- S&P futures up 0.3% and Nasdaq futures up 0.5% in Monday morning trading. Comes after US equities finished mostly lower last week with small-caps, rate-sensitive plays, industrial metals, machinery, healthcare and banks among the laggards. Big tech largely outperformed with GOOGL the standout though NVDA came under pressure. Treasuries firmer after a big backup in yields last week. Dollar index little changed, mixed on the major crosses. Gold up 0.15%. Bitcoin down 0.6%. WTI crude off 1%.

- Market waiting for FOMC on Wednesday. Fed widely expected to cut rates by another 25 bps, though also expected to guide for a slower pace of easing going forward. Market narrative largely unchanged with seasonality and soft-landing traction the widely discussed bright spots, though some scrutiny surrounding breadth deterioration and upward pressure on yields. A few developments in focus over the weekend. Lot of discussion about CEOs flocking to Trump, though unable to get him to back off tariff plans. Tariff concerns already leading to stockpiling and may be driving inflation higher. China November activity data underwhelmed with retail sales unexpectedly slowing. South Korea impeached President Yoon Suk Yeol. Moody’s downgraded France.

- Empire manufacturing (weaker) and flash manufacturing and services PMIs out this morning.

- AAPL reportedly planning major design and format changes, including thinner, foldable iPhones that will be cheaper than Pro models. HON said exploring strategic alternatives, including potential separation of aerospace business. MSTR, PLTR and AXON up on news that they will join the Nasdaq 100. SMCI down on news that it has retained Evercore to help company raise capital. POST reportedly exploring a combination with LW. BHLB and BRKL reported to be in merger talks and deal could be announced as soon as this week. CPRI reportedly looking to sell its Jimmy Choo and Versace brands. LEN, MU, FDX, NKE, ACN and CCL the high-profile earnings reports out this week.

- Key Upgrades/Downgrades: Peabody Energy upgraded to outperform from market perform at BMO Capital Markets. Microchip Technology downgraded to underperform from neutral at BofA. Macy’s upgraded to buy from hold at Gordon Haskett. Netflix downgraded to hold from buy at Loop Capital Markets. Mizuho Securities USA upgrades COP, CRK, EQT; downgrades CNX, NOG, PARR, and PBF. ConocoPhillips resumed overweight at Morgan Stanley. Hovnanian Enterprises initiated neutral at Wedbush Securities.

- Currency and Commodity weekly notes – unlocked.

market snapshot

economic reports today

premarket trading

US MARKET SENTIMENT

S&P and Nasdaq bullish sentiment is mixed with stronger Nasdaq vs S&P

Bond bullish sentiment fell again on Friday and is oversold again

Currency bullish sentiment highlighted with US Dollar sentiment remaining at 85% – extreme.

Commodity bullish sentiment saw deep declines with metals on Friday

US MARKETS

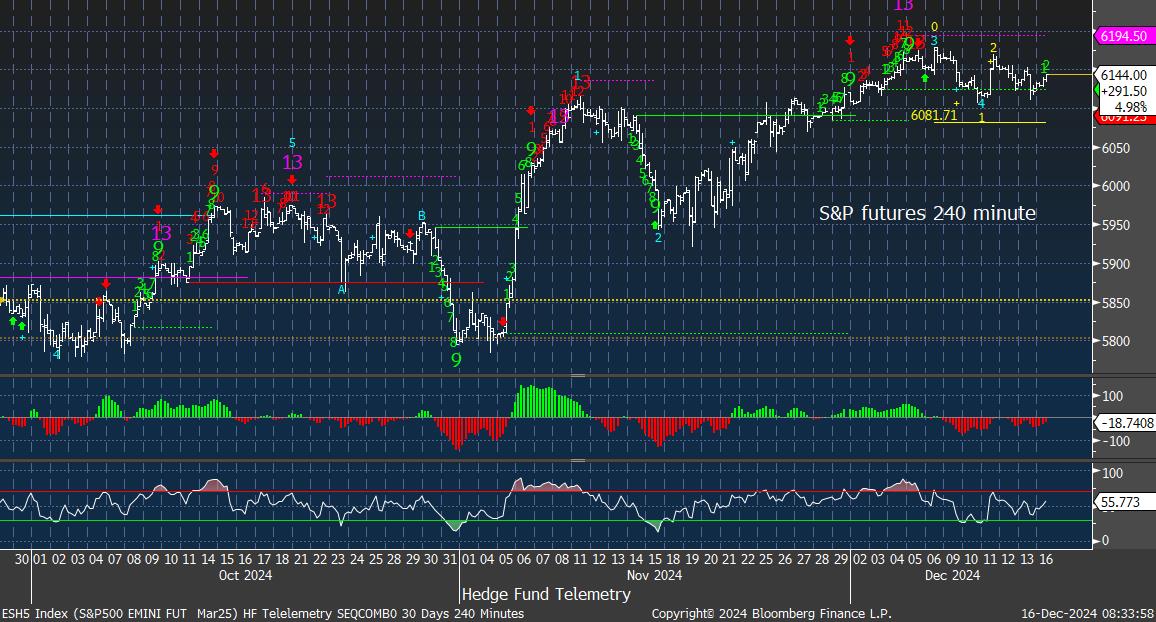

S&P futures 60 and 240-minute tactical time frames have been making lower highs after some DeMark sell Countdown 13’s. 6100 is first support on futures (not cash)

S&P futures daily has moderated while still holding the 20 day at 6100

Nasdaq 100 60 and 240-minute tactical time frames with DeMark Sequential sell Countdown 13’s in play.

Nasdaq 100 futures daily absent any DeMark signals but at the automated upside wave 5 of 5 price objective

Extra charts we’re watching

US Dollar Index daily with Sequential pending on day 8 of 13. Breakout potential not far from this level.

US 10-Year Yield stalling after a string of upside with yields. Breakout at 4.48% remains the risk.

Bitcoin Daily now on day 12 of 13 with the DeMark Sequential. To complete a Countdown bar thirteen must be greater/less than or equal to the close of the 8th bar and the normal pattern of the thirteenth bar must be greater/less than or equal to the high/low of two earlier bars.

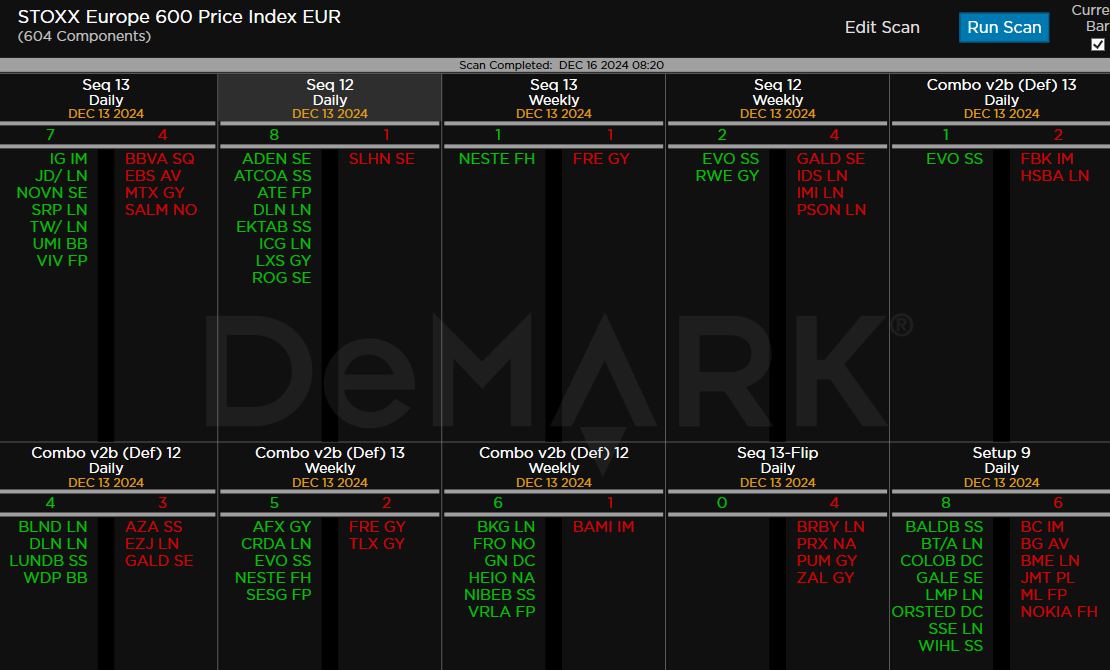

DeMark Observations – Euro Stoxx 600