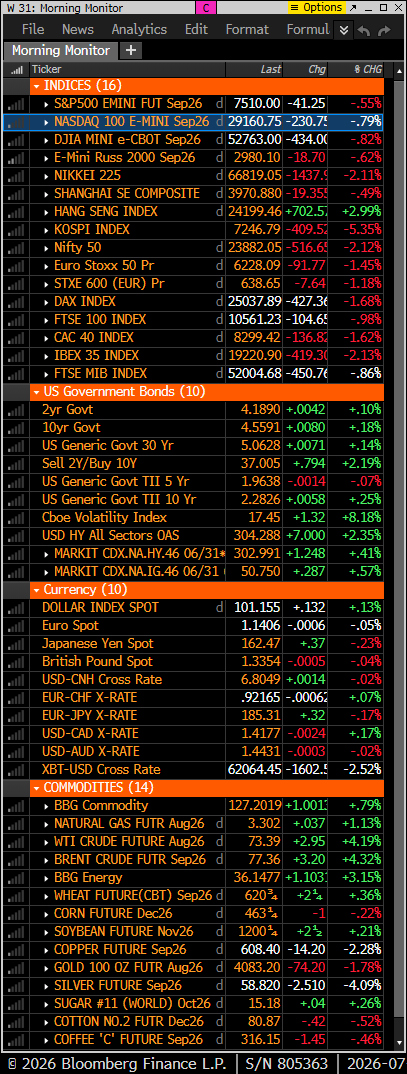

Premarket Price Action

US equity futures: S&P -0.6%, Nasdaq -0.75%, Russell 2000 -0.65% – off lows

Treasuries: rates +1–2 bp

Dollar: DXY +0.1%

Crypto: Bitcoin -3.0%

Commodities: Gold -1.5%, Silver -3.6%, Crude +4.1%, Natural Gas +1.3%

Here is the July Big Picture note. Last month, we posted an interim note on US AI risks, and this edition highlights some Chinese AI and EV potential big-upside ideas that are early in a rebound. If you subscribed to the Big Picture and have any issue accessing the note, please let us know. If you would like the note added to your current subscription, we can add it for you; just let us know if you want one of the two-year plans.

Overnight – Global Markets

Asia: Mixed but ugly under the surface. Korea -5.4% with SK Hynix and Samsung hit again. Japan -2.1%. Hong Kong was the standout, with Alibaba/Baidu strength offsetting broader regional pressure.

Europe: Broadly lower, down ~175–200 bp. Energy is the only clear outperformer as oil spikes; autos, industrials, banks, retail and software lag.

Premarket Setup and What’s Driving Markets

Risk is under pressure from the wrong mix: oil higher, yields higher, dollar firm and AI leadership still unwinding. Trump saying the Iran ceasefire is “over” put geopolitics back in the driver’s seat, while semis/memory remain heavy after Samsung failed to satisfy elevated expectations.

- Brent spike is pressuring futures and keeping rates from rallying.

- AI pick-and-shovel unwind continues, with South Korean memory still the pressure point.

- The market is rotating, but today’s oil/rates shock is a direct headwind to the broadening-out trade.

- FOMC minutes are today’s macro event, with focus on Warsh’s communication shift and hawkish dots.

- 10-year auction supply adds another test for rates.

Macro & Policy Focus

May wholesale inventories are due this morning. Treasury sells $39B of 10-year notes. June FOMC minutes at 14:00 ET are the main event, especially given Warsh’s early push toward less forward guidance and a more uncertain reaction function.

Initial claims, existing home sales and a 30-year auction follow tomorrow. Williams and Logan also speak Thursday.

Company, Sector Movers, Earnings Summary

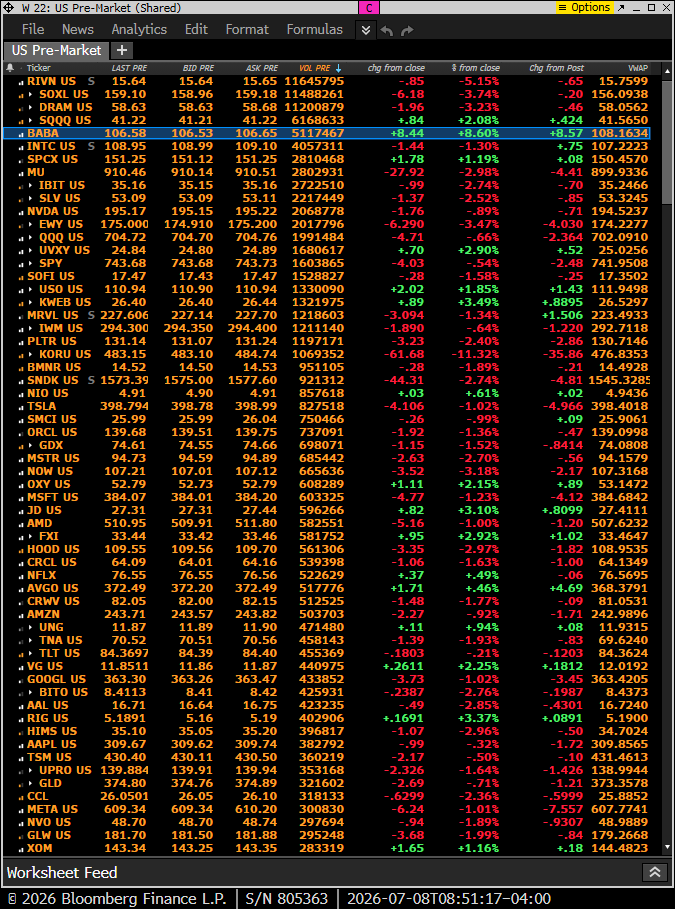

- AAPL: Testing CXMT memory chips for China-sold devices. Something I said would happen.

- SK Hynix: ADR listing reportedly multiple times oversubscribed.

- BABA: Strong in Hong Kong, reinforcing rotation into China internet while Korea memory sells off.

- We remain very bullish China/Hong Kong with various names

- OpenAI: Cleared to launch GPT-5.6 after prior White House restrictions lifted.

- MSFT: Reportedly replacing some OpenAI/Anthropic models with proprietary MAI models to cut costs.

- FISV: President resigns; payments complex also in focus after bank consortium reports.

- KRUS: Comps missed; traffic weak.

- XOM: Preliminary Q2 implies a large sequential profit increase. – we remain long XOM and CVX

- PENG: Strong AI-driven upside and raised guide.

Key S&P 500 Upgrades / Downgrades

Upgrades

- DLTR: Raised to Neutral at Goldman; PT $125

- ODFL: Raised to Overweight at Wells Fargo; PT $250

- OXY: Raised to Outperform at Evercore ISI; PT $65

Downgrades

- CINF: Cut to Market Perform at KBW; PT $201

- HCA: Cut to Equal-Weight at Barclays; PT $427

- TRV: Cut to Market Perform at KBW; PT $356

- UDR: Cut to Hold at Truist

- UHS: Cut to Equal-Weight at Barclays; PT $179

Initiations

- MA/V: New Overweight at Barclays

- PYPL: New Underweight at Barclays

- XYZ: New Overweight at Barclays

- FIS/FISV/GPN: New Equal-Weight at Barclays

- RCL: New Outperform at BMO

- CCL/NCLH: New Market Perform at BMO

- WYNN: New Buy at Truist; PT $125

- T: New Underweight at Wells Fargo; PT $18

What We’re Watching Today and bottom line

- Crude reaction to the Iran ceasefire breakdown.

- Whether Nasdaq selling spreads beyond semis/memory.

- 10-year auction demand.

- FOMC minutes and any clues on Warsh’s communication regime.

- Rotation into China internet vs. continued Korea memory weakness.

- The tape has shifted from AI leadership stress to a broader macro stress test as oil and yields move higher together. The market can absorb a contained semi unwind, but not if crude, rates and the dollar all rise at the same time. Risk/reward is less clean until oil stabilizes and Nasdaq leadership stops leaking.

market snapshot

economic reports today

premarket trading

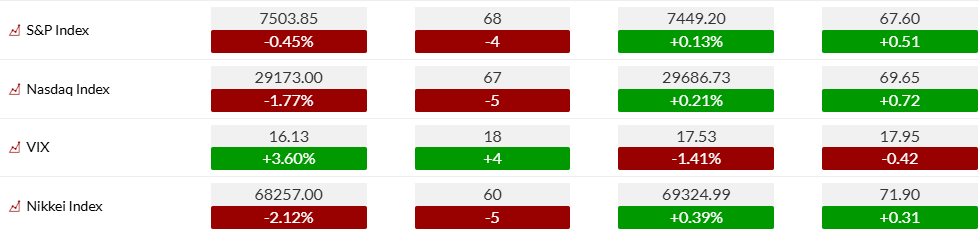

US MARKET SENTIMENT

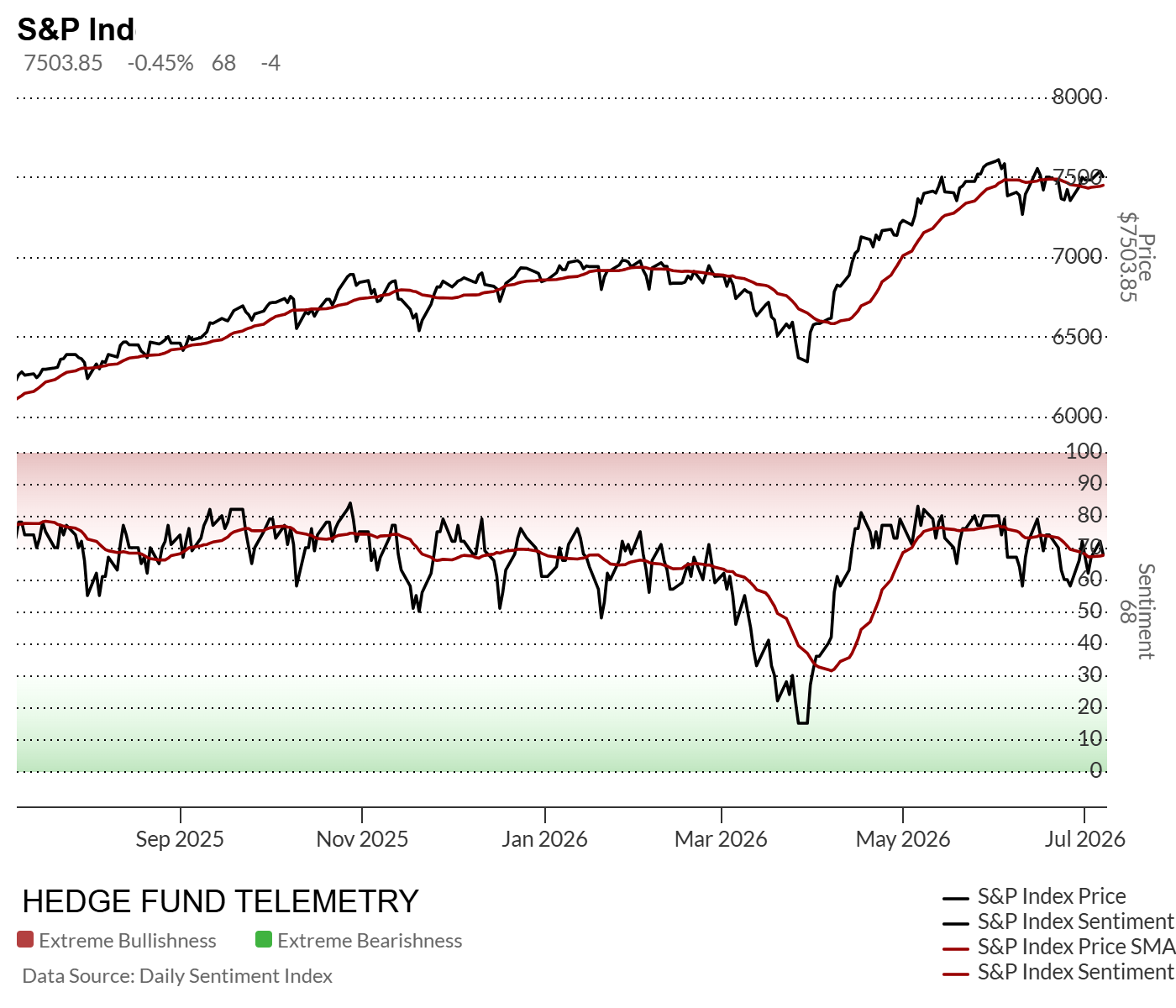

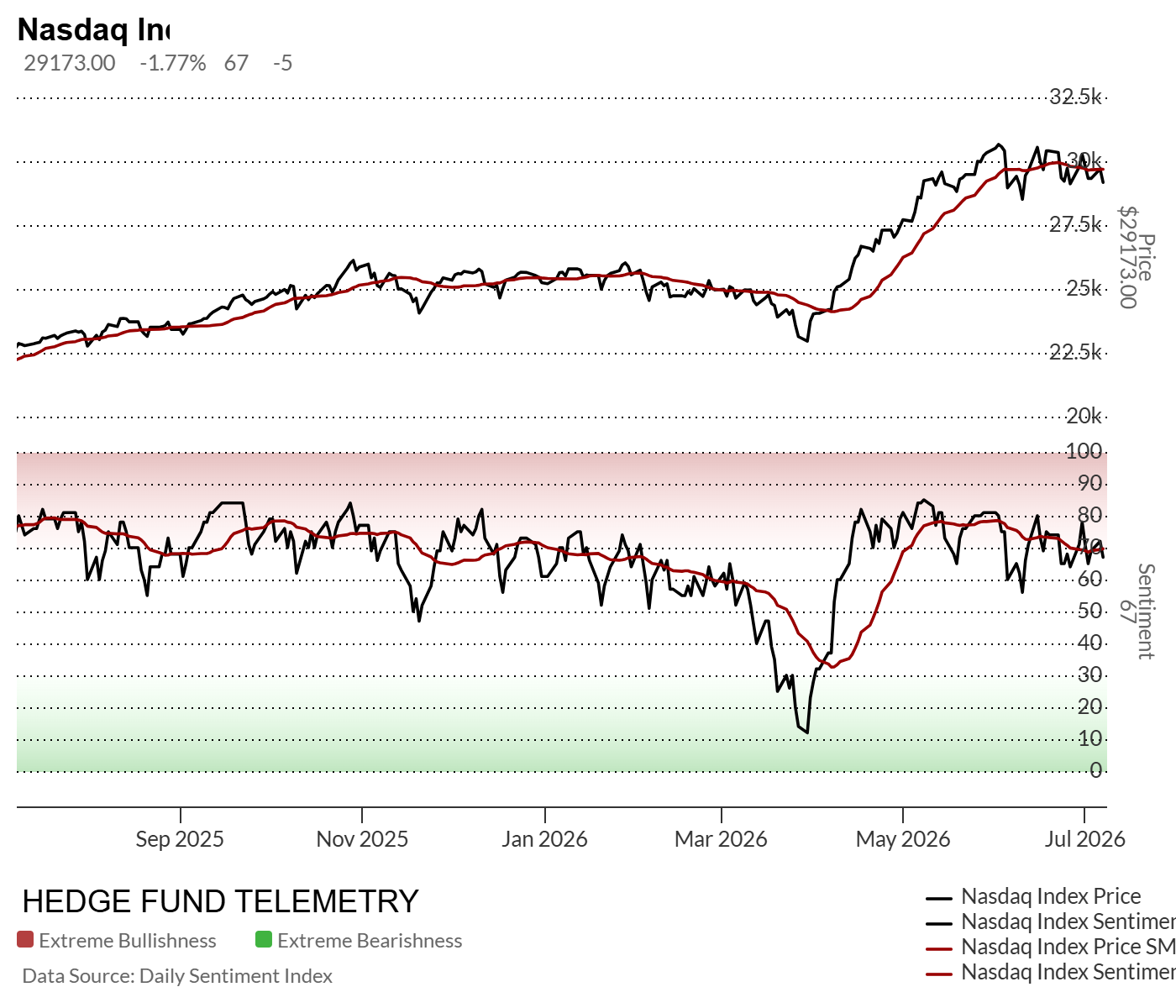

S&P bullish sentiment is 68%, down 4 points. Nasdaq sentiment is 67%, down 5 points. VIX sentiment is 18%, up 4 points but still in an extreme low-volatility/complacency zone.

Equity sentiment remains above the 50% pivot, but the direction is deteriorating. The Nasdaq move is the more important signal given the pressure in semis/memory and AI infrastructure. This is not yet broad capitulation; it is leadership stress.

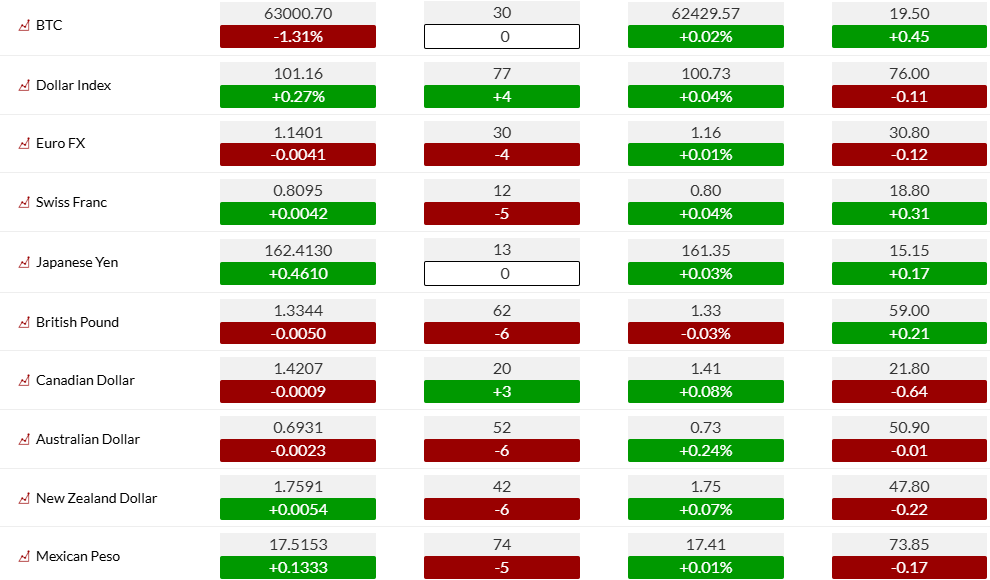

Rates: 10-year Treasury sentiment fell to 40%, down 7 points, and 30-year sentiment fell to 35%, down 7. Rates sentiment is shifting lower as yields rise, and the market is losing the benefit of duration support into the oil spike.

FX: Dollar sentiment is elevated at 77%. Euro sentiment is weak at 30%. Swiss franc sentiment is very low at 12% and yen sentiment remains depressed at 13%. FX still reflects dollar dominance and crowded weakness in funding currencies.

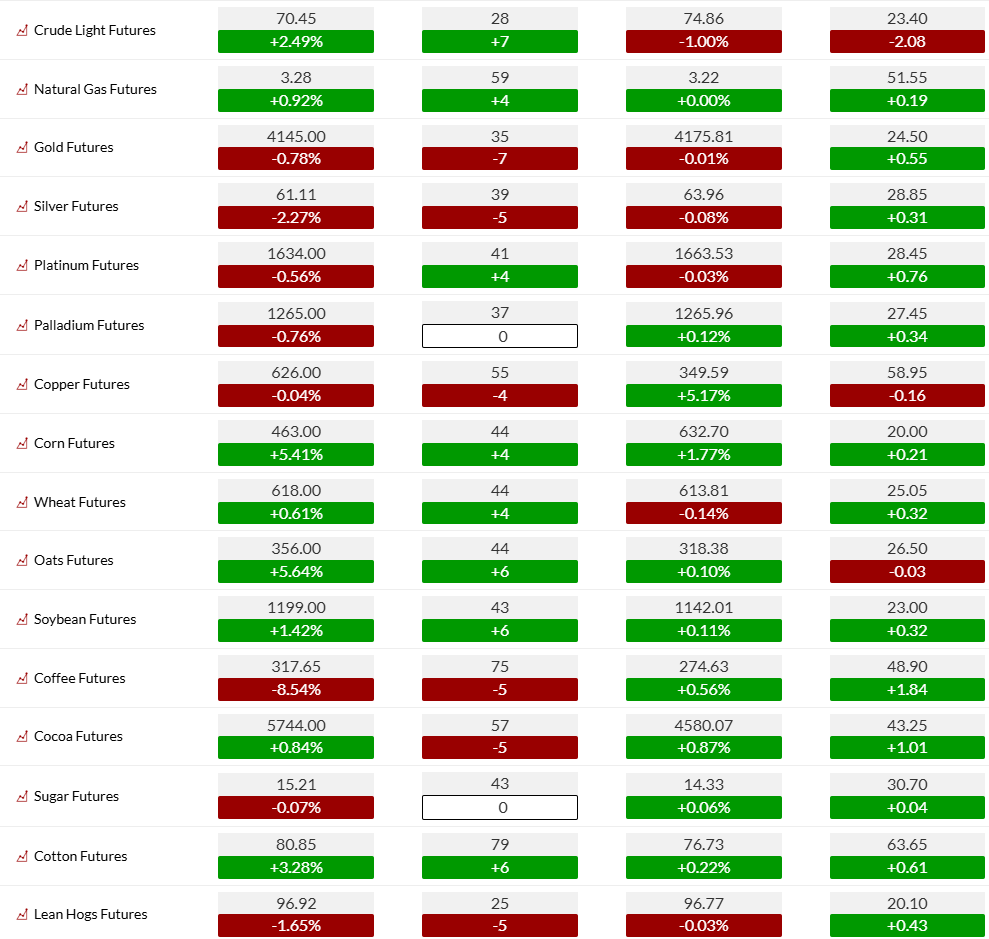

Commodities: Crude sentiment rose to 28%, up 7, but remains low despite the sharp oil move. Natural gas sentiment is 59%. Gold sentiment fell to 35%, silver to 39%. Cotton is near an extreme at 79%, while coffee remains elevated at 75%.

US MARKETS

S&P futures 240-minute tactical time frame has TDST Setup Trend resistance and support levels to watch. Recent Sequential sell Countdown 13. The downside TDST support at 7368 is essential for the bulls to hold.

S&P futures daily has a lower high wave 2 of 5 pattern after recent Sequential and Combo sell Countdown 13’s. A new high would cancel the downside wave pattern and revert back to wave 5 of 5. Momentum has been weak

Nasdaq 100 240-minute tactical time frame broke the TDST support with new buy Setup 9. In range-bound markets, the Setup 9s can signal inflection points. Continuation lower will see a new Sequential Countdown begin.

Nasdaq 100 futures daily is below the TDST support – it has turned red from dotted green signifying qualifying. The pending Sequential could cancel today with this break.

Extra charts we’re watching

Gold futures today qualified the pending DeMark Sequential buy Countdown 13. Still having trouble clearing the 20-day.

US Dollar Index daily holding the upslopping 20 day moving average

US 10-Year Yield still moving higher

Bitcoin Daily now has qualified corrective lower high wave 4 of 5 and there is a new downside wave 5 price objective of 53,790

I showed the Bitcoin 240 minute chart with the recent Sequential sell Countdown 13. And price has dropped but still is above the low from a few days ago.

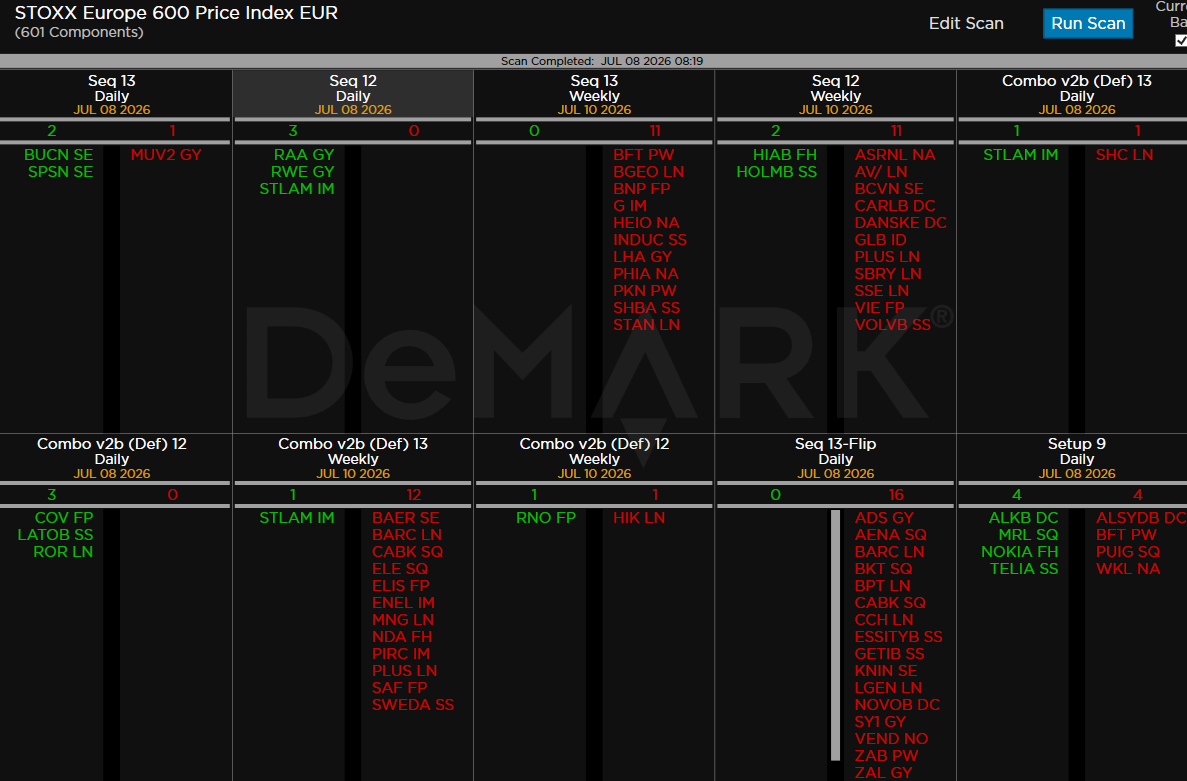

DeMark Observations – Euro Stoxx 600

Keep an eye on the large number of price flips on the downside – good place to find short ideas