Today on CNBC, Berkshire Hathaway’s new CEO, Greg Abel, said, “I did not use AI to write Berkshire Hathaway’s annual letter.” Sort of comical to even mention that since Greg is replacing Warren Buffett, which is like replacing Michael Jordan. The bar is very high, but Warren Buffett and Charlie Munger left the company in a perfect position for the new CEO to take over. With $375 billion in cash and lighter on some recently overweighted positions, they have a lot of capital to deploy, which will be done in a very Warren Buffett Berkshire way.

I started learning about Warren Buffett in the early 90’s when I started in the business. Back then, he was already a legend. I have a different style and process I’ve built that works for me, yet I have a valuation bent and a few other things I look for, such as moats, clean balance sheets, and solid management. On the short side, at times that process can work in the opposite. I started reading his letters in 1999, as he seemed to miss the tech boom. It became clear why, soon enough. Back then, I bought some BRK/A in a retirement account and still haven’t sold it. Reading his annual letter has been something of a must because he’s not telling you what he’s buying, but he laid out nuggets of investment wisdom with humility. I have them all printed out in a folder, and they can also be read in an archive by year.

Now that we have AI, I thought it might be informative to use ChatGPT to summarize each year’s letter. I did, and I posted 30 takeaways below. AI is not just for memes; ChatGPT made a nice summary, and I suggest that if there is one year that gets your attention, go to the archive and read the whole letter.

Update: As I mentioned on First Call, my daughter went into labor, and I will be off the desk from time to time for the next couple of days. I’ll do my best to post notes. Thanks for all your well wishes. Our family is thrilled and excited.

Quick Market Views

Stocks: Indexes are heavy today and trading near lows as we go to print. No major levels have broken yet. Breadth is weakening with NYSE with 2575 net down issues, Nasdaq with 2100 net down issues. S&P has 119 up, 385 down issues. Every sector is down on the day except for energy up small.

Bonds: Rates are higher by 2-4 bps – higher on the short end

Commodities: Mixed with energy strong Crude up 6.4%, Natural Gas up 1.5%. Copper down 1.6%, Gold down 1.2%, Silver down 1.8%.

Currencies: US Dollar index is lifting up 0.5%. Bitcoin is down 3.5%

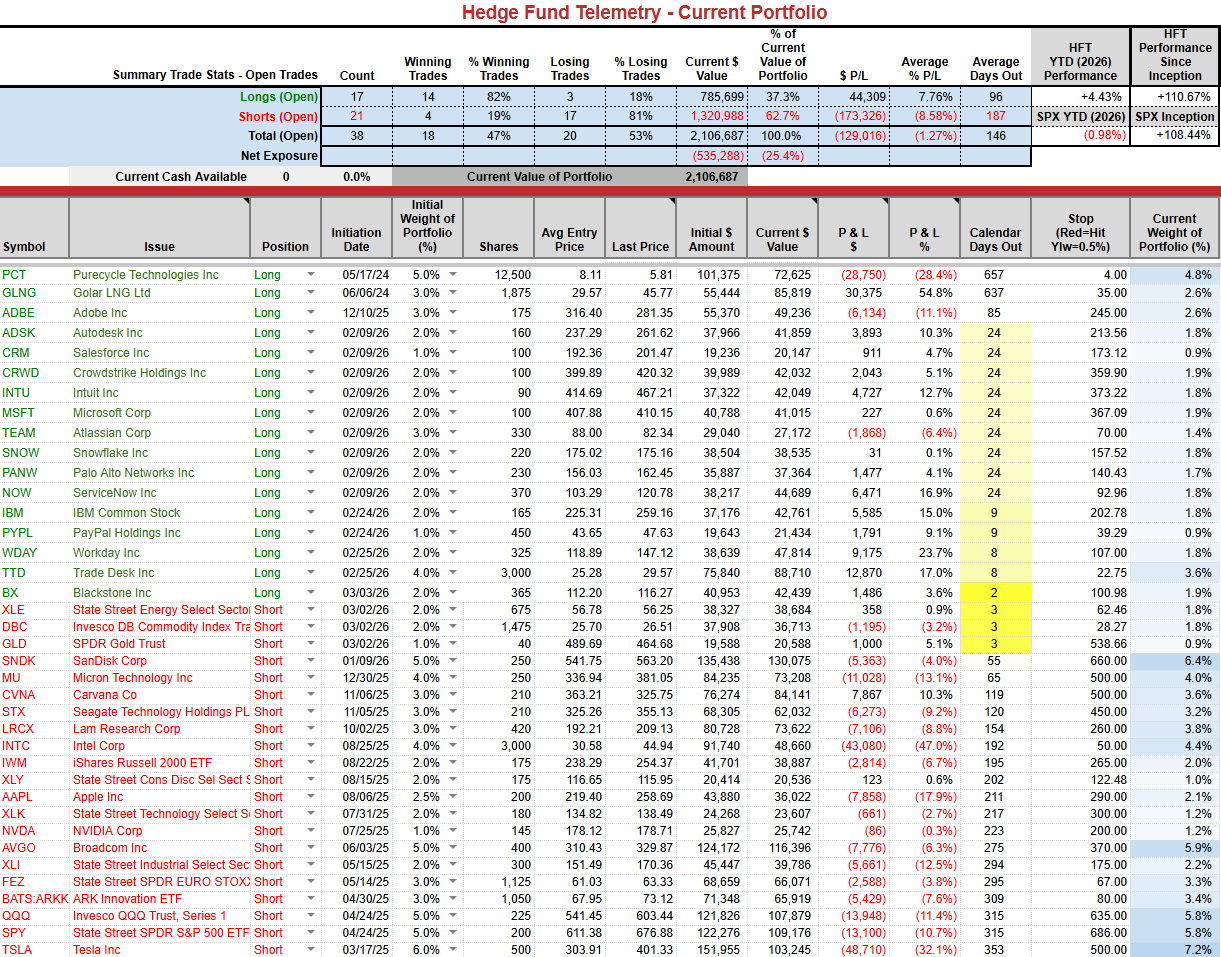

Current Portfolio Ideas: Decent PNL move this week

Changes: I will trim a few things just to have some cash with lower conviction ideas: selling MSFT up 0.6%, BX up 3.6%, PYPL up 9%

Thoughts: Continued Iran news hitting nonstop. Weak tape with software still working ok and semi’s fading. It’s all about positioning, with semis still crowded longs and software underweight. I still have the SPY and QQQ put spread expiring tomorrow. As these get into the money, take the gains when you get them. We can roll out further tomorrow.

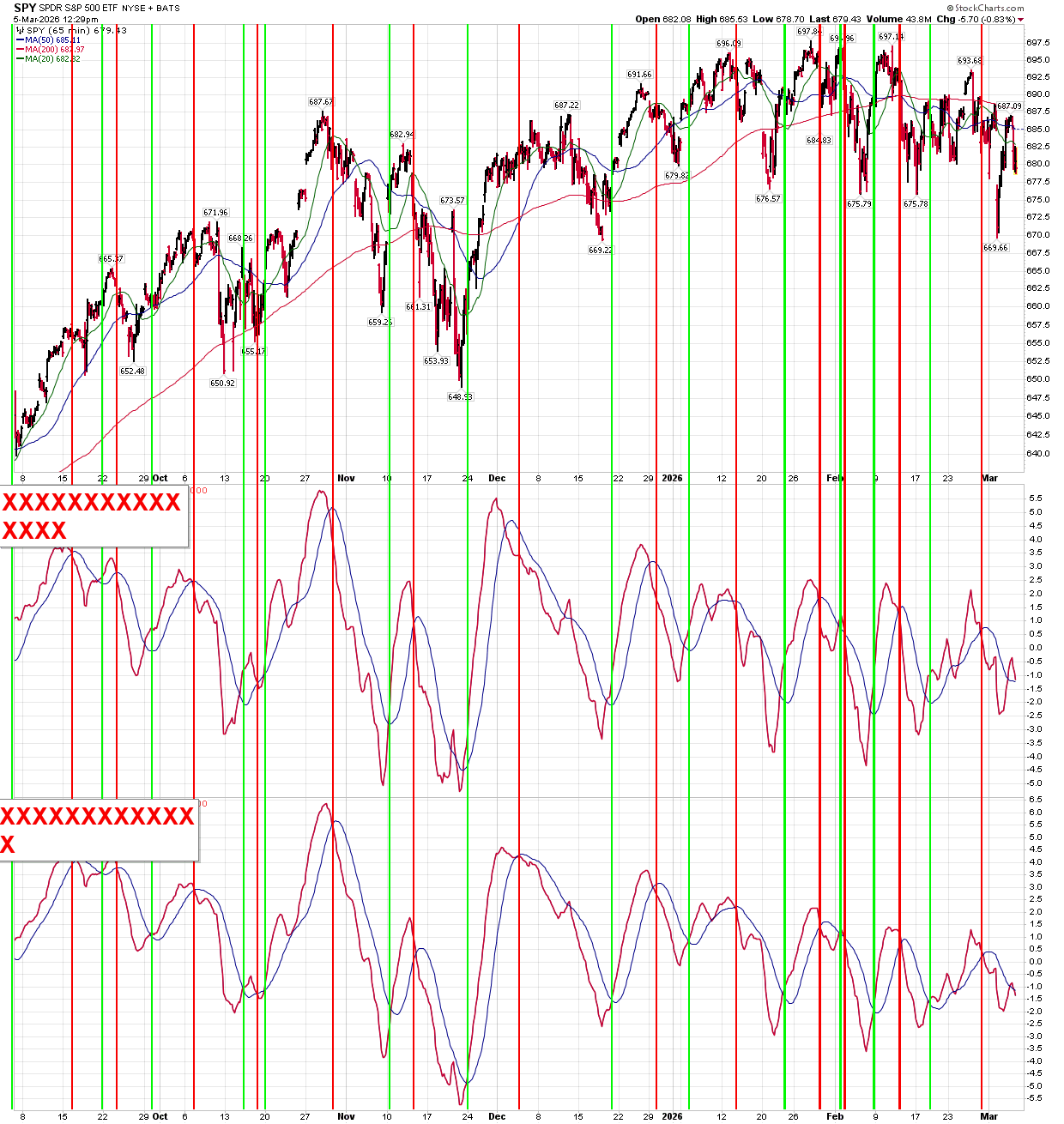

US INDEXES

S&P futures 60-minute tactical time frame choppy and giving back recent bounce. 6700 was this week’s low.

S&P 500 Index daily remains in the range from October. Slipping below first support at 6800. Major support at the TDST Setup Trend support at 6602

Nasdaq 100 Index daily reversing down with another lower high. TDST support 24,239, which remains the main support level.

Current Portfolio

Pre changes

The short term SPY and QQQ momentum has been difficult in this whippy and gappy narrow range. Should turn back to sell today. So consider these back on sell signals.

The 30 most important lessons from Buffett’s letters

I thought I’d start with this, since when going through each year, you’ll pick up more when looking below at each year’s summary.

- Intrinsic value > accounting value (think like an appraiser).

- Time is the friend of the wonderful business.

- Price matters; even great businesses can be terrible buys at extremes.

- Circle of competence beats “smart-sounding” diversification.

- Moats matter: durability of advantage is the core edge.

- Owner earnings: look through GAAP to true free cash flow.

- Maintenance capex is real—don’t ignore it.

- Avoid leverage; it turns mistakes into fatal errors.

- Volatility isn’t risk; permanent loss is.

- Temperament beats IQ; behavior drives outcomes.

- Cash is strategic optionality in crises.

- Insurance float is powerful only if underwriting is disciplined.

- Underwriting profit is the goal; growth is secondary.

- Incentives drive behavior; read compensation like a detective.

- Beware the “institutional imperative.”

- Culture is a moat (especially in decentralized systems).

- Integrity is non-negotiable; reputation compounds or collapses.

- Avoid complexity you can’t explain.

- Great managers allocate capital; they don’t just “run operations.”

- Buybacks only add value below intrinsic value.

- M&A is where CEOs overpay; demand a margin of safety.

- Forecasts are fragile; processes are durable.

- Ignore macro prediction; focus on business economics.

- Concentration is fine when you truly know what you own.

- Patience is an edge; activity is not productivity.

- Fees matter; compounding hates friction.

- Taxes matter; defer when rational, but don’t let taxes dictate stupidity.

- Align with shareholders; treat partners fairly.

- Survival first; compounding requires staying in the game.

- Bet on productive America over long horizons.

Berkshire Hathaway shareholder letters

1977–1989: Insurance float + early “moat” thinking

1977 Theme: insurance economics + capital discipline • Quote: Paraphrase: “Underwriting matters; float is only valuable if it’s not costly.” • Stock idea: best-in-class P&C insurers with consistent underwriting profit across cycles.

1978 Theme: compounding + patience • Quote: Paraphrase: “Time is the friend of a good business.” • Stock idea: high-ROIC compounders with long reinvestment runways.

1979 Theme: inflation reality • Quote: Paraphrase: “Inflation is a tax that punishes savers and weak businesses.” • Stock idea: pricing-power franchises (brands, mission-critical services).

1980 Theme: accounting vs economics • Quote: Paraphrase: “Reported earnings can mislead; focus on cash earning power.” • Stock idea: cash generative businesses with low maintenance capex.

1981 Theme: “economic goodwill” • Quote: Paraphrase: “Some businesses grow intrinsic value without needing much capital.” • Stock idea: asset-light tollbooths (payments, data, software-like models).

1982 Theme: incentives + culture • Quote: Paraphrase: “Structure incentives so managers think like owners.” • Stock idea: founder/owner-operator businesses with rational capital allocation.

1983 Theme: float as strategic asset • Quote: Paraphrase: “Float is a big deal if it’s durable and low cost.” • Stock idea: scale insurers with underwriting edge + conservative reserving.

1984 Theme: avoiding “institutional imperative” • Quote: Paraphrase: “Big companies do dumb things to look busy.” • Stock idea: avoid serial acquirers with value-destructive M&A.

1985 Theme: exit bad businesses (textiles) • Quote: Paraphrase: “A bad industry will beat a good manager.” • Stock idea: avoid structurally broken industries; prefer moats over turnarounds.

1986 Theme: intrinsic value discipline • Quote: Paraphrase: “Price is what you pay; value is what you get.” • Stock idea: discount-to-intrinsic with clear catalysts (buybacks, spin-offs).

1987 Theme: crash psychology • Quote: Paraphrase: “Volatility is not risk—permanent loss is.” • Stock idea: keep a watchlist to buy quality during panics.

1988 Theme: franchise investing (Coke era) • Quote: Paraphrase: “A great brand can be an economic fortress.” • Stock idea: global consumer brands with habit + distribution dominance.

1989 Theme: “moat” vocabulary solidifies • Quote: Paraphrase: “Durable competitive advantage is the whole game.” • Stock idea: dominant share businesses with high switching costs.

1990–1999: Owner earnings + bubble warnings + governance

1990 Theme: owner earnings • Quote: Paraphrase: “Subtract the capex required to stay competitive.” • Stock idea: free-cash-flow yield screens adjusted for true maintenance capex.

1991 Theme: integrity • Quote: Paraphrase: “Reputation is priceless; protect it.” • Stock idea: avoid governance landmines; prefer clean accounting + aligned boards.

1992 Theme: pricing power • Quote: Paraphrase: “The best businesses can raise price without losing customers.” • Stock idea: inelastic demand names.

1993 Theme: executive comp • Quote: Paraphrase: “Pay for performance—real performance.” • Stock idea: companies with ROIC-based comp (not EPS hacks).

1994 Theme: risk in complex finance • Quote: Paraphrase: “If you can’t explain it, don’t own it.” • Stock idea: avoid opaque balance sheets; prefer simple, understandable models.

1995 Theme: temperament • Quote: Paraphrase: “Investing success is behavior, not IQ.” • Stock idea: strategies that reduce bad behavior: DCA + valuation discipline.

1996 Theme: market froth forming • Quote: Paraphrase: “Expect lower returns from high starting valuations.” • Stock idea: lean to value + quality when multiples are stretched.

1997 Theme: scale challenges • Quote: Paraphrase: “Bigger capital makes high returns harder.” • Stock idea: prefer mid-cap compounders over mega-caps when valuation is equal.

1998 Theme: long-term ownership • Quote: Paraphrase: “Our favorite holding period is forever.” • Stock idea: buy-and-hold compounders with durable unit economics.

1999 Theme: dot-com mania warning • Quote: Paraphrase: “Speculation is most dangerous when it looks easiest.” • Stock idea: avoid “story stocks”; focus on cash + moats.

2000–2009: aftermath + derivatives warning + crisis playbook

2000 Theme: bubble hangover • Quote: Paraphrase: “Business value didn’t change—prices did.” • Stock idea: buy quality franchises after multiple compression.

2001 Theme: transparency • Quote: Paraphrase: “If we can’t explain it clearly, we won’t do it.” • Stock idea: companies with simple disclosures and conservative accounting.

2002 Theme: derivatives risk • Quote: Direct: “Derivatives are financial weapons of mass destruction…” • Stock idea: avoid leveraged financials; prefer strongly-capitalized insurers/banks.

2003 Theme: insurance cycle discipline • Quote: Paraphrase: “Walk away from dumb pricing.” • Stock idea: insurers that shrink when pricing is irrational.

2004 Theme: governance & disclosure • Quote: Paraphrase: “Bad accounting is a silent partner.” • Stock idea: short-list companies with high-quality earnings.

2005 Theme: expected return realism • Quote: Paraphrase: “Future returns are a function of starting price.” • Stock idea: tilt toward reasonable multiples + buybacks.

2006 Theme: philanthropy + stewardship • Quote: Paraphrase: “We’re caretakers of capital, not entertainers.” • Stock idea: capital allocator CEOs with rational repurchase frameworks.

2007 Theme: leverage concerns • Quote: Paraphrase: “Easy credit plants the seeds of pain.” • Stock idea: avoid high-debt cyclicals late-cycle.

2008 Theme: crisis opportunity • Quote: Paraphrase: “When liquidity vanishes, prepared buyers win.” • Stock idea: keep dry powder for forced sellers situations.

2009 Theme: big deals + America bet • Quote: Paraphrase: “Pessimism is an asset for the buyer.” • Stock idea: post-crisis best-of-breed financials/industrials at distressed valuations.

2010–2019: Berkshire as a giant + buybacks + Apple era

2010 Theme: “real economy” ownership • Quote: Paraphrase: “Own productive assets, not predictions.” • Stock idea: infrastructure + transport businesses with durable demand.

2011 Theme: buybacks discipline • Quote: Paraphrase: “Repurchases only make sense below intrinsic value.” • Stock idea: net cash companies with disciplined repurchase triggers.

2012 Theme: succession + durability • Quote: Paraphrase: “Build systems that work without the hero.” • Stock idea: businesses with deep benches + decentralized ops.

2013 Theme: compounding retrospect • Quote: Paraphrase: “Time + reinvestment beats brilliance.” • Stock idea: repeatable reinvestment models.

2014 Theme: culture as moat • Quote: Paraphrase: “Culture compounds.” • Stock idea: firms with low bureaucracy + high trust.

2015 Theme: overpaying risk (mega deals) • Quote: Paraphrase: “Big acquisitions demand extra humility.” • Stock idea: avoid empire-building; prefer bolt-ons + buybacks.

2016 Theme: equity portfolio as business ownership • Quote: Paraphrase: “Stocks are pieces of businesses.” • Stock idea: business-analyst stock picking, not chart picking.

2017 Theme: concentration into best idea • Quote: Paraphrase: “Diversification is protection against ignorance.” • Stock idea: concentrated quality + valuation bets (within risk limits).

2018 Theme: patience + cash optionality • Quote: Paraphrase: “Cash is a call option on chaos.” • Stock idea: maintain liquidity to exploit dislocations.

2019 Theme: size + opportunity set • Quote: Paraphrase: “The easiest billions are gone; discipline remains.” • Stock idea: look for mid-cap “Berkshire-like” compounders.

2020–2024: pandemic, inflation, maturity, and legacy

2020 Theme: uncertainty + mistakes • Quote: Paraphrase: “We’ll be wrong sometimes—survive to compound.” • Stock idea: fortress balance sheets; avoid fragile leverage.

2021 Theme: America bet • Quote: Direct: “Never bet against America.” • Stock idea: own broad productivity winners (industrial automation, logistics, payments).

2022 Theme: inflation + rates • Quote: Paraphrase: “Inflation changes the hurdle rate; stay rational.” • Stock idea: pricing power + low capital intensity.

2023 Theme: partnership + temperament • Quote: Paraphrase: “Rationality is a competitive advantage.” • Stock idea: avoid hype cycles; buy mispriced quality.

2024 Theme: stewardship + endgame simplicity • Quote: Paraphrase: “Good processes beat good forecasts.” • Stock idea: “boring winners”: regulated utilities, insurers, staples, selectively at value.

s&P 500 heat map

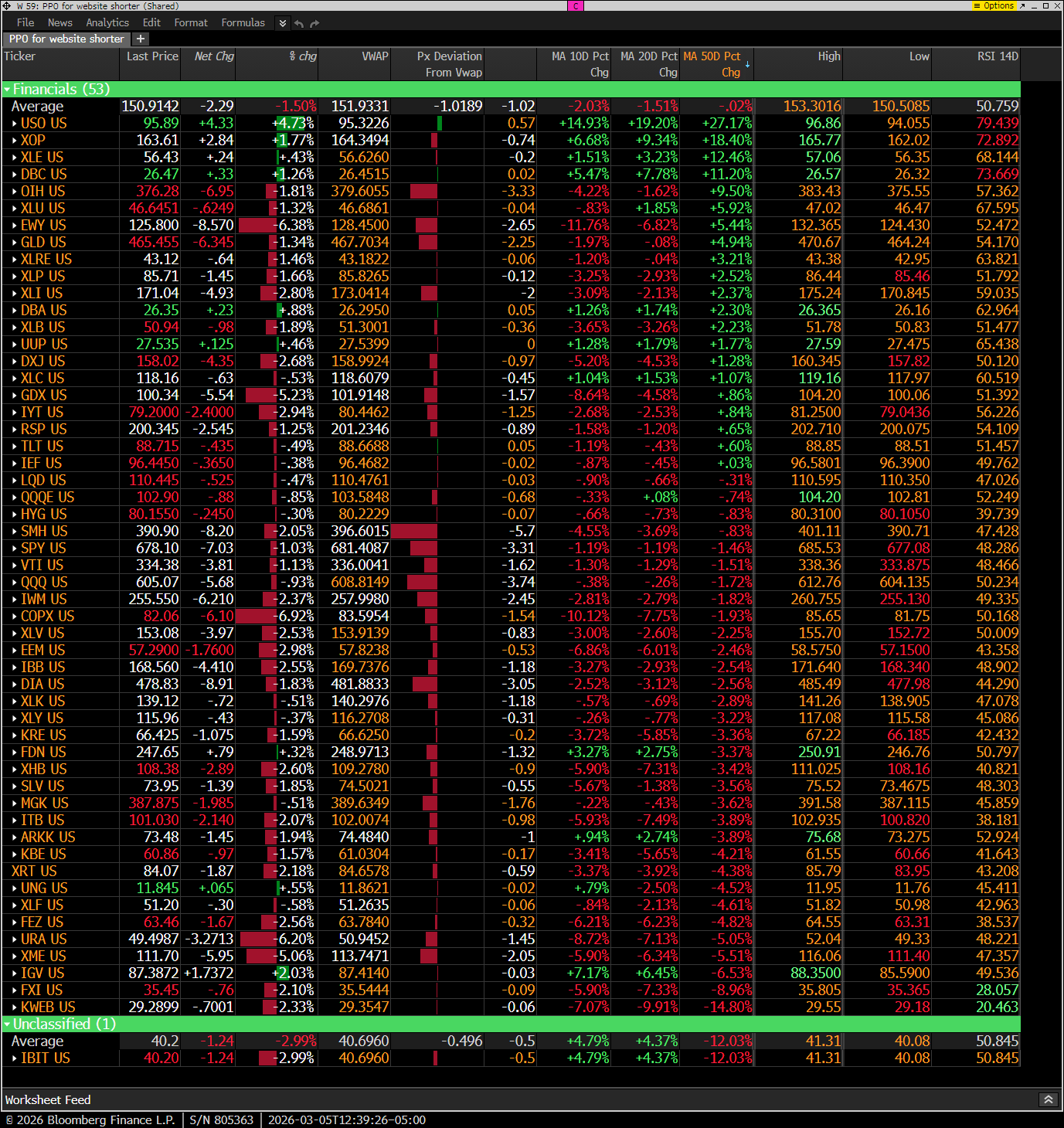

Hedge Fund Telemetry ETF Percentage Price Oscillator Monitor

The PPO monitor (percentage price oscillator) force ranks ETFs by percentage above/below the 50-day moving average. This monitor and others are offered to Hedge Fund Telemetry subscribers on Bloomberg. Heavy action today. IGV is now above the 10 and 20 day moving averages and off the bottom of the monitor.

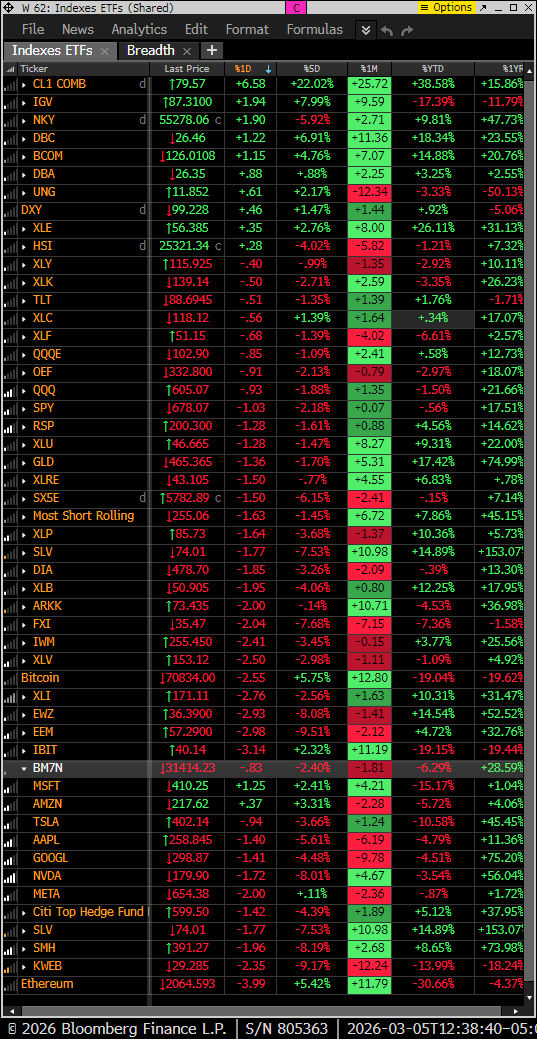

Index ETF and select factor performance

ETF with today’s performance with 5-day, 1-month, and 1-year rolling performance YTD. Crude and software leading

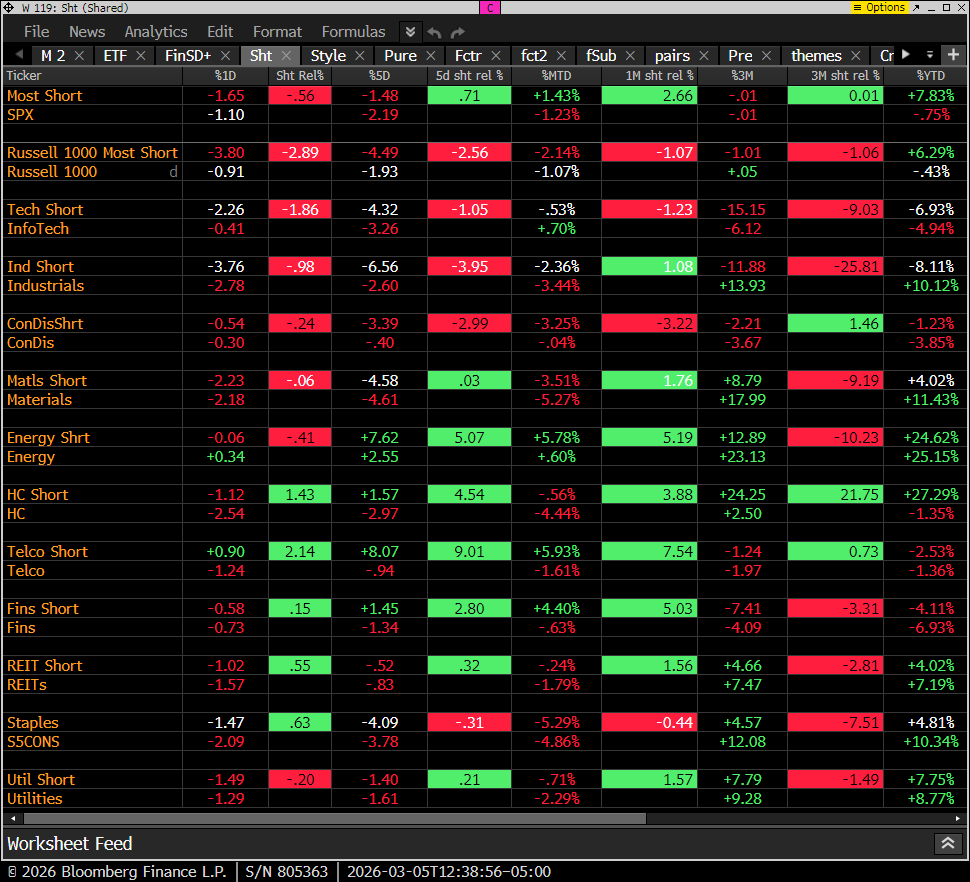

Goldman Sachs Most Shorted baskets vs. S&P Indexes

This monitor has the S&P indexes and the Goldman Sachs most shorted baskets. Short baskets are mostly down. Every sector down ex energy up small.

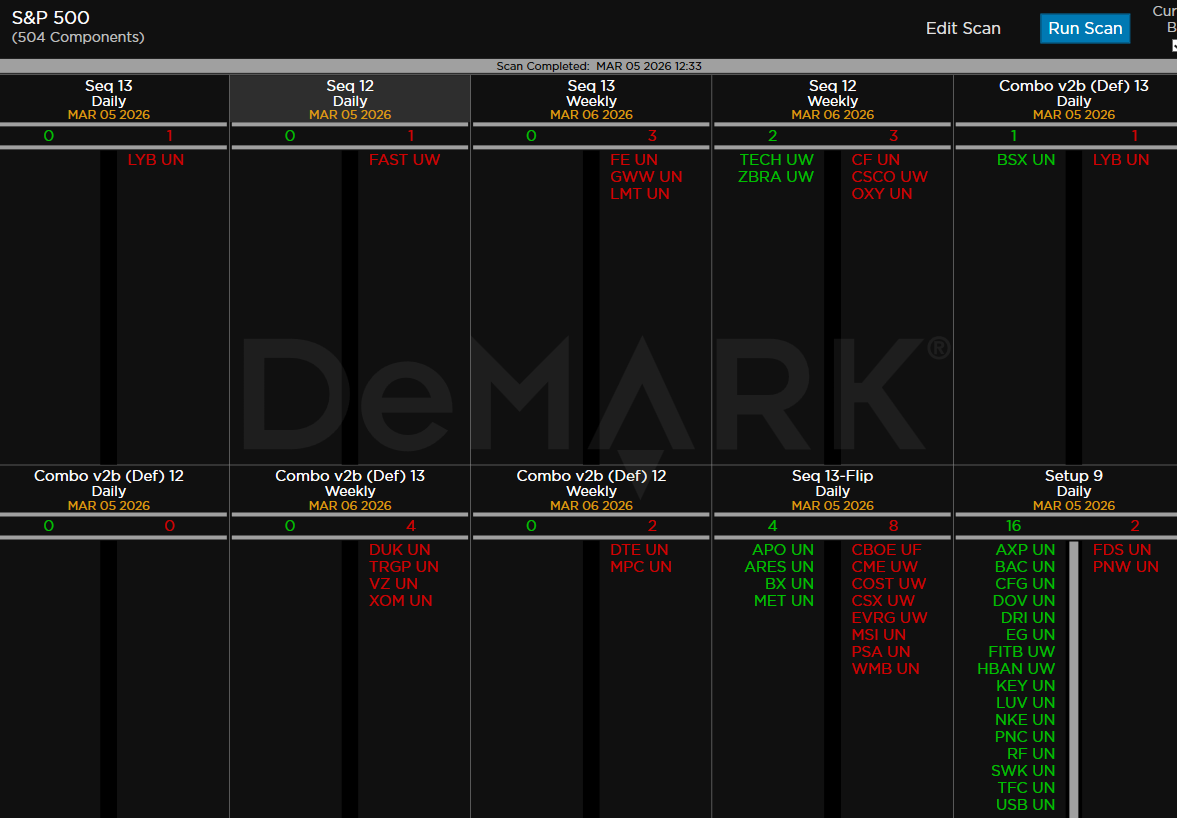

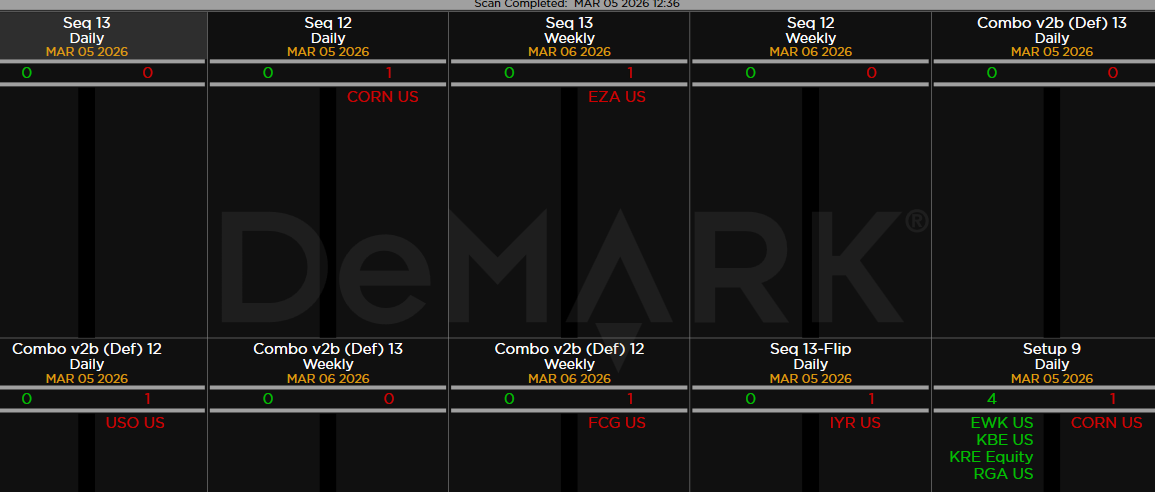

DeMark Observations

Within the S&P 500, the DeMark Sequential and Combo Countdown 13s and 12/13s on daily and weekly periods. Green = buy Setups/Countdowns, Red = sell Setups/Countdowns. Price flips are helpful to see reversals up (green) and down (red) for idea generation. The extra letters at the end of the symbols are just a Bloomberg thing. Worth noting: A few to watch on the price flip up and down columns. Quiet with the 13’s as expected with range bound trading.

Major ETFs among a 160+ ETF universe.

If you have any questions or comments, please email us. Data sources: Bloomberg, DeMark Analytics, Goldman Sachs, Street Account, Vital Knowledge, Daily Sentiment Index, and Erlanger Research