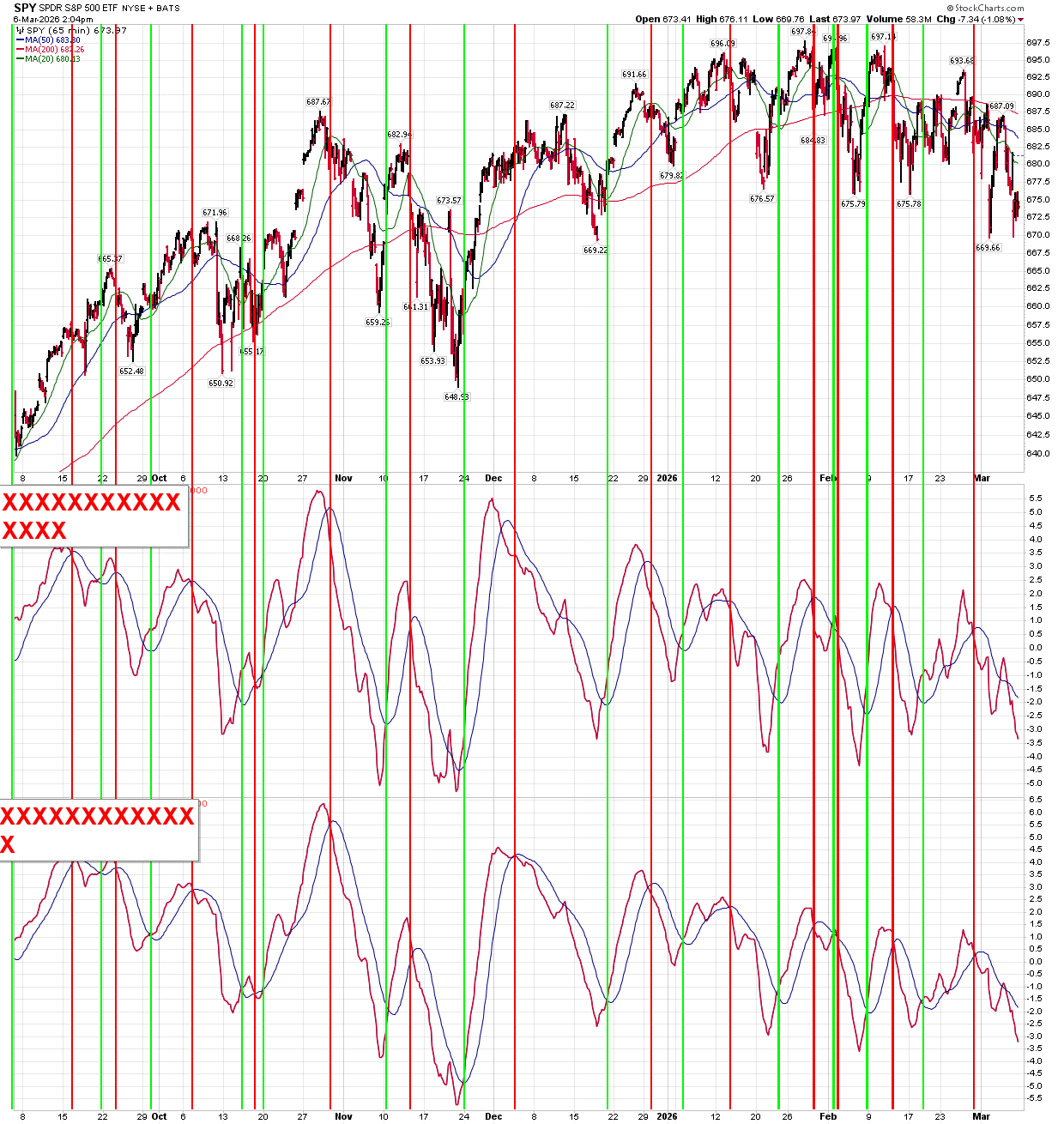

Stocks: Nasty action but well off lows and for now above the SPY and QQQ VWAP levels. Breadth is weak with NYSE with 2275 net down issues, Nasdaq with 1850 net down issues. S&P with 119 up and 384 down. NDX with 30 up and 70 down. Russell 2000 with 310 up and 1607 down. All the sectors are lower ex energy.

Bonds: Rates reversed back down now down 1-2bps

Commodities: Strong across the board. Crude up 11.50%, Natural Gas up 6.50%, Grains very strong with Wheat leading up 5.7%. Copper up 0.3%, Gold up 2%, Silver up 3.3%

Currencies: US Dollar is down 0.35%. Bitcoin is down 4% nearly back under 68k

Current Portfolio Ideas:

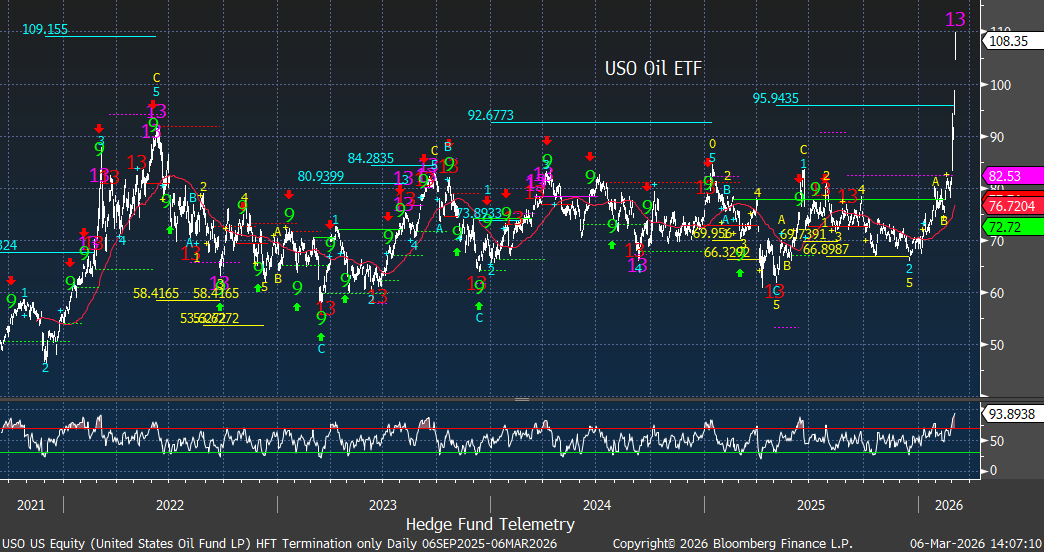

Changes: I wanted to add a new 2% weight USO Crude ETF short. UPDATE – MOST BROKERAGES WON’T LET PEOPLE SHORT THIS, SO I WILL NOT BE SHORTING THIS TODAY.

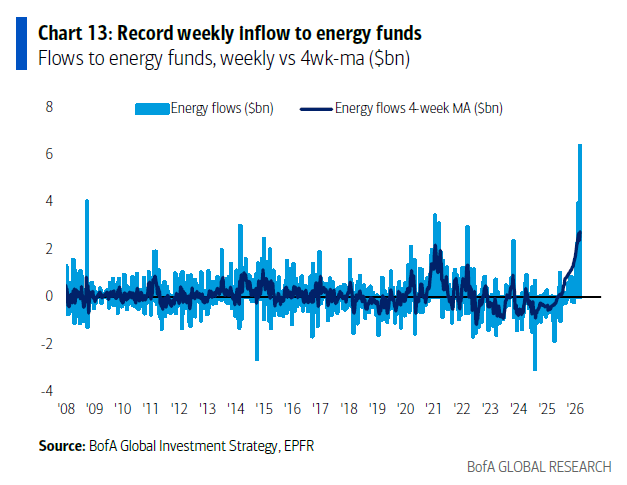

Thoughts: Fading the record inflows has worked well – see a few from the latest BofA Flow Show below.

US INDEXES

S&P futures 60-minute tactical time frame a bit weaker looking vs Nasdaq with this making a new low earlier today

S&P 500 Index daily still under 6800 the recent support. A lot of days showing bounces off lows. When that changes the market is in trouble. A lot of buy the dip mentality out there.

Nasdaq 100 futures 60-minute tactical time frame sideways mess holding recent lows

Nasdaq 100 Index daily has been making lower highs while holding the TDST Setup Trend support at 24,239

Current Portfolio

Pre changes

The short term SPY and QQQ momentum is on sell signals. Yesterday for a minute this turned to buy but with choppy nature I have been giving the signals a little more time to be clear. The sharp whips and gaps make trading momentum difficult.

USO Oil ETF with new Combo sell Countdown 13. RSI is extremely overbought. It can and might go more however I’m going to short a 2% weighted position with this also 41% above the 50 day. I’ll be interested to see tonights Crude sentiment!

flow show – fade the record flows

Bank of America’s Flow Show had a few charts that I thought I’d highlight as they have been informative recently, selling into the large inflows and buying the outflows. Record inflows into energy funds. It has also cleared any funds that were short. I am short XLE.

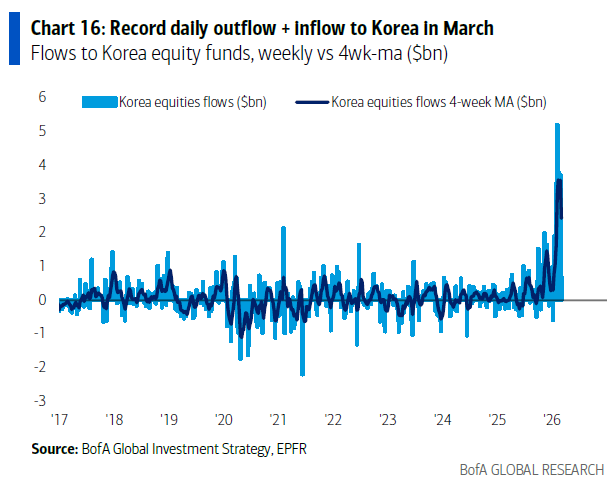

I highlighted the record inflows into Korean equity funds and added to EWY short and then covered with it, getting whacked hard. I still like this short, but I will look for a new entry-level.

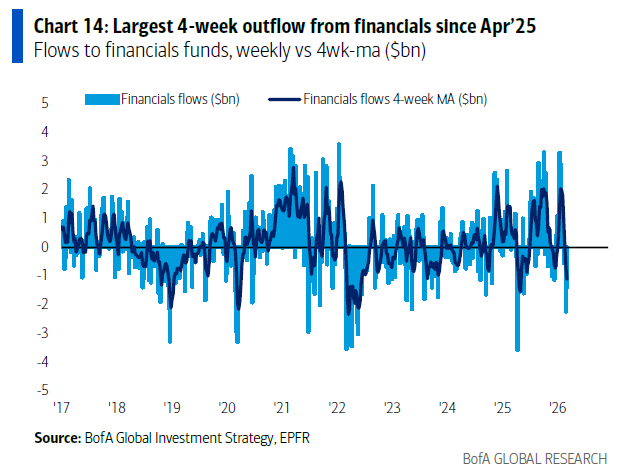

They jammed into Financials not too long ago and have been selling. Come April, ahead of earnings, these might be at buyable levels.

s&P heat map

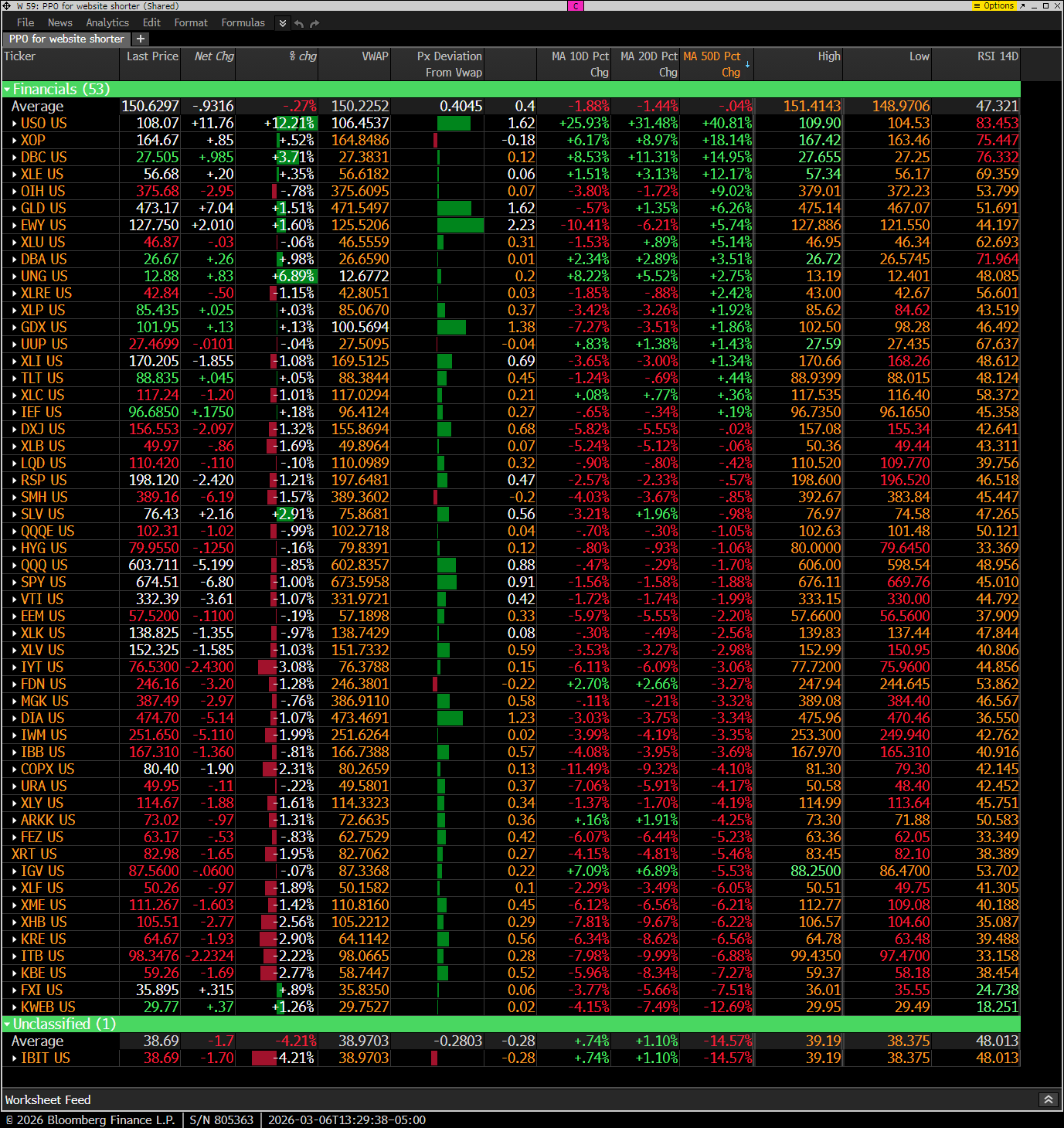

Hedge Fund Telemetry ETF Percentage Price Oscillator Monitor

The PPO monitor (percentage price oscillator) force ranks ETFs by percentage above/below the 50-day moving average. This monitor and others are offered to Hedge Fund Telemetry subscribers on Bloomberg. Most ETFs are lower today while they are mostly above today’s VWAP levels. A sign of underlying buying, however, watch SPY VWAP at 673.60 and QQQ VWAP at 602.83, as they are slightly above the VWAP. If those levels break, it could get slippery into the close ahead of the weekend.

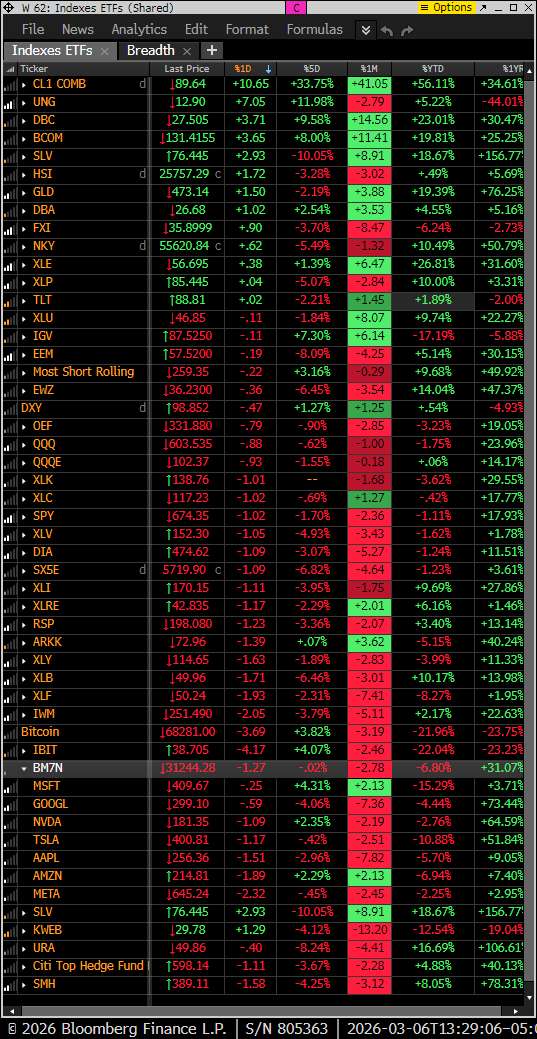

Index ETF and select factor performance

ETF with today’s performance with 5-day, 1-month, and 1-year rolling performance YTD. Every Mag7 stock is down YTD with the basket down 6.8%.

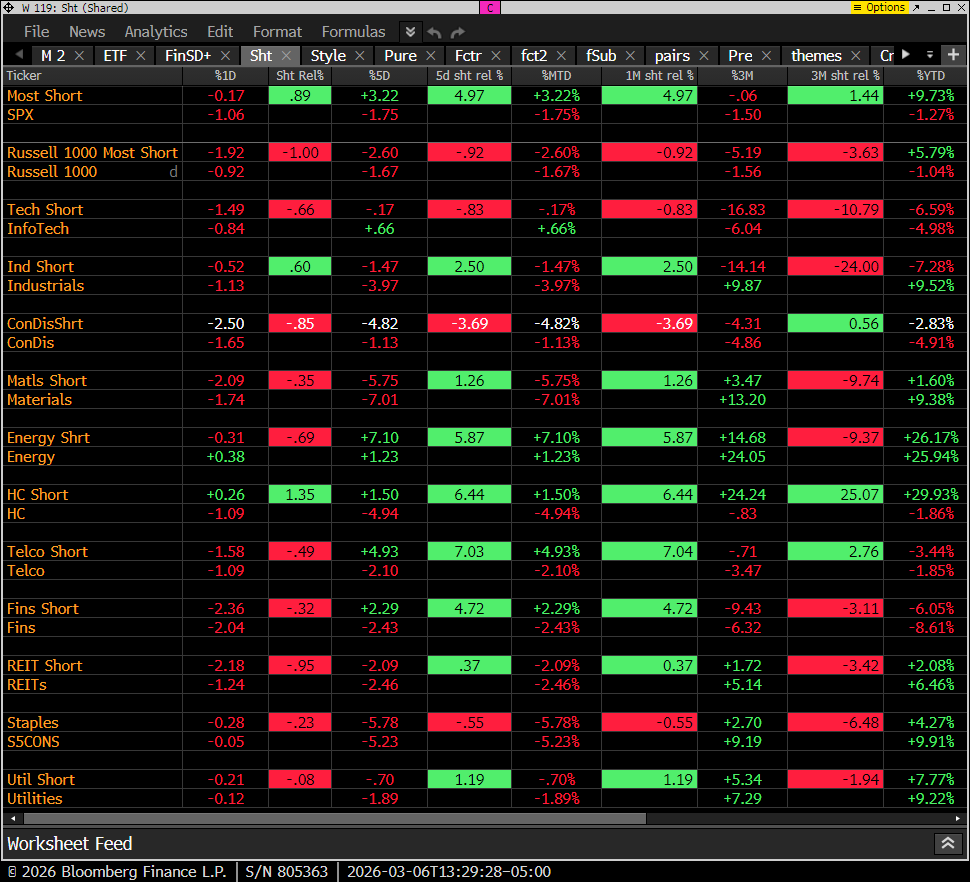

Goldman Sachs Most Shorted baskets vs. S&P Indexes

This monitor has the S&P indexes and the Goldman Sachs most shorted baskets. Most short baskets are down today. Even the most shorted energy basket is down.

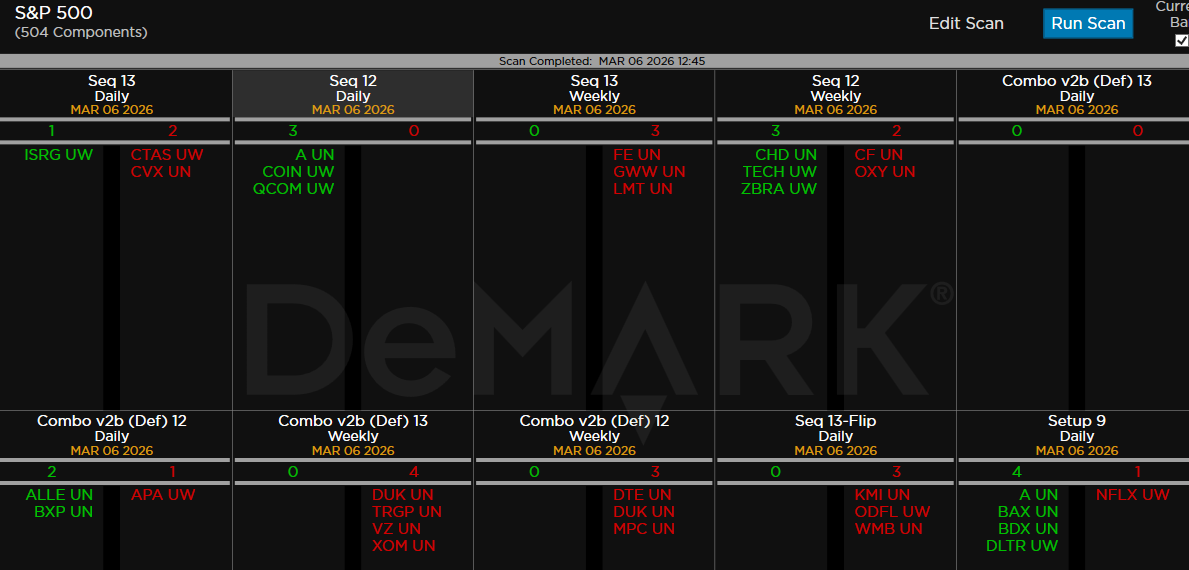

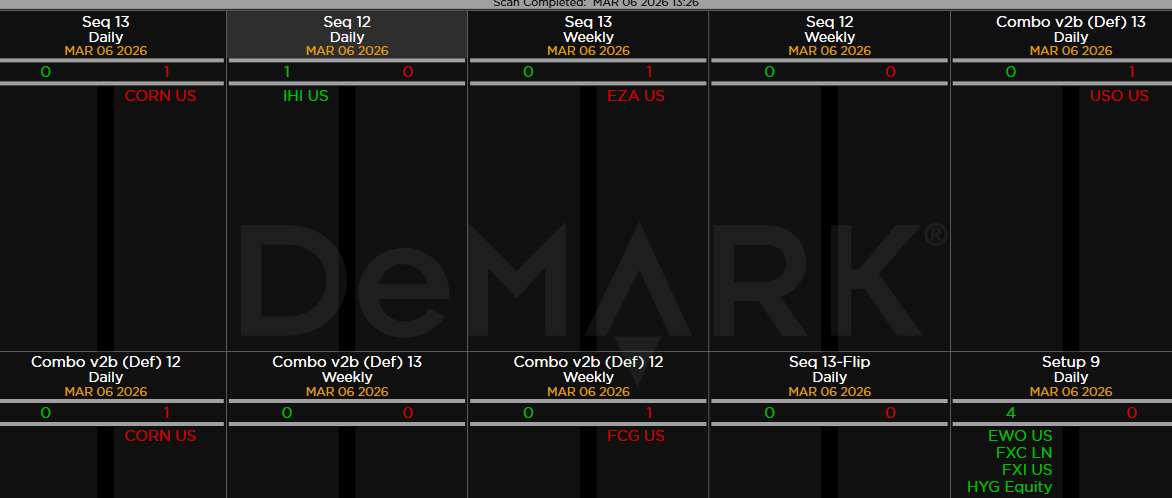

DeMark Observations

Within the S&P 500, the DeMark Sequential and Combo Countdown 13s and 12/13s on daily and weekly periods. Green = buy Setups/Countdowns, Red = sell Setups/Countdowns. Price flips are helpful to see reversals up (green) and down (red) for idea generation. The extra letters at the end of the symbols are just a Bloomberg thing. Worth noting: A little quiet with a few signals to watch.

Major ETFs among a 160+ ETF universe.

If you have any questions or comments, please email us. Data sources: Bloomberg, DeMark Analytics, Goldman Sachs, Street Account, Vital Knowledge, Daily Sentiment Index, and Erlanger Research