TOP EVENTS AND CATALYSTS

It should be a quiet week with economic data and corporate news. We’ll watch China’s NBS PMIs for December on Monday night and the US manufacturing ISM for December on Friday. In addition, the House Speaker vote scheduled for 1/3 will be watched closely after the recent stopgap saga. Tesla will publish its Q4 delivery numbers on the 2nd or 3rd. Expectations are for a slight YoY decline for deliveries. One factor that could lead to an upside is the threat of Trump eliminating the $7500 tax credit, causing a pull forward in short-term demand. The bulls will probably be OK with no growth despite Tesla trading at an absurd P/E of ~160x. It’s not like they care about fundamentals.

Weekend News

- After Another Bad Year for Bonds, Investors Lose Faith in a Turnaround WSJ

- US energy production won’t rise rapidly in the coming years despite what Trump desires, for two big reasons: shale fields are aging (and thus a lot less productive than before) and they’re now mostly controlled by large oil companies (which are extremely disciplined on spending and output) WSJ

- TikTok – Trump in a legal filing Friday night asked the Supreme Court to delay the Jan 19 TikTok sell-or-ban deadline to give his incoming administration time to consider the matter Washington Post

- Rekor has caught the attention of the meme crowd on Reddit.

Here is the replay link for our Market Update webinar from Friday. Here are unlocked Currency and Commodity weekly notes. (This is the last weekend with unlocked notes) These are cheap for what you get at a discounted rate of just $250 for current Hedge Fund Telemetry Subscribers. We see these notes as rounding out the macro picture our subscribers have said they like, as they can quickly decipher the trends and get a few ideas too. If you want to add these notes, email us, and we’ll add them to your subscription.

Charts we are watching

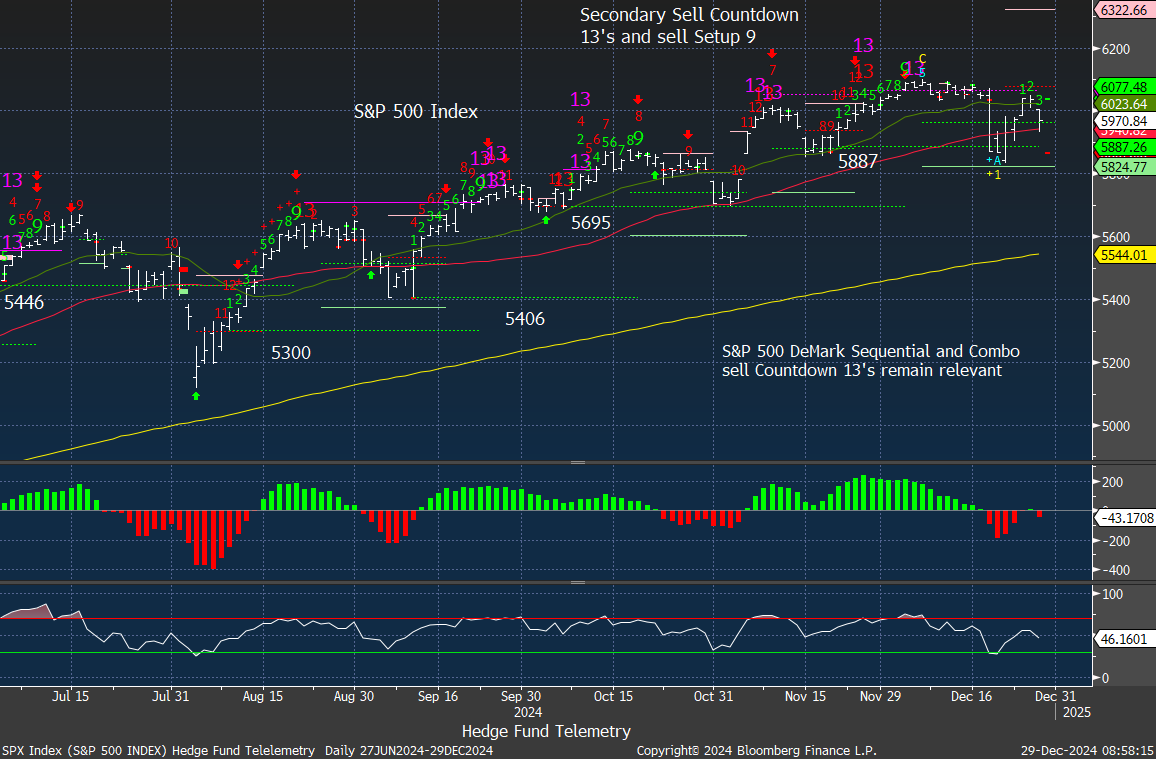

S&P 500 Index shows the drop with the Fed and bounce nearly back but failing to hold with a decent sized drop on Friday holding the 50 day. A break of the 5887 TDST Setup Trend support would be a negative. A move to the 200 day would probably be a healthy sized correction at 5544. Roll out the Markets in Turmoil CNBC special!

S&P 493 ex Mag 7 has been under pressure with a downside Sequential on day 7 of 13. TDST support at 165.52 – near the recent lows remains important. I’ll post this chart a few times this week.

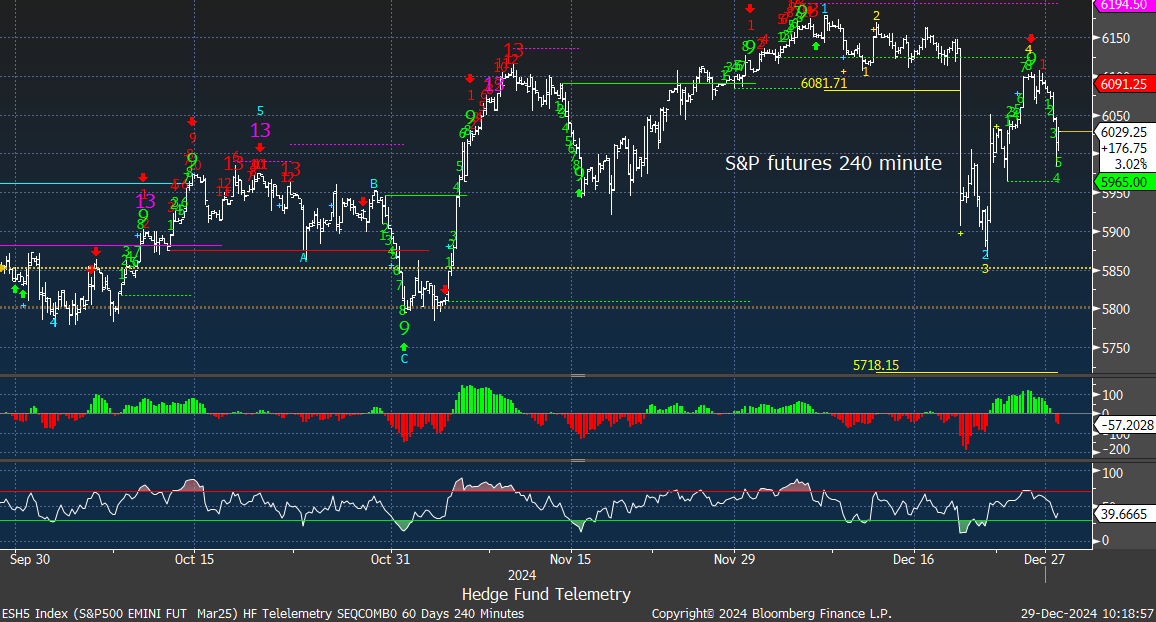

The 60 minute S&P 500 futures shows the bounce from last week giving back some on Friday although up on late in the day off the lows. A downside Sequential pending on hour bar 9 remains a risk for a lower move.

The 240 minute chart shows the reversal off the recent bounce. A break of the wave 3 lows (yellow 3) would qualify downside wave 5 of 5 with potential price objective of 5718

REKR charts look decent for a continued move higher with both daily and weekly DeMark buy Countdown 13’s in play. The huge volume in the last few days might continue higher for a few weeks. (hopefully longer!) As always, keep your size small as this remains a high risk, high reward idea.

I don’t expect this to go back to 25 anytime soon but a move to 4-5 would be nice. Let’s keep our expectations low.

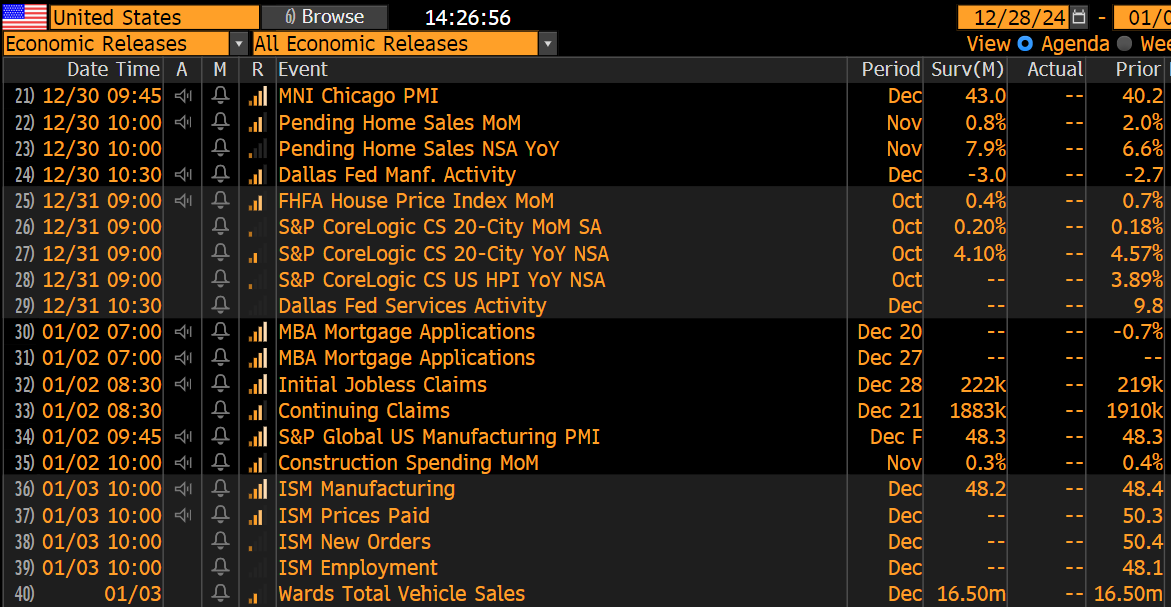

US economic data for the week

KEY MARKET SENTIMENT

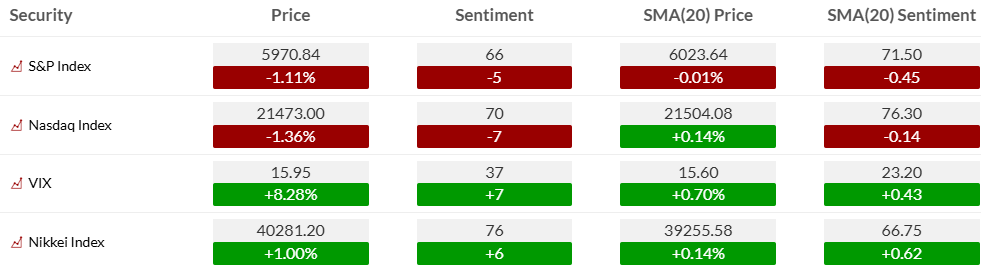

Equity bullish sentiment backed off on Friday with both under the now declining 20 day moving averages of bullish sentiment.

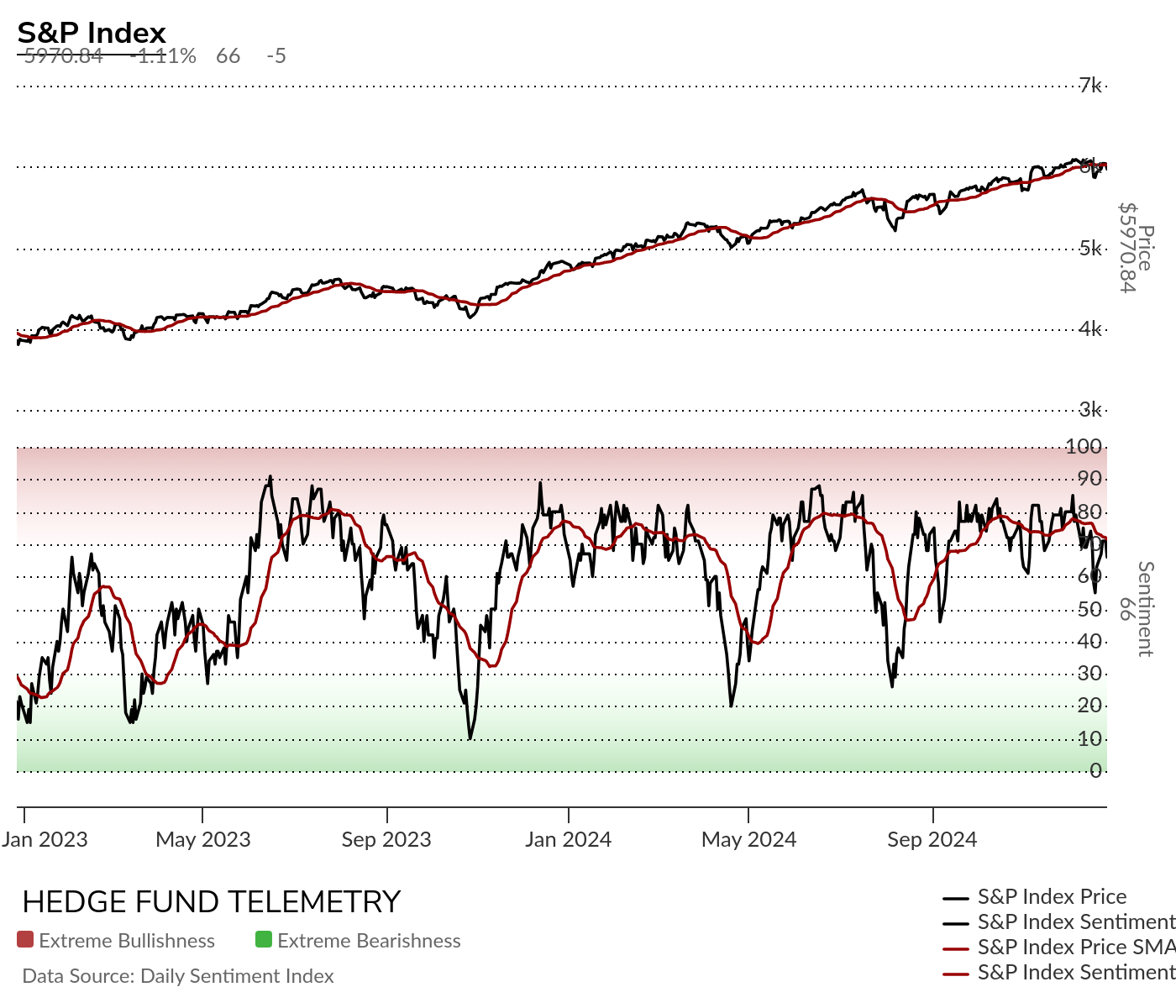

S&P and Nasdaq bullish sentiment possibly starting to make lower highs. S&P is a longer term view. Breaking 50% would see a deeper equity sell off.

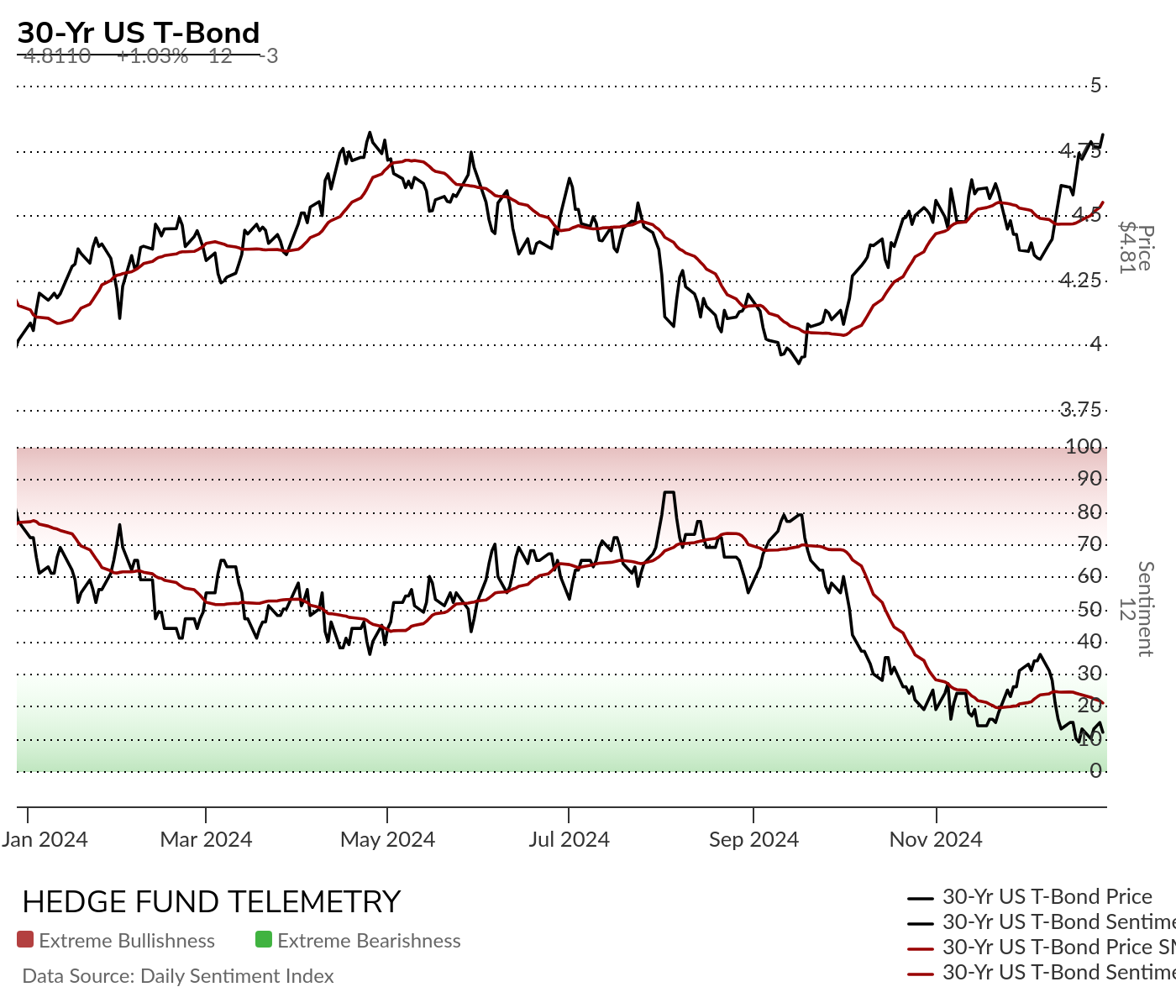

Bond bullish sentiment remains under pressure

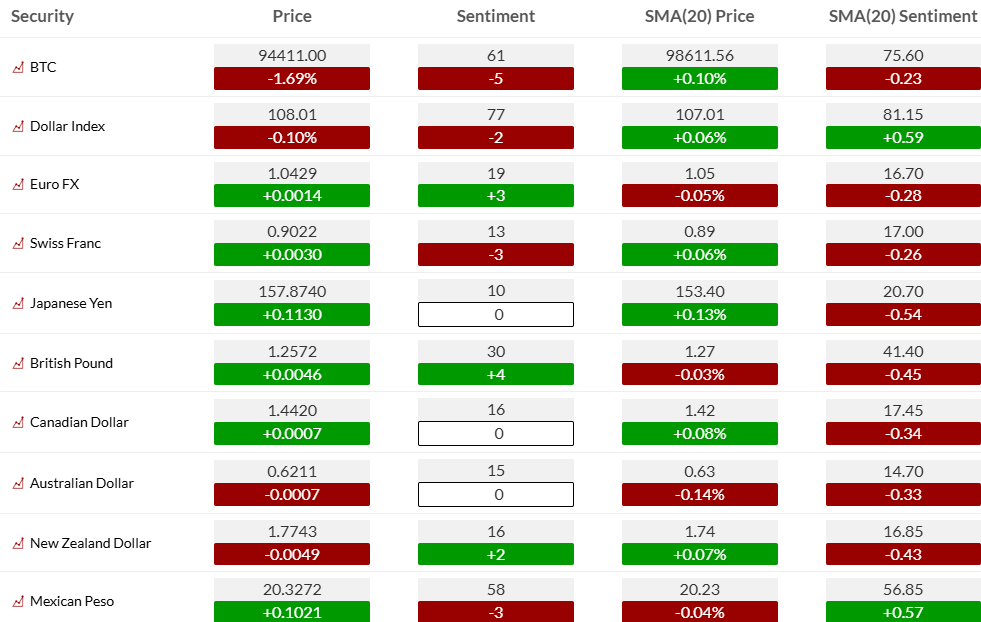

Currency bullish sentiment with US Dollar bullish sentiment dipping into the upper end of the elevated zone. Bitcoin bullish sentiment making a new recent low.

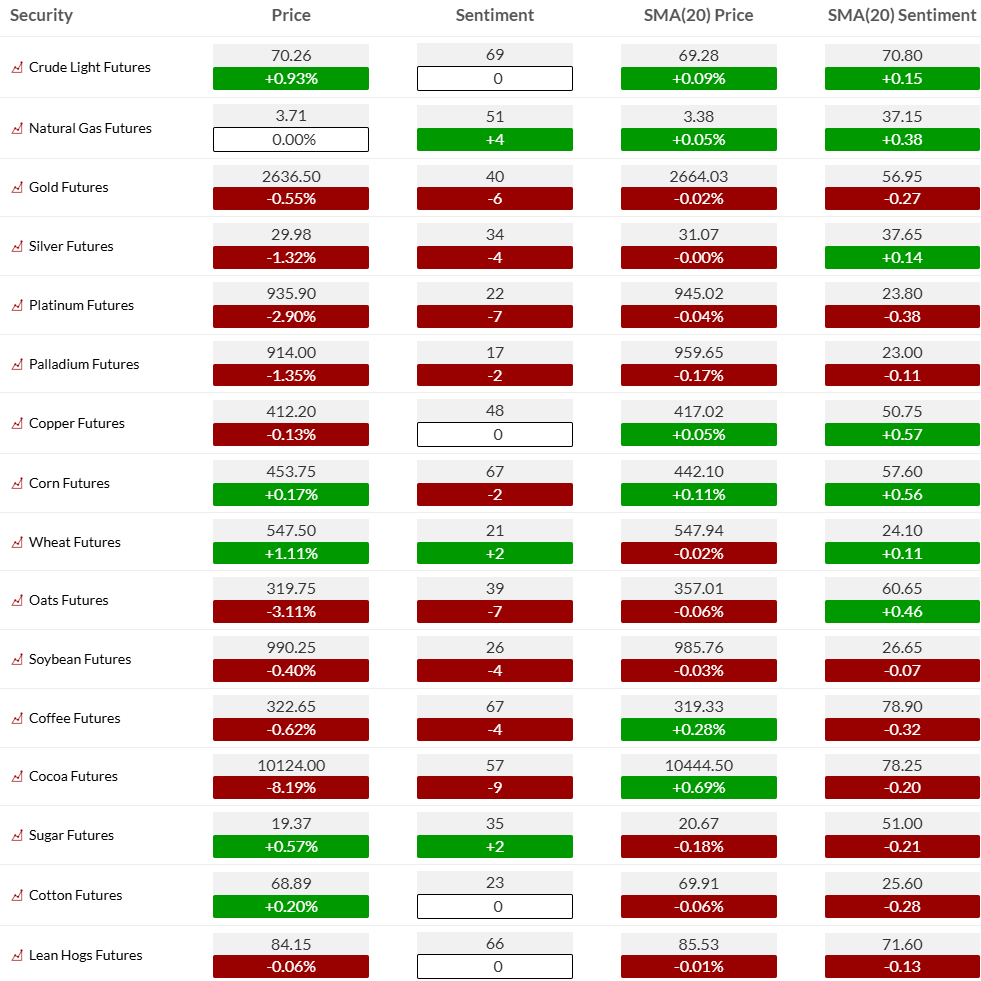

Commodity bullish sentiment continued weakness with metals. Copper holding near 50% and I like it long here. More details on Commodity weekly

EARNINGS, CONFERENCES, AND ECONOMIC REPORTS

- Monday 30-Dec:

- Corporate:

- PDUFA: NBIX (crinecerfont)

- Economic

- US: Chicago PMI, Pending Home Sales

- Europe: PPI y/y, Nationwide House Price Index y/y, Preliminary CPI y/y, KOF Leading Indicator

- Asia: CPI y/y, Non Manufacturing PMI y/y, official Manufacturing PMI y/y

- Corporate:

- Tuesday 31-Dec:

- Corporate:

- PDUFA: 500124.IN (Reditux), ANAB (JEMPERLI), BGNE (Tevimbra), CRNX (paltusotine), GSK.LN (AREXVY), GSK.LN (gepotidacin), GSK.LN (GSK4023393), GSK.LN (Nucala), HPHA.GR (TLX250), KRYS (VYJUVEK), MRNA (mRNA-1345), NOVO.B.DC (WEGOVY), REGN (REGN5458), RLAY (RLY-4008), TLX.AU (ILLUCCIX), TLX.AU (TLX101)

- Economic

- US: FHFA House Price Index, Redbook Chain Store, API Crude Inventories

- Europe: Retail Sales y/y

- Asia: Trade Balance

- Corporate:

- Wednesday 01-Jan: Markets Closed for New Year’s Holiday

- Economic

- Europe: Manufacturing PMI

- Economic

- Thursday 02-Jan:

- Corporate:

- Earnings:

- Post-close: LFCR, RGP

- PDUFA: VRTX (vanzacaftor)

- Earnings:

- Economic

- US: PMI Manufacturing Final, Construction Spending, Weekly Jobless Claims, EIA Natural Gas Inventories, DOE Crude Inventories, MBA Mortgage Purchase Applications

- Europe: Manufacturing PMI, Unemployment Change, M3 Money Supply y/y

- Corporate:

- Friday 03-Jan:

- Corporate:

- Economic

- US: ISM Manufacturing Index

- Europe: SVME PMI, Unemployment Rate, BoE Mortgage Approvals, M4 MoneySupply m/m, Unemployment rate

- Asia: Retail Sales Nominal NSA Y/Y

Thanks to Street Account, Vital Knowledge, and Bloomberg as valued sources.